Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has risen by 0.24% to 1.0862 |

EUR/CHF and USD/CHF, September 30(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: As the quarter ends, the capital markets are mixed. Equities in Asia Pacific were heavier, except in Hong Kong and Australia, while shares were mixed, leaving the Dow Jones Stoxx 600 little changed through the European morning. US shares are trading firmer. Benchmark 10-year bond yields are 2-3 basis points higher, though Australia’s bond yield was up seven basis points. The Australian and New Zealand dollars are bearing the brunt of the stronger US dollar today. The Aussie is testing last week’s base, while the Kiwi is unwinding last week’s gains. Sterling and the Canadian dollar are posting small gains. The South Korean won and Turkish lira leading the emerging market currencies with modest gains (~0.3%), while the South African rand (-~-0.5%) and Indian rupee (~-0.25%) are bringing up the rear. The price of gold has fallen in four of past five weeks and is testing the shelf created last month in the $1483-$1485 band. A break would undermine the technical tone and warn of 5% or more downside risk. After losing 3.75% last week, November WTI is trading with a heavier bias today. |

FX Performance, September 30 - Click to enlarge |

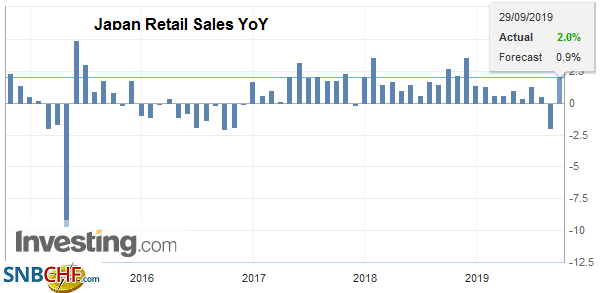

Asia PacificJapan is set to hike the sales tax tomorrow, and it appears that consumers may have stepped up their purchases ahead of the increase. August retail sales jumped 4.8%, twice the median forecast in the Bloomberg survey. Household machinery surged 17.4%. To the extent this is “tax arbitrage, then it borrows demand from the future. That means that it may not fuel sustained economic strength. Japan reported industrial production in August, in the face of the surge in retail sales, fell by 1.2%. The median forecast was for a 0.5% decline. The 4.7% contraction year-over-year is the steepest in four years and speaks to the deflationary forces that the BOJ may feel compelled to respond to at the end of the month. South Korea reported its August industrial output fell 1.4%. A pullback was widely expected after the 2.6% (revised to 2.8% jump in July), but economists had expected a smaller (~1.0%) decline. The year-over-year decline of 2.9% is the most since February. The central bank is already on alert for the loss of economic momentum. It boosts the chances of a cut in the seven-day repo rate (now 1.50%) after the hike last year was reversed in July. The won appreciated by about 0.8% this month to pare this quarter’s loss to a little less than 4% (the weakest in Asia). |

Japan Retail Sales YoY, August 2019(see more posts on Japan Retail Sales, ) Source: investing.com - Click to enlarge |

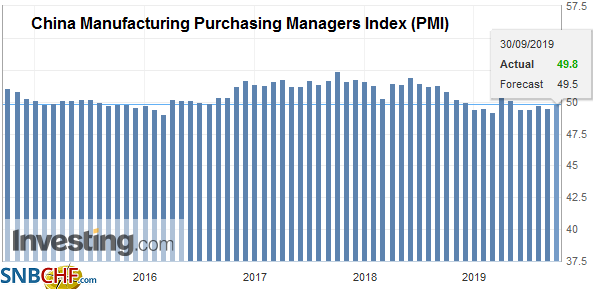

| China’s September PMI may be showing some signs of stabilization, but it does not rule out additional stimulus. The manufacturing PMI edged up to 49.8 from 49.5, leaving it still in contraction mode. |

China Manufacturing Purchasing Managers Index (PMI), September 2019(see more posts on China Manufacturing PMI, ) Source: investing.com - Click to enlarge |

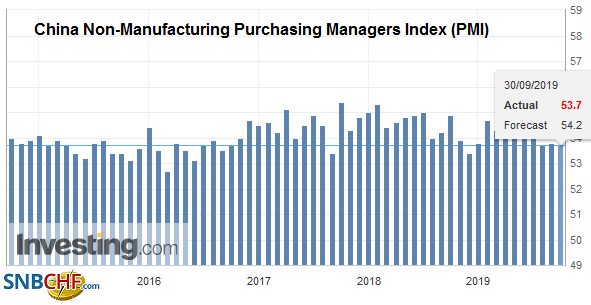

| The non-manufacturing PMI slipped slightly to 53.7 from 53.8. The composite reading stands at 53.1 from 53.0 in August. |

China Non-Manufacturing Purchasing Managers Index (PMI), September 2019(see more posts on China Non-Manufacturing PMI, ) Source: investing.com - Click to enlarge |

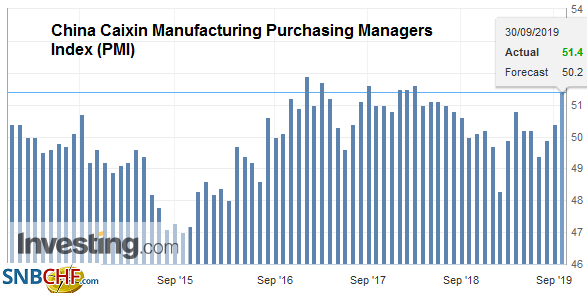

| The Caixin manufacturing PMI, which is understood to focus more on small businesses than the so-called official one, rose to 51.4 from 50.4. Tomorrow begins the week-long holiday celebration. President Xi’s speech tomorrow is expected to be closely watched for insight into the broad strategy in dealing with the confrontation with the US and the slowing economy. Separately, the PBOC set the dollar’s reference rate today at CNY7.0729 (CNY7.0731 previously). The dollar closed near CNY7.1225 before the weekend and is near CNY7.14 now, the strongest in three weeks. |

China Caixin Manufacturing Purchasing Managers Index (PMI), September 2019(see more posts on China Caixin Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The dollar has been confined to about a quarter of a yen below JPY108.00, where a $950 mln expiring option is struck. There is another option at JPY107.50 ($1.5 bln) that will also roll-off today. The pre-weekend low was about JPY107.65, and the high was almost JPY108.20, and the greenback looks comfortable within it. The Australian dollar is testing the shelf forged last week near $0.6740. The Reserve Bank is widely expected to cut the cash rate by 25 bp tomorrow for the third cut this year. A break risks $0.6700, and although it was penetrated on an intraday basis a few times in August and September, it has not closed below there. On the upside, it likely takes a close above $0.6800 to lift the tone.

EuropeThe Austrian election results reflect broad trends. First, the populist-anti-immigration fervor is not in ascendancy throughout Europe as it previously appeared. The AfP did win state elections as had been projected in Germany. In Italy, the League’s gambit was rejected, and the Democrat Party-Five Star alliance will likely find a more support EC. The anti-immigration Freedom Party in Austria was humbled by the recent scandal, and its support fell to 16% from 26% in the last national election two years ago. Second, in Austria, as throughout Europe, climate change has risen in political significance, and this is reflected in the fortunes of the Green Party. In Austria, the Greens support practically tripled to 14%. A survey by Eurobarometer showed concern about the environment surpassed poverty and terrorism as the most important concern in Austria since 2017. Germany reported a 0.5% gain in August retail sales, in line with expectations. A pleasant surprise was delivered though as the July series was revised to show a fall of a 0.8% rather than the initial 2.2% drop. The unemployment queues fell by 10k in August while economists had expected an increase (5k) and the increase in July was halved (to 2k). The states have reported their preliminary September inflation estimates and the country’s EU-harmonized estimate, which will be reported shortly, is expected to be little changed from the 1.0% pace seen in August. Italy reported a 1.5% jump in September CPI, which is a seasonal quirk. The year-over-year pace slowed to 0.3% from 0.5%. Separately, Italy reported that unemployment fell to 9.5% from a revised 9.8% (was 9.9%). This is an eight-year low. Attention is turning to the new government’s 2020 budget. The strategy may be to submit figures that would project a 2.1% deficit and then negotiate for a little bit more. The draft budget is due in Brussels in the middle of October. |

U.K. Gross Domestic Product (GDP) YoY, Q2 2019(see more posts on U.K. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

The euro is in less than a fifth of a cent range below $1.0950. The uninspiring activity is not neutral, however. The failure to sustain even modest ticks shows the bears still have the whip hand. There is a 2.3 bln euro option at $1.09 that expires today, and below there is another 1.5 bln option at $1.0875. Sterling is hanging in better and is trying to snap the three-day down draft seen in the second half of last week. Still, sterling has been stymied just in front of the pre-weekend high a little above $1.2335. Turkey’s trade deficit narrowed, and the government updated its economic forecasts to project stronger growth and lower inflation. It will report September CPI later in the week, and a sharp decline (toward 9% from 15%) will set the stage for another dramatic rate cut (October 24). The dollar is approaching the 200-day moving average near TRY5.63, its lowest level since mid-August.

America

The Federal Reserve’s overnight and two-week repo conducted before the weekend were under-subscribed, suggesting the banking system had adequate liquidity. The overnight repo operations will continue into early October. At the meeting at the end of the month, the Fed is expected to announce what it intends to do going forward. Some have argued for a new round of QE and others have argued for organic growth of the balance sheet, which was commonplace before the Great Financial Crisis. Both approaches have one thing in common. They both boost excess reserves without necessarily increasing liquidity to the repo market. That means that organic growth and new asset purchases might be the right answer to a different problem. If the problem is that banks’ don’t have sufficient excess reserves, these measures will address it.

However, if the problem is that even with excess reserves, banks may be reluctant to participate in the repo market. To boost the likelihood of banks to re-engage the refi market, the regulatory framework, which creates some disincentives, may have to change. In lieu of this, which does not seem particularly likely any time soon, then a standby refi facility appears to be the most likely way to ensure sufficient liquidity. Moreover, we think that the Fed does not want to confuse these plumbing issues and monetary policy proper by using the same tool (QE) for both.

The US economic data highlight will be the employment report at the end of the week, and no fewer than a dozen Fed officials speak over the next several days. However, the week begins off slowly with no Fed officials on tap and only secondary or tertiary reports of the Chicago PMI and the Dallas Fed’s manufacturing survey. Canada reports raw material and industrial price gauges today, but keener interest is in the July GDP report tomorrow and the trade figures at the end of the week.

The US dollar approached a two-week low against the Canadian dollar before the weekend, but the selling pressure abated. The greenback is languishing around little changed levels and is confined to a little more than a 10-tick range on either side of CAD1.3235. Our reading of the technical favors further dollar gains against the Mexican peso. Provided the MXN19.60-area holds, we look for an initial move to MXN19.79 and then MXN19.90.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,China Caixin Manufacturing PMI,China Manufacturing PMI,China Non-Manufacturing PMI,Currency Movement,EUR/CHF,FX Daily,Japan Retail Sales,newsletter,South Korea,U.K. Gross Domestic Product,USD/CHF