Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has risen by 0.49% to 1.0759 |

EUR/CHF and USD/CHF, July 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A recovery in US stocks yesterday, coupled with optimism over Moderna’s vaccine, is providing new fodder for risk appetites today. Equities are being driven higher, and the dollar is under pressure. Most equity markets in Asia advanced. China and Taiwan were exceptions, and, in fact, the Shanghai Composite fell for the second consecutive session for the first time in a month. European shares are pushing higher, and the Dow Jones Stoxx 600 is up almost 1% in late morning turnover in Europe. It is the third advance in four sessions. US shares are trading with a clear upside bias, and the S&P 500 will flirt again with unchanged levels for the year. Benchmark yields are mostly 1-2 basis points lower, while the US 10-year hovers around 62 bp. The dollar has been sold across the board. Against the majors, the Scandis are leading the way, but the euro and Australian dollar are standing above key levels ($1.14 and $0.7000, respectively). South Africa, Hungary, and Mexico are leading emerging market currencies higher. The JP Morgan Emerging Market Currency Index is near its best levels in a month. Gold is steady near $1808. On the back of a large drop in API oil inventory estimates (~8.3 mln barrels) and OPEC+ seeking to get compensatory cuts from some excess producers (e.g., Iraq and Nigeria) could offset part of the increase from others, September WTI is near $41. |

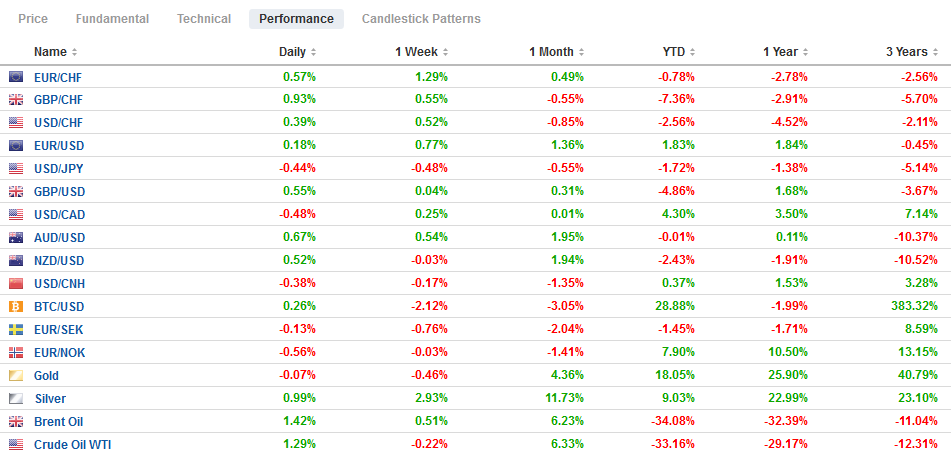

FX Performance, July 15 - Click to enlarge |

Asia Pacific

The USDA confirmed record Chinese purchases of US corn as it scrambles to try to meet its commitments under the Phase 1 trade deal. The order for 1.76 mln tons of corn for the 12 months beginning September 1 is the fourth largest order on record. It follows on the heels of a separate order last week for 1.36 mln tons (almost evenly divided between delivery by the end of August and for the year beginning September 1. China has also boosted its orders for soy and wheat in recent weeks too. It sounds impressive, and it is, but it is still small beer. Consider that two orders for corn together are worth around $410 mln. China agreed to double its agriculture exports from the 2017 level of $24 bln.

The Bank of Japan, as widely anticipated, did not alter policy. However, its forecasts show that its pessimism has not been lifted. In April, it forecast the economy would shrink by 3%-5% in the fiscal year ending next March. Today’s forecast puts the contraction at 4.7%, and that assumes not another widespread shutdown. While that may seem reasonable, Tokyo raised its alert level to its highest today.

Since China enacted its new security law in Hong Kong, there has been a threat of a brain drain, as several countries, including the UK and Australia, make it easier for Hong Kong nationals to emigrate. While China has taken offense, it does not want to be left behind. Reports suggest it is shifting its tax on Chinese citizens to include their global income. This is effectively a large tax hike on those living in HK.

It has been five sessions since the dollar traded above JPY107.50. In Europe, it is struggling to hold above JPY107.00, where a $755 mln option is struck that expires today. There are also options for around $1.12 bln between JPY107.25 and JPY107.30 that expire as well. The recent low was near JPY106.65, and below there, the JPY106 area is the bottom end of a three-month trading range. The Aussie was bid to $0.7020, its highest level in a month, in the local time zone. It has been straddling the $0.7000 area in Europe. Initial support is seen near $0.6980. The PBOC set the dollar’s reference rate a little softer than the models suggested, and the dollar fell below CNY6.99 today. The dollar has fallen in eight of the past ten sessions against the yuan.

Europe

The jockeying for position ahead of the EU’s summit at the end of the week continues. There are two sources of misdirection. First, the commentariat class consumed many column inches, debating explaining what a common bond is necessary and appropriate now. The big Hamilton Momentum. Yet, it is among the least controversial elements. Second, the “Frugal Four” was seen as the main obstacle. It has been clear for several weeks at least that they could largely be coopted through expanding rebates. As the selection of the Eurogroup President recently illustrated, eastern and central European members.

Yesterday, Hungary’s parliament approved a resolution for Prime Minister Orban to reject the EU Recovery Plan and seven-year budget until the EC ends its investigation into potential violations of the rule of law. The EU decision needs to be unanimous, and given the urgency, it creates a powerful incentive for a defect, i.e., hold out for individual concession. Merkel seems to have suggested that she has room to compromise, while Dutch Prime Minister Rutte sounded doubtful, and agreement can be reached.

On the eve of the summit, the EU has been dealt a blow. The General Court, the second-highest in the EU, ruled against the EC’s decision that ordered Apple to pay 13 bln euros in back taxes to the Irish government in 2016. The court ruled that the EC failed to demonstrate that the tax arrangement was an illegal state subsidy. The EU can appeal the decision, but it seems to undermine Brussel’s effort to pursue low tax members. In recent days, reports had surfaced, suggesting the EC was going to try a new tactic in addressing the corporate tax regimes that seem to facilitate tax avoidance strategies. The Netherlands, Luxembourg, Belgium, and Ireland were the likely targets, and EC sought an approach that would require a qualified majority rather than unanimity.

The UK reported June inflation figures. CPIH rose 0.8% year-over-year after a 0.7% pace in May. CPI itself rose 0.1% in June for a 0.6% year-over-year rate. The core rate ticked up to 1.4% from 1.2%. Producer prices were mixed. Input prices accelerated (2.4% month-over-month from a revised 0.9%, initially 0.3%), but the year-over-year rate remains well below zero (-6.4%). Output prices rose 0.3% and are still off 0.8% year-over-year. There appeared to be little market reaction. Tomorrow the UK reports employment figures.

The euro reached four-month highs in early European turnover near $1.1445, just shy of the $1.1450 option for nearly 825 mln euros that expires today. The intraday technicals are stretched, and the immediate risk is on the downside. There is a 1.7 bln euro option at $1.14 that expires today, too, which could be a factor. Look for the $1.1380 area to contain losses. Sterling was testing support around $1.25 yesterday and today has tested resistance near $1.2630. It too appears to have been over-extended in early European turnover, and an initial pullback is likely now. The $1.2550-$1.2575 should offer support.

America

It is the first policy decision for the new Bank of Canada Governor Macklem. It is also the first meeting since the government clarified its fiscal strategy. The budget deficit this year will around 16% of GDP, and the government will issue about C$400 bln of debt this year, something on the magnitude of three times more than last year. Since April, the central bank has been buying almost C$7 bln a week after committing to buying at least C$5 bln a week. Some observers argue that the increased government outlays requires the central bank to buy more bonds. However, we suspect the government issuance is only one variable in the equation, and it may not be the decisive one.

Long-term asset purchases appear primarily aimed at either helping markets stabilize or supporting financial conditions when the zero-bound has been approached. The markets have stabilized, and so have interest rates. Consider the 3-year yield. The Reserve Bank of Australia is targeting it at the cash rate of 25 bp. The three-year yield in Canada has been hovering around 30 bp for more than a month. There is no upside pressure. The 10-year yield has been mostly in a five basis point range above 50 bp. That said, the Canadian dollar is the only major that has fallen against the US dollar over the past month. However, for all practical purposes, the decline is immaterial for policymakers. Meanwhile, illustrated by June employment and housing starts, the economy is on the mend. It is not yet showing the resurgence of the virus that is seeing many US states reintroduce closures and weakening some high-frequency economic data.

A US District Court judge announced that the US government has agreed to rescind last week’s decision that international students must take at least one in-person class or lose the right to remain in the US. The issue is not necessarily fully resolved.

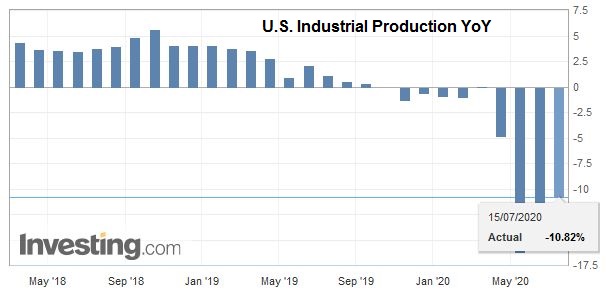

| The US reports June industrial production figures today. Recall that in March and April, industrial output fell by 4.6% and 12.5%, respectively. It rose 1.4% in May and is expected to have accelerated by more than 4% in June. Last year, industrial output fell in seven of the 12 months. Manufacturing production fell by 5.3% and 15.5% in March and April before bouncing by 3.8% in May. |

U.S. Industrial Production YoY, June 2020(see more posts on U.S. Industrial Production, ) Source: investing.com - Click to enlarge |

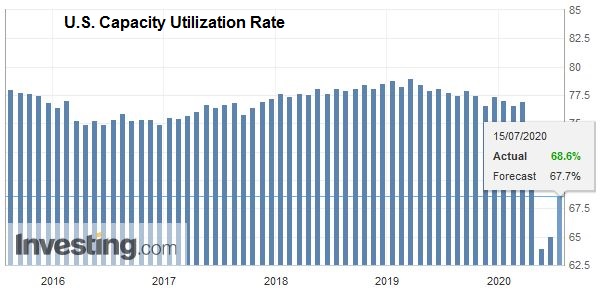

| It is expected to have risen by a little more than 5.5% last month. However, given the new surge in virus cases, June data may be too old for investors. The first survey data from July will be made available today in the form of the Empire State Manufacturing Survey. It is forecast to show the first positive reading since February. The Beige Book, in preparation for the July 29 FOMC meeting will be released later today. Its anecdotal survey may shed more light on how the new closures are impacting activity. |

U.S. Capacity Utilization Rate, June 2020(see more posts on U.S. Capacity Utilization Rate, ) Source: investing.com - Click to enlarge |

The Canadian dollar is not only a laggard over the past month, but even today, it is among the weakest of the majors with around a 0.2% gain against the greenback. Only the Swiss franc, which is virtually flat, has done worse among the majors. Here in July, the US dollar has been confined to a range of about CAD1.3490 to CAD1.3650. Yesterday, it probed the upside. Today, it is finding support near CAD1.3580. The US dollar also appears rangebound against the Mexican peso. It seems comfortable with an MXN22-handle. The greenback’s low this month is near MXN22.15. The dollar has fallen against the peso in 9 of the past 12 sessions coming into today, and yesterday’s nearly 1.4% decline was the largest in a month.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Bank of Japan,China,EU,Featured,newsletter