Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

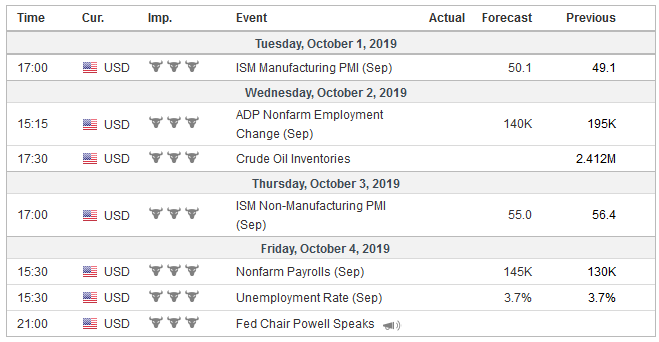

United StatesThe world’s largest economy appears to have grown by about 2% in Q3 at an annualized pace, the same as in Q2, and in line with what many Fed officials understand to be trend growth. The strength of the US labor market underpins consumption, the powerful engine of the US economy. The latest readings of both the labor market and consumption will highlight the economic data in the week ahead. The strength of the recent housing data (starts and sales) suggest that the decline in interest rates is beginning to have some traction in the particularly sensitive sectors of the economy. It seems that the economic conditions that foster residential investment also favor auto sales. US light vehicle sales have averaged 16.93 mln a month a seasonally-adjusted annual basis. In both 2017 and 2018 average sales averaged about 17.15 mln. Lower interest rates and greater average incentive (industry estimates average in September of $4.2k compared with $4.0k in September 2018) would favor a gain on the 16.97 mln pace seen in August. However, there is a quirk in the calendar that warns the report may disappoint. The weekend before Labor Day (September 2) was captured in August’s report. Auto sales and jobs growth are cyclical. The 12-month moving average of US vehicle sales peaked in February 2016 at 17.57 mln. With all the revisions, it may be hard to keep track of it, but the 12-month average of non-farm payroll growth peaked in February 2015 at 260k. In a revealing but straightforward way, it illustrates where the US economy is in the business cycle. US job growth is slowing. The average monthly job growth this year has been 158k. In the first eight months of 2018, an average of 234k jobs were created. The quarterly average has steadily fallen this year, and it will again if the jobs growth reported on October 4 is less than 178k. The median forecast in the Bloomberg survey calls for 140k after August’s 130k. Weekly jobless claims were flat between the survey periods. Some survey data has warned of weakness. The GM strike and government census hiring could impact the September jobs report in opposite directions. The takeaway message is lower interest rates (10-year yield is about 30 bp lower year-over-year) and lower oil prices (~15% year-over-year) maybe helping the US economy extend its recovery in the face of the end of the fiscal stimulus, tax hikes (on imports), and trade certainties and uncertainties. The economy may show sufficient rigor and price pressures sufficient firmness that a consensus toward a standing pat after two cuts may gain currency. At the same time, the Fed will likely provide some details of its assessment of the banking system’s reserve demand at the October meeting. Given the extent of the confusion among investors, it would be instructive for the Fed to separate its operational issues, the plumbing, if you will, from the conduct of monetary policy proper. Arguably a way to do that is not to announce a change in both simultaneously, i.e., at the October meeting. When the US money market calm returns as we expect, then let’s assume for the sake of the exercise that the fed funds effective rate averages 1.85%. A 25 bp rate cut would bring it to 1.60%. The implied yield of the January 2020 futures settled last week at 1.5750%. At this juncture, the market appears to accept the Fed’s framing of the issue as a midcourse correction that will extend the record-long recovery. |

Economic Events: United States, Week September 30 - Click to enlarge |

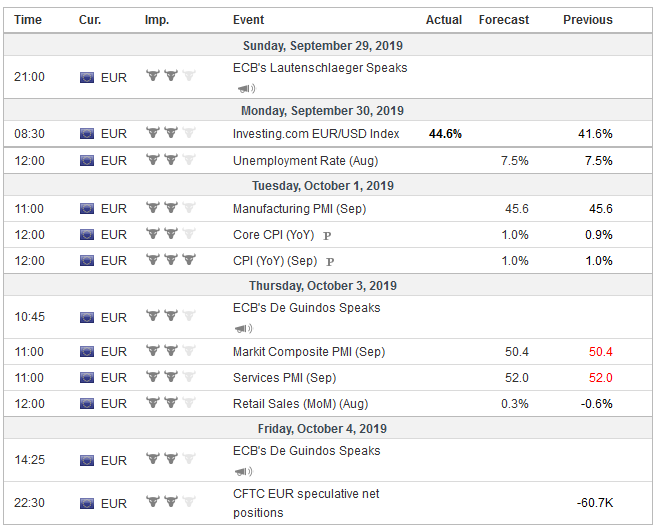

EurozoneThe final September PMI for the eurozone is the main economic report from the EMU in the week ahead. Yet, typically it does not deviate much from the flash report or change the general view that the eurozone has yet to emerge from the soft patch it has hit. The monetary lever has been used again, even as money supply growth and bank lending remains robust. The resignation of Lautenschlager Germany’s representative on the ECB Executive Directors came as a surprise. The ECB’s recent decision on re-activating its asset purchases program was controversial. This time, according to reports, the French joined the Germans, Dutch, Austrians, and Estonians, who have objected to asset purchases from the get-go. Draghi was asked explicitly about the disagreement at his press conference and acknowledged it was the only measure that was disputed. He refused to “name names,” but it was clear, he explained, without taking a formal vote that there was a clear majority of support to resume the buying. Some official thought it proper to provide what Draghi refuse to in terms of how countries voted. Typically, winners do not go to the media. There is no reason. It is often those that lost the battle to take their case to the press. Many, if not most, accounts link the resignation to past resignations of German officials at the ECB who have resigned in protest, like Weber and Stark. Some reports suggest Lautenschlager was one of the only members of the executive board to oppose the asset purchases. If true, it says something more about Germany and its frustration of some officials to being over-voted and less about the conduct of monetary policy. It has little bearing on interest rates or exchange rates. It is most unlikely to change the configuration of the ECB, with another German woman, who likely is as wedded to ordoliberalism, be named to replace Lautenschlager. The more things change, the more they stay the same. Brexit, as Lewis Carroll might have said, is becoming curiouser and curiouser. UK Prime Minister suspension of Parliament was ruled illegal by the UK Supreme Court. It is a defeat of historic proportions. However, it changes little. The UK needs to take positive action of some kind to avoid leaving at the end of October. Thus far, Johnson’s proposals are not satisfactory to the EC, and a large gap remains. Parliament has ordered the Prime Minister to seek a three-month extension of Brexit. Johnson has indicated he will ignore it or look for a legal way around his instructions with the sole purpose in mind as to circumvent the will of Parliament. This was, of course, the grounds on which the prorogation of Parliament was illegal. At the same time, what is the EU to do? If there is no request from the Prime Minister for a delay at the October 17-18 EU summit, momentum picks up toward a no-deal exit. Parliament will be faced with a cruel dilemma: accept a no-deal exit, which it is loathe to do, or revoke Article 50, which would be politically controversial. Sturgeon, the head of the Scottish Nationalist Party, signaled another possible path. She suggested a willingness help defeat Johnson in a vote of confidence and could support Corbyn as an interim PM, who would seek an extension and then election. The SNP would do well in an election in part because of Labour’s refusal to endorse Remain. The Tory Party Conference runs from September 29 through October 2. Two things may come from it. First, Johnson will solidify his election strategy as the people against Parliament. Yet, with the Supreme Court’s decision, it looks more like 10 Downing Street against the representatives of the people and the guardians of the rule of law. Second, Johnson’s concrete proposals to make a backstop unnecessary need to converge more with the EU, and this may be the last opportunity ahead of the EU Summit. |

Economic Events: Eurozone, Week September 30 - Click to enlarge |

ChinaChina is on holiday after Monday, celebrating the 70 years of Communist rule, a year longer than the Soviet Union. It faces three challenges: trade conflict with the US, unrest in Hong Kong, and a slowing of the domestic economy. President Xi may be the most powerful leader in China since Mao, but the challenges may be more formidable him. It seems naive if Chinese officials believe a Democrat president would be easier on China. Instead, to the extent that the issue is discussed, many of the Democrat candidates talk about working through the WTO. Such an approach is consistent lead an alliance to mount a broad and sustained push for China to be a better actor on the world stage. However, now the US may be seen as unpredictable in the extreme. One day the US President complains that China is not buying US agriculture goods, the next he pushes against a short-term agreement part of a long-term and larger agreement. Then Trump says that an agreement may be closer than is thought while sanctioning Chinese oil companies for helping Iran circumvent the embargo. Reports before the weekend that Trump Administration is looking at ways it can disrupt the portfolio capital flows going into China’s stock and bond markets. Measures that apparently were discussed include delisting Chinese companies from the US exchanges, limiting exposure of government pension funds, and mandating caps on benchmark indices. Around 155 Chinese companies are listed on US exchanges with a combined market cap of $1.2 trillion. This underscores our hypothesis that strategic end-game in the US-China conflict is a period of disengagement. We understand this broadly to include people, goods, money, and information. It also strengthens our conviction that the administration would not seriously contemplate selling dollars and buying yuan as intervention would imply. |

Economic Events: China, Week September 30 - Click to enlarge |

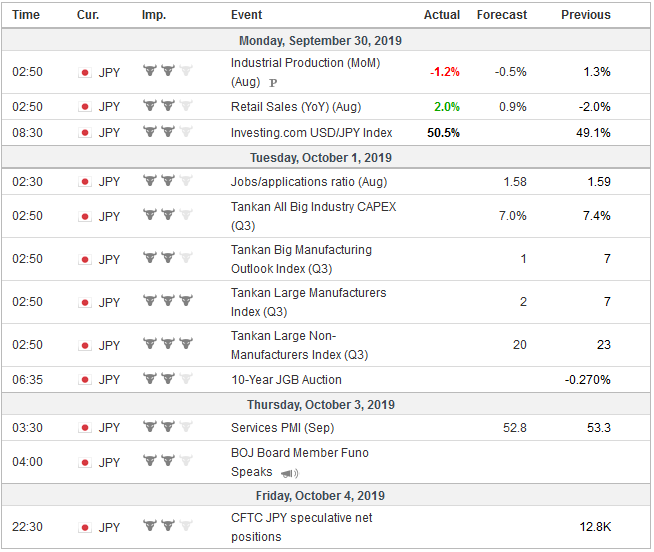

JapanJapan’s sales tax will be increased to 10% from 8% on October 1. It is not exactly clear why Prime Minister Abe insists on raising the tax when aggregate demand is not robust, trade tensions not just between the US and China but between Japan and South Korea, and slowing world growth make for a challenging international environment. Whatever sovereign debt concerns there are (over 200% of GDP), the fact another arm of the government, the BOJ, owns around half, changes the dynamics. Moreover, as the Q3 Tankan survey (September 30) is expected to show the modest momentum the economy appeared to enjoy earlier this year has faded. |

Economic Events: Japan, Week September 30 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week September 30 - Click to enlarge |

The Reserve Bank of Australia meets on October 1. About 20 bp appears (ostensibly of a 25 bp move) seems to have been discounted. We suspect this cut, which will bring the cash rate to 0.75% is the last move before an extended pause. A combination of lower rates, a weaker currency, and like some many are calling for in Europe, fiscal stimulus (tax cuts) should help the economy gain some traction.

Full story here Are you the author?Tags: Brexit,China,federal-reserve,jobs,newsletter,RBA