Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

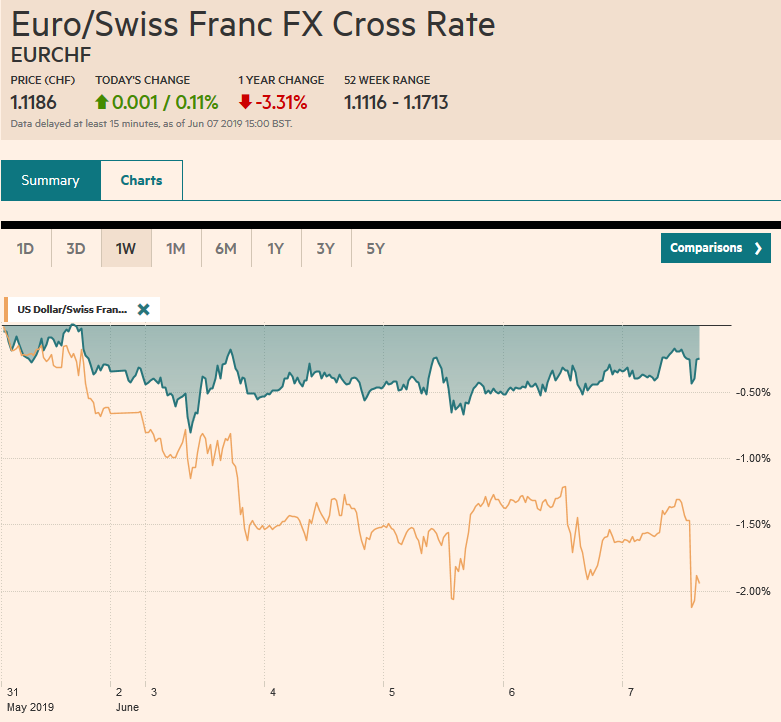

Swiss FrancThe Euro has risen by 0.11% at 1.1186 |

EUR/CHF and USD/CHF, June 07(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Global equities continue to recover from the recent slide. Chinese and Hong Kong markets were on holiday today, but the MSCI Asia Pacific Index eked out a minor gain and ensured that its four-week slide ended. Europe’s Dow Jones Stoxx 600 is up about 0.7% through the European morning. It is the fourth advancing session this week, and ahead of the US employment data, it is up 2% for the week, which is the best in two months. US shares are also trading firmer, and the S&P 500 is bring a three-day rally into today’s session. The 3.3% gain thus far this week puts it on track for its best week of the year to end a four-week spill that began with the end of the tariff truce between the US and China. Benchmark 10-year yields are mostly little changed, but the yield chase is evident in the European periphery, where Spanish and Portuguese yields are off a couple of basis points to new record lows, while Italy continues to play catch-up despite political and financial concerns. Its 10-year benchmark yield is off nearly 8 bp, half of this week’s decline. Italy’s bank share index has not reacted to the rally. It recorded a three-year low yesterday. The dollar is enjoying small gains against most of the major currencies amid what appears to be modest position squaring. Among emerging market currencies, the South African rand is extending the recent drop, and with the dollar rising above ZAR15.0 following S&P’s warning that the troubled power generator Eskom is “too big to save.” The return of the local market in Turkey after the Ramadan holiday has seen the lira for the second day, confirming the end of the 10-session advance. The dollar remains firm (~MXN19.75) against the Mexican peso ahead of last-ditch efforts to avoid the threatened tariffs that are to be implemented after the weekend. A seemingly offhand comment from the PBOC governor that he was not focused on the currency level was seen as a green light to see the offshore yuan (CNH). The dollar jumped about 0.4% (~CNH6.96), which is the largest advance since mid-May. |

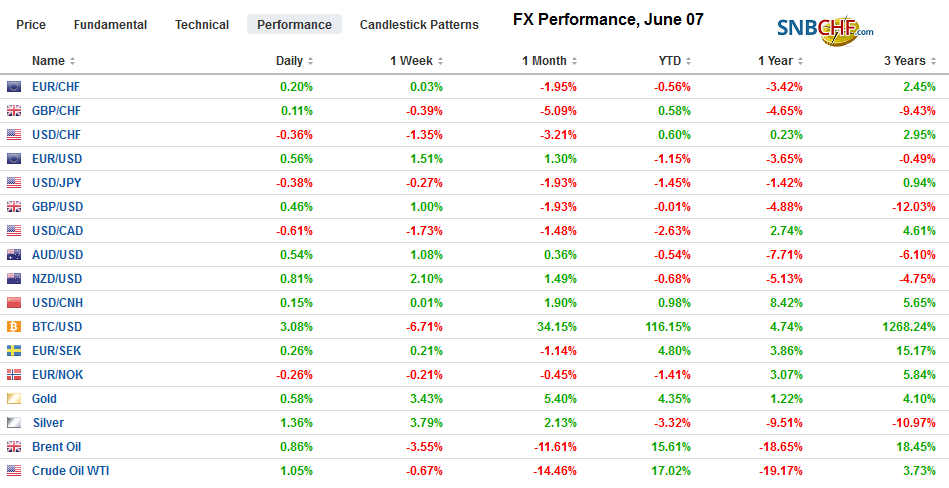

FX Performance, June 07 - Click to enlarge |

Asia Pacific

The US gave the strongest sign to date about a potential meeting between Trump and Xi late this month on the sidelines of the G20 summit. Trump himself said he will meet Xi and afterward decide on whether to implement the next round of tariffs on the remaining Chinese imports of around $350 bln. The issue appears to be, at least in part, whether the US will only accept a grand comprehensive deal, for which the odds seem stuck between slim and none, or a trade arrangement to secure some low hanging fruit. Our attempt to game it out, suggests there is little incentive for Xi to meet with Trump. It would seem to be capitulating to US demands without assurances of success (e.g., no new tariffs and/or terms to reduce current ones. Moreover, the unscripted meeting leaves Xi open to the kind of embarrassment delivered when Trump walked away from negotiations with others. Indeed, by not meeting with Trump, Xi would appear to reassert control of the process. Lastly, China’s policy must be prepared for the punitive tariffs on all its exports to the US. The US has been boisterous on the world stage, and the negotiating tactics that may work in other forums have not generated new agreements, let alone better, with North Korea, Iran, the Middle East, or China. A potential success of a new NAFTA agreement is in jeopardy because due to threatened tariffs on Mexico over migration dispute.

This weekend the G20 finance ministers and central bankers meet in Japan. There is often a statement that is released, but it is not clear that there will be now. The diplomatic speak may not be sufficient to paper over the cacophony of rising economic nationalism and distrust. US Treasury Secretary Mnuchin will meet PBOC Governor Yi Gang. Both are seen as representing the “market” wing of their respective governments. Neither though seems to have the authority to make any agreement through their comments are likely to be promising. Recall that before the US ended the tariff truce on claims that China backed away from negotiated commitments, Mnuchin had negotiated a trade deal a year ago that Trump rejected.

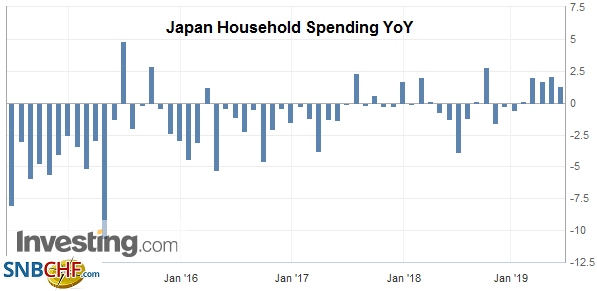

| Japan’s Prime Minister Abe recently reiterated that barring a dramatic crisis, the sales tax would be hiked as planned in October. Despite government efforts to offset the tax increase with some consumption incentives, the economic risks are grave. A key component of income is labor cash wages. Japan reported earlier today that labor cash earnings fell 0.1% year-over-year. They have not risen this year. Adjusted for inflation, real cash earnings are off 1.1%, for the fourth consecutive decline. |

Japan Household Spending YoY, Apr 2019(see more posts on Japan Household Spending, ) Source: investing.com - Click to enlarge |

The dollar finished last week near JPY108.30 and is now exchanging hands around JPY108.50. The less than a quarter of a yen range today will likely be expanded after the US jobs data, but expiring options struck at JPY108 (~$815 mln) and JPY109 (~$1.8 bln) may confine the action. The Australian dollar closed last week around $0.6940 and is now nearly $0.6970, where it has gravitated around over the previous few days. Despite the RBA rate cut and signal that another move is likely, the Aussie has held above the 20-day moving average (~$0.6930) since closing above it last week for the first time since late April.

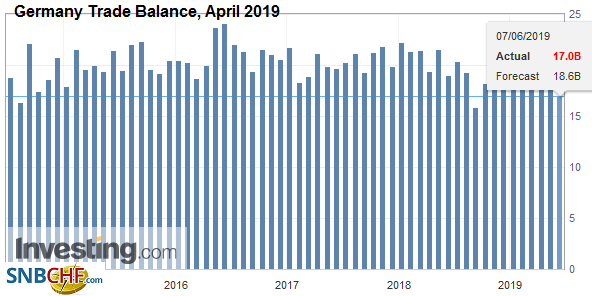

EuropeGerman data disappointed. The 1.9% drop in April industrial output was nearly four times larger than the fall forecast (median) in the Bloomberg survey. Many policymakers and economists complain about Germany’s export prowess, but the 3.7% decline in April shipments is not good news. It is the biggest fall in four years, and most certainly does not reflect reform and increased consumption of its own surplus capacity. Imports fell 1.3%, which of course someone else’s exports. Industrial output rose 0.4% in France. This was a bit stronger than expected but blunted by the downward revision in the March series to -1.1% from -0.9%. However, manufacturing itself was flat after a 1.1% decline in March. The aggregate industrial production figure for EMU will be reported next week. Given the German miss, the eurozone will likely report its third consecutive contraction in industrial output. |

Germany Trade Balance, April 2019(see more posts on Germany Trade Balance, ) Source: investing.com - Click to enlarge |

Although the ECB extended its commitment not to raise interest rates from the end of this year until the middle of next year and recognized that the risks to growth is still biased to the downside, the ultimate takeaway was less dovish. The terms of the TLTRO were not as favorable as they were for the previous tranche, and Draghi’s seemed somewhat optimistic. He does not expect a substantial worsening of the outlook from here, and opined that the economic data “weren’t bad,” and in any event, there was only a low probability of recessions. Some observers had seemed to emphasize that there was no “or lower” reference in its forward guidance, but this had already been jettisoned in the April statement. Draghi did acknowledge that some members discussed lower rates and resuming asset purchases. The importance of this was to give substance to the claim that should it be needed, the ECB stands ready to adjust all of its instruments to achieve its mandate.

The ECB staff forecasts were tweaked, but the precision implied is misleading. After stronger than expected Q1 growth and the recognition that growth slowed here in Q2, this year’s increase was revised to 1.2% from 1.1%, while the CPI forecast was lifted to 1.3% from 1.2%. Next year’s growth and inflation forecasts were shaved: GDP to rise 1.4% instead of 1.6% and CPI rose increase by 1.4% rather than 1.5%. Growth in 2021 was pared to 1.4% from 1.5%, while the CPI projection was left unchanged at 1.6%. The forecasts require some assumptions about the exchange rate and oil prices. The economic estimates assume the euro remains around $1.12 throughout the forecasting period and oil prices generally trend modestly lower from $66.1 this year to $62.7 in 2021.

UK Prime Minister official steps down as leader of the Tory Party today. She will remain Prime Minister until a replacement is found. The first stage is among the members of parliament Starting next week, they will narrow down the first over the next couple of weeks and hope to present the final two candidates to the rank and file members of the party where a vote will be held and the results likely known by the third week in July. Separately, Labour held on to its seat in Peterborough’s byelection. The preliminary count gave Labour 30.9%, the Brexit Party 28.9%, and the Tories 21.4%.

The euro is trading nearly a cent above where it finished last week (~$1.1170). It has been confined to a quarter-cent range thus far today. There are around 3.4 bln euros in expiring options struck between $1.1250 and $1.1275, but the broad range may be defined the 2.7 bln euros in a $1.12 option and 2.1 bln euros in $1.1300-$1.1325. Sterling is firmer for the fifth session of the past six. Since midweek, it has been flirting with the 20-day moving average (just below $1.2720 today), but it has not closed above it since May 7. There is a $1.27 option for about GBP215 mln that will be cut today. The intraday technical indicators warn sterling is stretched.

America

The US has created an average of 205k jobs a month through April. The average in the first four months of 2018 was 220k and the average in the same period in 2017 was 183k. However, the February quirk of only 56k jobs distorts this year’s performance. Although ADP warns of the risk of another downside surprise, other reports, including the weekly jobless claims and non-manufacturing ISM, offer no reason to think the labor market has deteriorated. Given the base effect, average hourly earnings need to have risen by 0.3% to maintain the year-over-year rate of 3.2%. In May 2018, average hourly earnings rose 2.9% year-over-year and 2.5% in May 2017. The workweek has been in a sawtooth pattern alternating between 34.4 hours and 34.5 hours since November. The decline in April was likely reversed in May.

US Job growth in manufacturing has slowed, and manufacturing output has not risen this year. The auto sector has been an important headwind. Through April, it has lost 19.8k jobs, which is more than three times the sector’s job loss in the first four months of 2018. Late last month, Ford announced it would cut 10% of its salaried workforce or around 7000 positions by the end of August. These numbers from Challenger, Gray & Christmas do not include the ripple effect in the parts manufacturers. Note that the 12-month moving average of auto sales and non-farm payrolls peaked in February 2016, which would seem to confirm the maturation of the US business cycle.

Canada reports its May jobs data as well. April’s 106.5k surge was a record. It is unreasonable to expect anything close to this. The Bloomberg survey found a median forecast of 5k. Canada has created an average of 55k jobs a month this year through April. In the first four months of 2018, Canada lost an average of 2.1k jobs. Canada’s 12-month moving average stands a 35.5k, which is the highest since October 2007. Barring a decline in employment in May, the 12-month moving average will likely have made a new cyclical high. The average hourly wage of permanent workers has trended higher this year from 1.49% at the end of 2018 to 2.57% in April. It reached a nine-year peak last May just shy of 4%.

It is not clear whether Mexico’s latest concessions, which appear to capitulate to the demand expressed by US Vice President Pence, according to news accounts, are sufficient to hold off the introduction of 5% tariffs all Mexican imports to the US on Monday. We are concerned that even if the tariffs are not imposed, some damage has already been inflicted. Investors considering relocating from China must think again about the protection that NAFTA gives. It may put at risk the NAFTA2.0 ratification process. Talks are supposed to continue today. Separately, and as a follow-up to their decisions on the sovereign credit, Fitch cut Pemex credit (2nd cut in five months) to BB+ (below investment grade status), while Moody’s cut the outlook to negative.

Last week, the US dollar finished near CAD1.3520, seemingly breaking out higher. It reached the highest level since the very start of the year. Now it is trading near CAD1.3360, having recorded its lowest level since April in the European morning. It has not closed below CAD1.33 since March 1. While much rests on the reaction to the employment data, there are two sets of options to note: There is one set for about $520 mln at CAD1.3400, should there be a significant development, options for $1.2 bln are found between CAD1.3465 and CAD1.3470. The US dollar (~MXN19.7760) is about 0.8% higher against the peso on the week after surging nearly 3% in the immediate response to the tariff threat.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Canada,EUR/CHF,Germany Trade Balance,Japan Household Spending,jobs,Mexico,newsletter,USD/CHF