Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

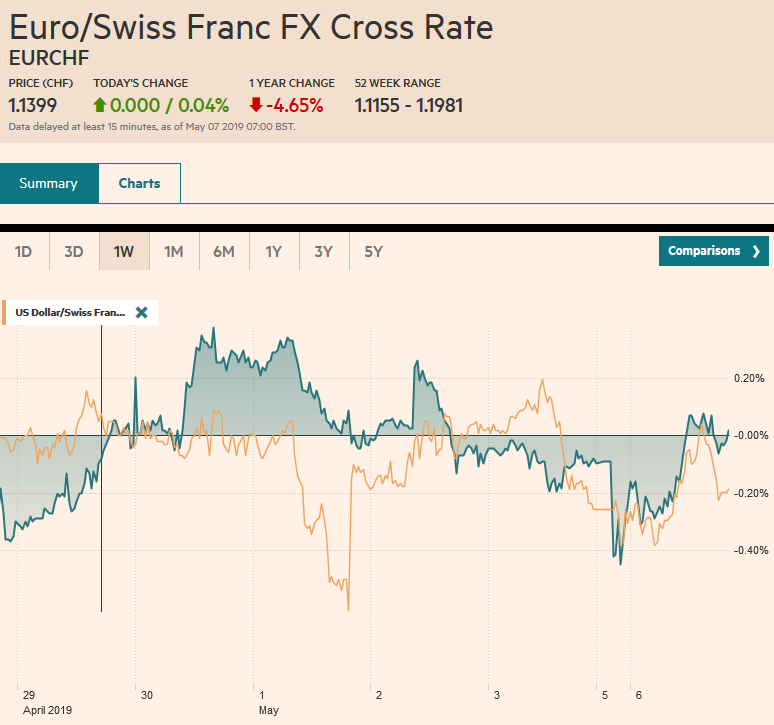

Swiss FrancThe Euro has risen by 0.04% at 1.1399 |

EUR/CHF and USD/CHF, May 06(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Reports that a US-China deal could be struck by May 10 before the weekend left investors ill-prepared for the presidential tweets yesterday that announced that the US was ending the tariff truce. Trump indicated that the 10% tariff on $200 bln of Chinese goods would be lifted to 25% at the end of the week and that the remaining $325 bln of Chinese goods that have not been subject to an extra levy, will be slapped with a 25% tariff soon. Some projections suggest that such a tariff regime would take as much as 1.5% off China’s GDP and around half as much from US GDP. Stocks tanked. The Shanghai Composite fell 5.6% while Shenzhen bled 7.4%. In Singapore, the entrepot, shares fell 3%. European shares trended lower all morning, leaving the Dow Jones Stoxx 600 off more than 1.3%, for its biggest drop in three months. The S&P 500 is called almost 1.75% lower. Bond yields are lower. Australian bonds, where the central bank meets later this week, saw yields tumble five basis points as did China’s 10-year benchmark yield following a targeted cut in required reserves for small banks. European bonds yields were one-two basis points lower, with Italian bonds being the exception. The dollar is stronger against most major and emerging market currencies. The Japanese yen is the chief exception, though local markets will not re-open until tomorrow. |

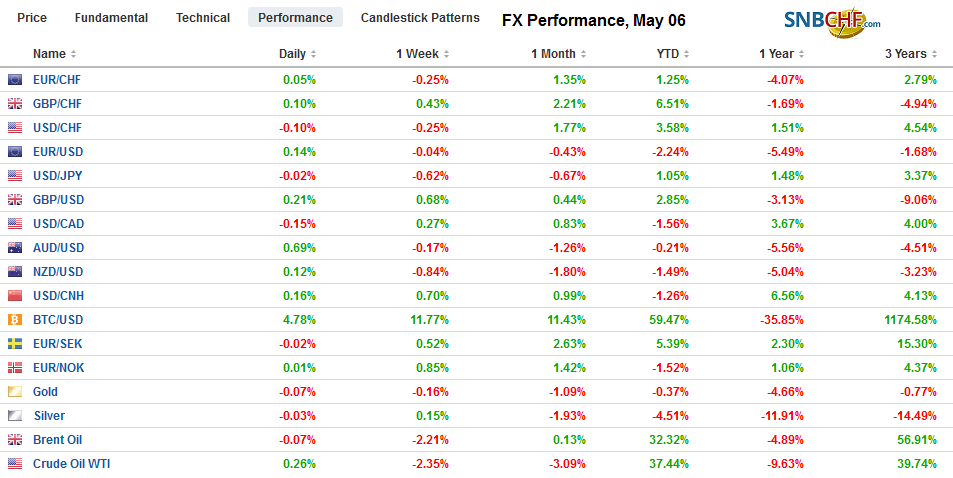

FX Performance, May 06 - Click to enlarge |

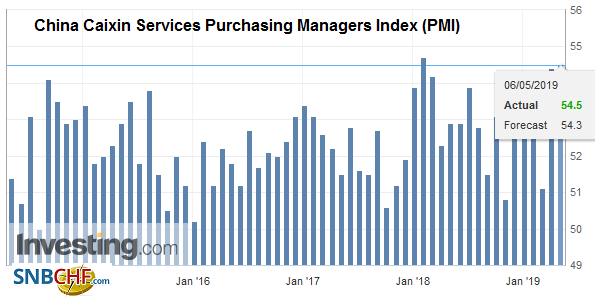

Asia PacificThe US tariff threat is the main news, and it rocked the region, which had seemed like the laggard, especially recently as EMU’s Q1 GDP surprised on the upside. South Korea’s GDP contracted in Q1, and Taiwan’s had slowed. While South Korea’s manufacturing PMI rebounded back above 50 in April, Taiwan’s fell deeper below 50. South Korea’s export orders were at nine-month lows. Singapore’s April PMI stood at 47.3, and its non-oil exports had dropped nearly 12% in March. The market was more inclined to see New Zealand cut rates than Australia, escalating US-China tensions may push the RBA over the edge, and the odds have risen. There have been conflicting press reports about how China will respond. The first issue is whether China’s negotiating team, some 100 strong, led by Vice Premier Liu He, will still come to Washington as planned by the middle of the week. Chinese officials reportedly were blindsided by Trump’s tweets. There is also some thought that US industry may need more than a week to prepare for the hike in tariffs. The targeted required reserve ratio reduction for small Chinese banks is estimated to inject about CNY280 bln (~$40 bln+). US economic adviser Kudlow played up the chances of a US-Japanese trade agreement by the end of the month. The heightened tensions with China may make the US more willing to secure its other markets. However, what seems more likely is that the US wants Japan to grant the same terms for agriculture as it granted to others under TPP and the free-trade agreement with the EU. Trump has a trip to Japan planned toward the end of the month that could provide such an opportunity to sign a deal. Japan, however, has gently pushed back. It does not want a quick deal that will be followed by a longer negotiation. It wants a comprehensive deal now, and it does not wish to be subject to US auto tariffs, which Trump threatens. It wants the steel and aluminum tariffs that have been levied on national security grounds to be lifted. |

China Caixin Services Purchasing Managers Index (PMI), April 2019(see more posts on China Caixin Services PMI, ) Source: investing.com - Click to enlarge |

In unusual price action, the dollar gapped lower to start the week in Asia. Recall the dollar finished last week on its lows, just above JPY111.00. It opened the Tokyo-less Asian session near JPY110.70 and has not been above JPY110.85. It fell to almost JPY110.25 before finding a bid. The lows from late March were set in the JPY109.80 area. Tokyo markets re-open tomorrow. The dollar was around JPY111.50 when its extended holiday began. The Australian dollar was sold down to almost $0.6960 on the initial reaction. It is often viewed as a liquid proxy for China. The $0.6950 level, where an A$1.1 bln option is set to expire today, corresponds to (61.8%) retracement objective of the rally since the flash crash (January 3) low near $0.6740. A close above $0.7000 would be constructive. The dollar jumped from around CNY6.7350 before the May Day holiday to almost CNY6.80 today, a four-month high. The dollar rose 0.7% today against the offshore yuan, which had been trading over the extended holiday.

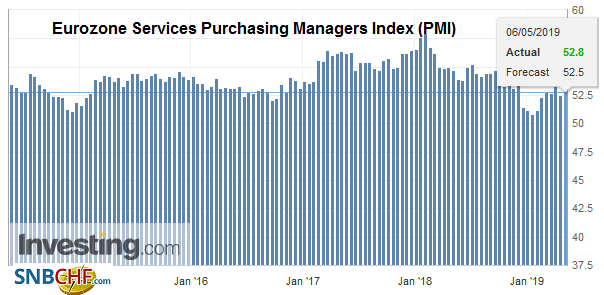

EuropeEuropean markets and currencies have responded to the end of the US-China tariff truce, but local news has been more important for the euro and sterling. The EMU service and composite PMI were in line with expectations while Labour seems cool to May’s latest overture after the stunning results of the local elections. The EMU service PMI edged up to 52.8 from the flash reading of 52.5. Don’t confuse this with an uptick. It stood at 53.3 in March. The decline was a little less than initially projected. This is mostly because of the firmer German showing. Germany, not known for its service sector, saw its PMI firm to 55.7 from the flash’s 55.6 and March’s 55.4. |

Eurozone Services Purchasing Managers Index (PMI), April 2019(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

| The German service PMI is at its best level since last September. Italy and Spain’s service PMIs were lower than expected (50.4 vs. 51.8 and 53.1 vs. 55.1, for Italy and Spain respectively. The composite PMI for the eurozone stands at 51.5, up from 51.3 of the flash report, but still down from 51.6 in March. We see two takeaways. First, the growth in the region is uneven and fragile. Second, the real sector continues to outperform sentiment and survey data. |

Germany Services Purchasing Managers Index (PMI), April 2019(see more posts on Germany Services PMI, ) Source: investing.com - Click to enlarge |

Chastened by another electoral loss, May appears to be now willing to compromise with Labour and is offering a customs-union arrangement that would help resolve the Irish border issue. As Oscar Wilde would have it, there are only two tragedies–getting what you want and not. Like for many of us, the worse thing for Labour is to be given what it wants. It has not been lost on observers that the parties that do well were pro-EU. Reports suggest that in case talks with Labour breakdown, and Parliament votes in favor of a second referendum, the government has already given thought to what a referendum may entail. It might see a three-part offering–the negotiated deal, no deal, no exit.

The euro remains within the weekend range. It was initially sold to about $1.1160 but quickly rebounded toward $1.12, are where it has hovered in rather narrow ranges. There are around 1.8 bln euros in options struck between $1.1150-$1.1160 that expire today. The US market demonstrated after the strong headline jobs data that it was prepared to take some profits on long dollar positions. A move above the pre-weekend high near $1.1205 would confirm the corrective forces are intact. After opening about 2/3 of a cent lower, sterling immediately rallied and took out the pre-weekend high marginally and briefly before gradually returning to its lows near $1.31 in the European morning. There is a modest option (~GBP210) at $1.3105 that will be cut today, but the intraday technical indicators look constructive.

America

In addition to the knock on equities, and the general risk-off moment spurred by the heightened trade tensions, investors have concluded that a Fed cut is more likely. The risk of a cut had appeared to slacken after Fed Chair Powell had suggested that the softness in inflation was temporary. And indeed, as we noted, this week’s April CPI report is expected to be higher for the second consecutive month and back above 2.0% after reaching 1.5% in February. The implied yield of the January 2020 fed funds futures reached 2.115% in the middle of last week. The current average is near 2.41%. It rebounded to 2.265% after the jobs data and is now 2.195%.

While Q1 GDP was stronger than expected, the details were not as good as the optics. In particular, the inventory build was disconcerting. It was followed by the weakest ISM manufacturing report since November 2016, and little-noticed last week, was the sharp drop in April auto sale to 16.4 mln annualized pace, the least in almost two years. Rather than get the Fed to cut rates pre-emptively to help the US fight the trade war, as he had used the bully pulpit to do, Trump now appears to be playing for a cut in reaction to the “cross-currents” he is risking. Several Fed officials speak this week, including Powell, Williams, and Brainard. Of course, there are some differences among the voting members, but there has yet to be a single dissent under Powell. Yellen, in contrast, faced on at her first meeting. The differences seem contextual and, in any event, will not lead to a policy change for several more months, at least. In addition, the president’s public criticism of the Fed may also encourage officials to be particularly parsimonious with dissents for fear that it could be used to undermine the central bank.

The drop in oil prices and the risk-off moment weighs on the Canadian dollar. The US dollar has recouped the ground it lost after the employment report and is back knocking on CAD1.35. It rose above there in late April but did not manage to close above it. Initial support is seen near CAD1.3450. On balance, the CAD1.34-CAD1.35 may contain the greenback near-term. The dollar reversed lower against the Mexican peso ahead of the weekend, but the trade escalation prevents follow-through dollar selling. The recent highs for the greenback have been shy of MXN19.20. It has been up to MXN19.11 today already. Until there is some clarification, the dollar may hold above the MXN19.00 area. However, remember that Mexico is often seen as one of the beneficiaries of heightened US-China tensions. Separately, note that Saudi Arabia indicated it was cutting the price of oil shipped to the US next month while raising its prices elsewhere. WTI for June delivery spiked down to almost $60, which was important support, before rebounding back above $61. Resistance is pegged in the $61.50-$61.80 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Brexit,China,China Caixin Services PMI,EUR/CHF,Eurozone Services PMI,Germany Services PMI,newsletter,OIL,Trade,USD/CHF