Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

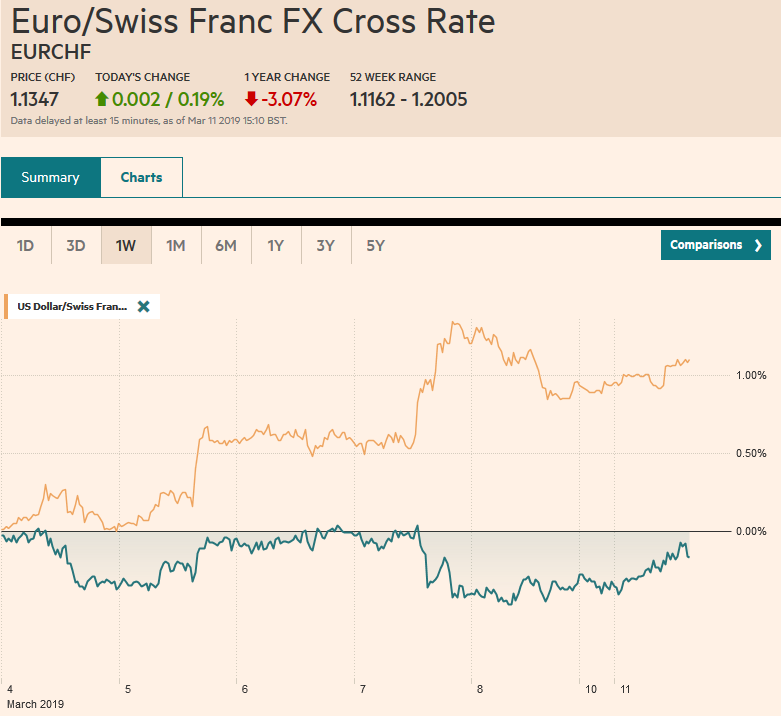

Swiss FrancThe Euro has risen by 0.19% at 1.1347 |

EUR/CHF and USD/CHF, March 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Asian shares recovered from opening losses to finish mostly higher, with the Shanghai Composite up nearly 2% and India tacking on 1% after the election was called, starting April 11. European markets, led by energy, communication, and materials sectors, is up about 0.5% through midday. The S&P 500, which closed lower every day last week is looking a little firmer. Benchmark yields are slightly higher, with the US 10-year yield up nearly three basis points at 2.65%. The dollar is little changed but mostly softer against the major currencies, which makes the Norwegian krone’s 0.8% gain an outlier. It was lifted by a higher than CPI, which boosts confidence that Norges Bank can raise rates when it meets on March 21. The US January retail sales report that is to be released today was highlighted by Powell in over the weekend comments. Auto and gas may have held the headline back, but the components for the US GDP are expected to have risen by around 0.6% after 1.7% plunge in December. |

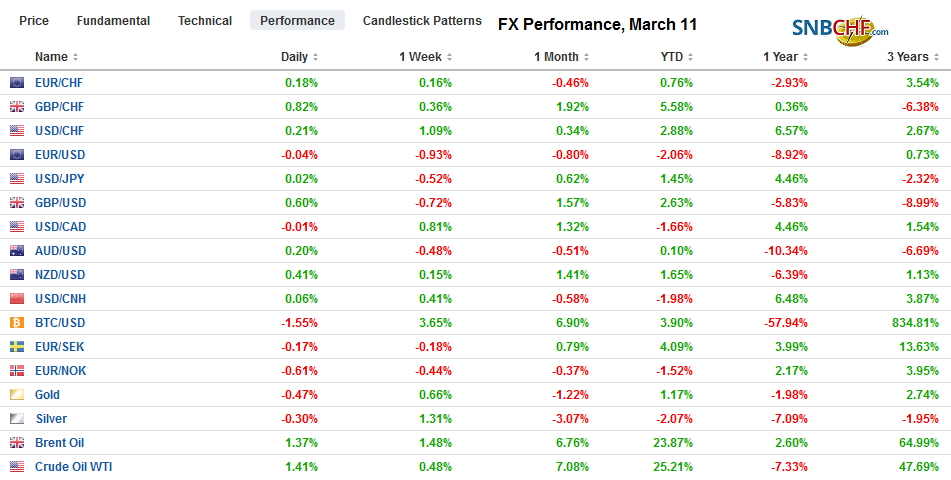

FX Performance, March 11 - Click to enlarge |

Asia Pacific

Chinese data reported over the weekend included a slightly softer than expected PPI and unchanged CPI (1.5%), while aggregate lending collapsed to CNY703 bln from CNY4635 bln.

However, the data is skewed by the Lunar New Year, and a simple average of the two is still elevated. At the same time, the signal is that the de-leveraging campaign that squeezed the shadow banking is over. The drying of credit from shadow banking appears to be one of the factors that weakened companies in the private sector.

The anticipated trip to the US by China President Xi at the end of the month has been postponed. As we suspected the US tactics, with its “take it or leave it” stance with North Korea deters Xi’s without a deal in hand. Yet we have been told that the only way a deal can be struck is between the two leaders. Nearly every day, the press reports talks are going well, and progress is being made. The currency issue itself seems not to be a major stumbling block. China has pledged not to seek competitive devaluations and spent about $1 trillion in reserves trying to keep the yuan stable. The enforcement mechanism was also going to be difficult. China is insisting that it is two-way, fair, and equal, but at the same time respecting the autonomy of each’s monetary policy. Recall that as the US launched QE, some argued that US monetary policy was instigating a currency war.

The Hong Kong Monetary Authority was forced to intervene in the foreign exchange market before the weekend to prevent the Hong Kong dollar from falling through its floor as rate differentials pressured it. It was the first intervention since last August and was seen as modest (HKD1.51 bln or ~$192 mln). The intervention typically squeezes liquidity, making it more expensive to be short. The dollar is just below the HKD7.85 threshold, warning that another bout of intervention is possible.

India has announced elections will be held starting April 11 and running through May 19. Some 900 mln people may vote, about 84 mln more than in the 2014 election. The early polls suggest Prime Minister Modi’s party may secure the most seats, it will likely fall short of a majority. The main opposition party, Congress, won three state elections in December and enjoys some momentum.

The US dollar held last week’s low near JPY110.80 in Asia and has firmed as the flight from risk assets seen at the end of last week ceased. The dollar reached a high in early Europe near JPY111.30. Initial resistance is seen near JPY111.65. The market is unlikely to push the dollar much away from JPY111.00, where an option for about $430 mln expires today, and a billion dollar option expires tomorrow. The Australian dollar is finding a bit better traction. The $0.7000 level held on last week tests. An option struck there today for about A$720 mln rolls off. The Aussie is testing the high from the end of last week near $0.7050. The next cap may be near $0.7080. The dollar edged higher against the Chinese yuan for the seventh consecutive session. Recall that in late February, the dollar slipped through what had been a floor near CNY6.70. We had thought we understood Chinese officials to indicate that yuan appreciation beyond that was not desired. It has now returned to CNY6.72. At the end of 2018, it stood almost at CNY6.88.

Europe

Brexit continues to be center stage. May’s strategy of “running out the clock” (brinkmanship) is playing out. Positions have not changed. Some estimates suggest the Withdrawal Bill may lose by as much as 150 votes tomorrow (Sunday Times). However, the refusal of the EC to show any flexibility is reportedly seeing the rise of those favoring no deal. Moreover, the EC may request a 50% increase the UK funds to compensate for a delay. Meanwhile, should the House of Commons reject the Withdrawal Bill tomorrow and the no-deal exit on Wednesday, the pressure on May to resign is likely to intensify. Lastly, note that that the BOE is requiring some banks to boost their liquid assets to cover 100-day (rather than 30 days) stress of drying up of interbank lending to ensure preparedness in case of a disruptive no-deal exit.

Last week, Spain, Italy, and France reported firm industrial output numbers for January. This fed hope that German numbers would rebound. The median forecast was for a 0.5% gain. Instead, German industrial output fell 0.8%. The saving grace was that the December series was revised to +0.8% from -0.4%. Ironically, this produced the expected year-over-year decline in January of 3.3%, though the December pace was revised to -2.7% from -3.6%. Separately, Germany report exports were flat in January, which was better than a 0.5% decline anticipated by economists after a 1.5% gain in December. Imports had been expected to slip 0.1% but instead rose 1.5% (December’s 1.2% rise was revised to 0.7%). We have suspected that the worst for the German economy has passed, but another month’s of data is needed to boost our conviction.

The euro was pushed below $1.12 last week by the dovish ECB, but the disappointing US jobs data helped the single currency recover ahead of the weekend. It is now testing the $1.1250 area, where a roughly 670 mln euro option is struck that expires today. This remains an interesting area as options for more than 1 bln euros struck there roll off tomorrow and Wednesday. Today, options for around 2.8 bln euros in the $1.1300-$1.1320 area also expire. Before the ECB’s announcement last week, the euro was near $1.1320. Sterling reached its lowest level since February 19 just below $1.2950. The 200-day moving average is near $1.2985. The next technical target is near $1.29, though the mid-February low was a little below $1.28. Before the jobs data, the US dollar had approached last year’s high against the Norwegian krone (NOK8.82), but with the likelihood of a rate hike later this month, the krone has strengthened. The greenback is trading near NOK8.69. Support is seen in the NOK8.63-NOK8.66 area. When everything is said and done, the krone is trading near its 20-day average against the euro.

America

Fed Chair Powell talked twice since the markets closed at the end of last week. We did not see new ground covered. The balance sheet operations are still expected to conclude later this year, with some observers suggesting October. Interest rate policy is in a “wait-and-see” mode, but patience was stressed. Powell formally recognized that the setting was broadly consistent with neutrality.

Fiscal policy is in focus today, as the Trump Administration’s first draft of the 2020 budget will be released. Some of the details apparently have been leaked. The draft reportedly calls for another nearly $7 bln for border security and increased spending for Homeland Security and defense. Cuts in spending on Medicare, food stamps, and EPA are proposed. Meanwhile, the US Treasury will sell over $70 bln in coupons this week to fund the current deficit.

It seems that many, if not most, are taking dismal US jobs growth reported for February with a large grain of salt. The January data exaggerated to the upside and February exaggerated to the downside. The three-month moving average of 186k is probably a more realistic reading and consistent with other economic reports. Today’s focus is on retail sales. Although auto and gasoline sales were likely a drag, a rebound is expected in the components used for GDP calculations. Many economists expect that the US economy may have nearly stagnated or worse at the start of the year–government shutdown and the bitter cold–but with the government re-opening and more normal weather is likely to see the animal spirits return. Manufacturing output later this week is expected to tell a similar story.

The contrasting jobs reports, with Canada creating more new net jobs than the US in February has stopped the Canadian dollar’s slide but has not strengthened it much. The US dollar is consolidating its recent gains and trading above CAD1.34 today. The intraday technicals suggest another try at CAD1.3430 area is possible, but the daily technical readings are getting stretched. The dollar is also consolidating against the Mexican peso just below MXN19.50, having reached MXN19.62, its highest level very early January. Support for the dollar is seen near ahead of MXN19.40.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,FX Daily,MXN,newsletter,Norwegian Krone,SPX,USD/CHF