Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

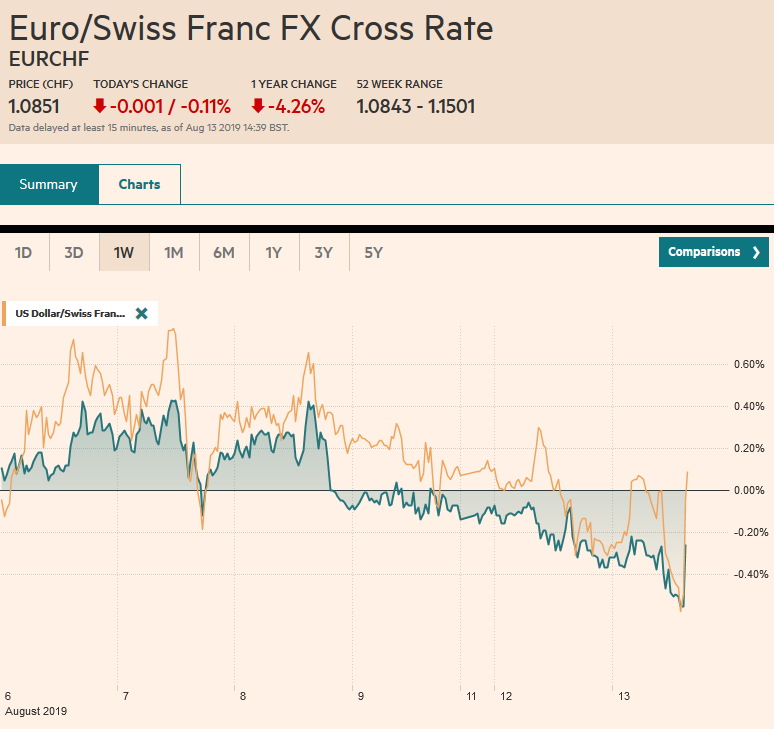

Swiss FrancThe Euro has fallen by 0.11% to 1.0851 |

EUR/CHF and USD/CHF, August 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

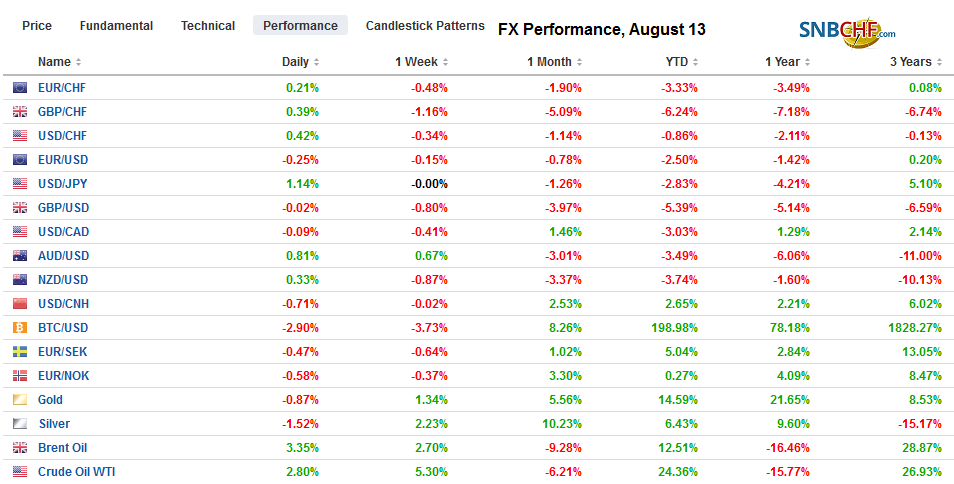

FX RatesOverview: The confrontation in Hong Kong and the fallout from the Argentine primary over the weekend join concerns the conflict between the two largest economies and slower growth to force the animal spirits into hibernation. Global equities remain under pressure. Japan’s Topix joined several other markets in the region to have given up its year-to-date gain. The MSCI Emerging Markets equity index is not from doing the same. European shares are faring better, and with today’s roughly 0.6% loss, the Dow Jones Stoxx 600 is up almost 9.2% this year. US shares are trading lower, which if sustained, would leave the S&P 500 up just shy of 15%. Bond yields are lower, and several European sovereign bond yields are at new record lows. The first European corporate 10-year bond (Nestle) yield slipped into negative territory. Italy’s vote of confidence looks more likely for next week, and this is allowing Italian bonds to stabilize after yields surged in recent days. China’s 10-year yield briefly dipped below 3% for the first time in three years. The US 30-year yield is slipping closer to the record low near 2.08%. The US dollar is firm against most of the world’s currencies, with the notable exception of the yen and Australian dollar. |

FX Performance, August 13 - Click to enlarge |

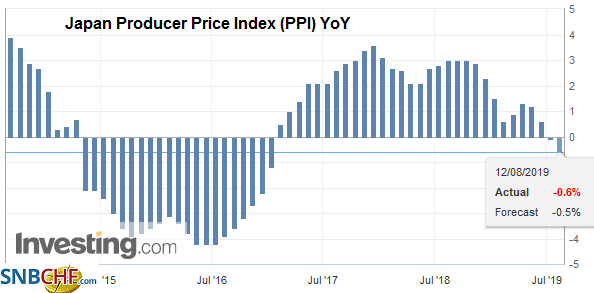

Asia PacificChinese officials continue to moderate the pace of the yuan’s decline. The dollar fix was set at CNY7.0326, while the models projected CNY7.0357. This means that the discretionary element in setting the reference rate was for a slightly stronger yuan. Yesterday’s report of slowing aggregate social financing seems to have set off two impulses. First, there is greater concern about the outlook for the Chinese economy as the slower lending is seen asphyxiating the economy, even though the linkages between lending and growth have become attenuated. Second, there seems to be greater confidence that the PBOC will ease policy. A cut in required reserves is the most common expectation, but there is also the risk of a rate cut. Developments in Singapore, a regional entrepot, often reflect regional forces and today’s disappointing Q2 GDP weighs on sentiment. The Strait Times equity index gapped lower and is up about 2.25% year-to-date. Q2 GDP contracted by 3.3% at an annualized rate, worse than the 2.9% decline expected and it is the second contraction in the past three quarters. Arguably more important is the government’s pessimism. It now expects the economy to expand 0-1% this year down from 1.5%-2.5% forecast in May and weaker than the IMF’s recently minted forecast of 2%. Singapore reports non-oil export figures for July on Thursday, and there is some hope that the pace of declines will begin moderating. Last week’s figures showing that the Japanese economy expanded at a stronger than expected pace in Q2 (1.8% annualized vs. median expectations for 0.5%) and Q1 was revised to 2.8% from 2.2%. However, the BOJ remains in a bind. The decline in PPI (-0.6% year-over-year vs. -0.1% in June) is the lowest since the end of 2016 and warns of renewed deflationary pressures. The 10-year JGB yield is at minus 25 bp, which seems to challenge the BOJ’s ability to effectively manage the yield curve, just as reports suggest other central banks, including the Federal Reserve, are interested in understanding it better. |

Japan Producer Price Index (PPI) YoY, July 2019(see more posts on Japan Producer Price Index, ) Source: investing.com - Click to enlarge |

The dollar remains pinned in its trough against the yen. It has not broken JPY105, but it has not been able to resurface above JPY105.60. These levels also match option expires today ($1.7 bln at JPY105 and almost $800 mln at JPY105.60). A break of the flash crash low of roughly JPY104.85, and last year’s low (~JPY104.65) risks emboldening participants to look for a move toward JPY100. While some reports speculate that Japan’s pension funds can buy US assets in a “stealth” intervention, we wonder if Japanese pension funds are part of what is taking the yen higher. Japanese pension funds and insurance companies had bought the unhedged US and European bonds and now reportedly are boost hedge ratios. The Australian dollar appears to be finding support a little below $0.6750. It must resurface above $0.6820 to be anything important. Meanwhile, initial resistance is seen near $0.6770.

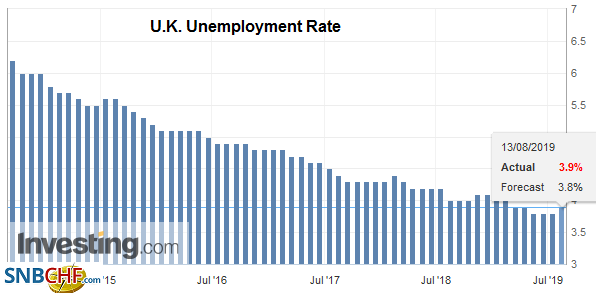

EuropeThe UK reported a stronger than expected employment report. The two highlights are job growth (3m through June, the UK added 115k jobs, nearly twice what economists expected) and average weekly wages rose 3.9%, excluding bonus payment, up from 3.6%. It is the strongest rise in over a decade and appears to have been helped by the timing of wage increases by the National Health Service. Marring the otherwise favorable report was the rise in unemployment to 3.9% from 3.8%. There is little new on the Brexit front. With a little more than two months to go, both sides of the Channel seem to show little sense of urgency. |

U.K. Unemployment Rate, June 2019(see more posts on U.K. Unemployment Rate, ) Source: investing.com - Click to enlarge |

| German investor sentiment continues to worsen. Economists had expected some deterioration, but it was more than expected. The assessment of the current situation stands at -13.5 in August. This was more than twice the drop that economists expected and follows a -1.1 reading in July. It is the lowest since 2010. The expectations component imploded to -44.1 from -18 in July. The median forecast in the Bloomberg survey was for -24.5. |

Germany Consumer Price Index (CPI) YoY, August 2019(see more posts on Germany Consumer Price Index, ) Source: investing.com - Click to enlarge |

For the seventh session, the euro is straddling the $1.12 level. There is a 1.1 bln option at $1.1215 that expires today. The high in Asia was $1.1220. The euro is finding bids around $1.1180. Initial resistance is seen near $1.1230, and a more important cap is seen in the $1.1250-$1.1265 band. Sterling continues to consolidate above $1.20. It has not been able to rise above $1.21 today. That likely marks the near-term range, barring new developments. The euro has lost some momentum against sterling. It is threatening to post its second consecutive loss against the pound, which would be first back-to-back loss in nearly three weeks.

America

Argentina is reeling after the weekend primary votes saw a stunning defeat for Macri, who investors clearly liked. Consider the bloodletting yesterday. Stock valuations were cut nearly in half, bonds lost a quarter, and at one time the peso was off by a third. Pricing of the credit default swaps implies about a 75% chance of a default within five years. It was less than 50% before the weekend vote. We suspect this is an exaggeration and note that at the end of the day, the peso closed down only 14.5%.

| The US July CPI and the API estimate of oil stocks are the highlights of today’s North American session. The CPI is of passing interest. |

U.S. Consumer Price Index (CPI) YoY, July 2019(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

| The year-over-year rates are not expected to change much from the June readings of 1.6% on the headline at 2.1% on the core rate. The trajectory of Fed policy seems more focused on the global headwinds, which appears to be the Fed’s euphemism for trade. Recall that last week the EIA reported its first rise in US oil inventories since the first week in June. The median call is for the rise to be unwound this week with a 1.5 mln barrel drop. September WTI has rallied nearly 8.3% over the past three sessions and is almost flat coming into the North American session. |

U.S. Core Consumer Price Index (CPI) YoY, July 2019(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The US dollar held support near CAD1.3200 for the last two sessions, and short-term participants may see the greenback’s upside as the path of least resistance, at least for another test on the 200-day moving average just above CAD1.3300. The weakness in equities and risk-taking appetites offset the positive impact for the Canadian dollar coming from the rally in oil prices and the narrowing of the US-two-year premium over Canada. It is slipped below 25 bp and finished last month near 35 bp. Argentine news yesterday sparked a surge in the US dollar to nearly MXN19.80 from about MXN19.40. But the door investors were pushing on was already open. The dollar had risen for four consecutive weeks against the peso before the weekend vote. Above MXN19.80 and the market appears to have its sights set above MXN20.00, which has not been seen this year (yet). The Brazilian real was also sold in sympathy with Argentina. The dollar briefly traded above BRL4.0 for the first time in almost three months.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$JPY,Argentina,Currency Movements,EUR/CHF,FX Daily,Germany Consumer Price Index,Japan Producer Price Index,newsletter,U.K. Unemployment Rate,U.S. Consumer Price Index,U.S. Core Consumer Price Index,USD/CHF