Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

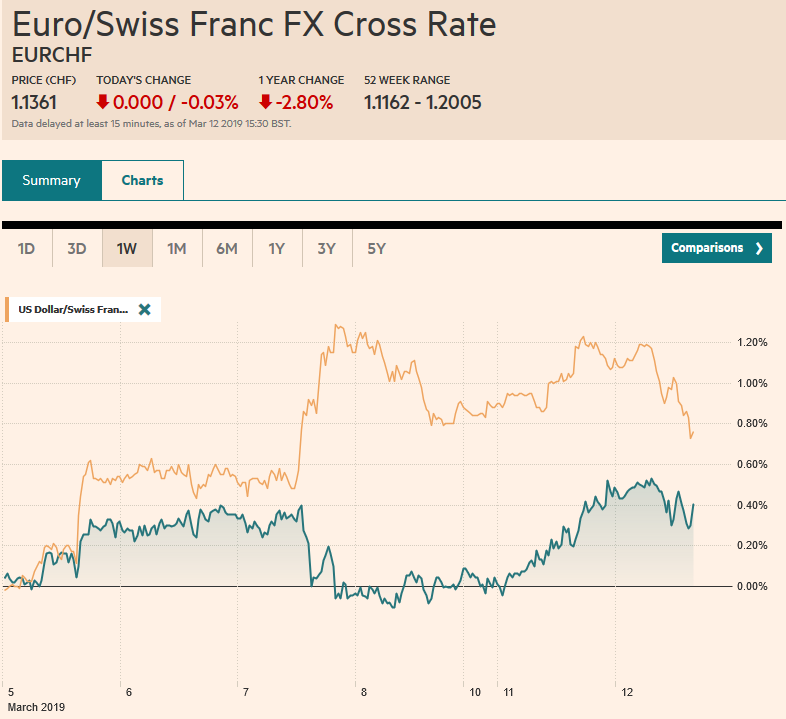

Swiss FrancThe Euro has fallen by 0.03% at 1.1361 |

EUR/CHF and USD/CHF, March 12(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Last minutes statements meant to clarify what many MPs find to be the most odious part of the Withdrawal Bill, the backstop for the Irish border is goosed global equity markets even though it does not seem as if the Withdrawal Bill has changed one iota. And after the big rally in US shares yesterday, there might have been follow-through buying in any case today. Asian markets did not disappoint. Nearly all of the major bourses were up over one percent, and several of the larger indices gapped higher, including the Nikkei, Shanghai Composite, the Hang Seng, Taiwan’s Taiex, and South Korea’s Kospi. Europe’s Dow Jones Stoxx 600 also gapped higher but was trying to fill the gap in the morning session. The three-dollar a barrel increase in the price of WTI the rally in equities appears to be sapping the strength of the bond market. Yields are mostly 1-2 bp firmer. There are a couple of exceptions, UK 10-year Gilt yields are up four basis points, while on the other side of the spectrum Greece’s 10-year yield is a couple basis points softer, even after the Eurogroup of European finance ministers delayed the first post-aid package payout due to lack of performance. The funds are expected to be delivered next month. The US dollar is weaker against nearly all the world’s currencies. Sterling snapped a seven-day slide yesterday traded almost to $1.33 today after dipped below $1.29 to start the week. Among the G10 currencies, the Japanese yen is heavier in the risk-on mood, while the Canadian and Australian dollars are also struggling. Among the emerging markets currencies, the Philippine peso has slid following comments by the central bank governor warned its currency is already strong and seemed to threaten intervention if it got stronger. |

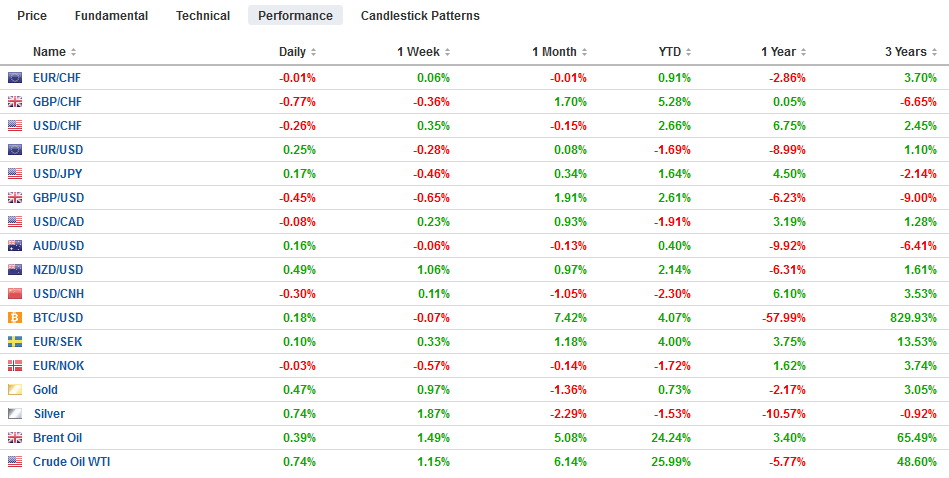

FX Performance, March 12 - Click to enlarge |

Asia Pacific

Weak South Korean trade data for the first part of March showed yesterday continued to show powerful headwinds. However, other reports suggest Asian trade may have begun improving. Earlier today, the Philippines reported that exports fell less than expected. January exports fell by 1.7%, less than half of what economists expected. Imports rose by 5.8%. Economists expected around a 4% decline. Part of the difference seems to be industry specific. In South Korea, for example, semiconductor exports have fallen by more than a quarter, though today, the semiconductor equities turned in a strong showing.

At the same time, Japan does not appear to have emerged from its economic funk. Yesterday Japan reported that preliminary February machine tool orders fell by a little more than 29%. It is the fourth month of double-digit losses and is nearly evenly split between domestic and foreign demand. A survey by the Ministry of Finance found sentiment among manufacturers to be the worst in three years. The Bank of Japan meets later this week. No one expects a change in stance now, but a Bloomberg survey found that 37% expected the BOJ’s next move to be easing policy, more than double the number from January. It is expected that the BOJ lower its outlook for output and exports.

The Australian dollar held $0.7000 last week, perhaps helped by some large options struck there. It is advancing for its third consecutive session and has tested the $0.7080 area, which corresponds to a 38.2% retracement of the decline from late February. The 50% retracement is seen near $0.7100. The real test for the Aussie bears might be in the $0.7125 to $0.7150 area. Today, there is an A$765 mln $0.7050 option. The dollar is continuing to recover against the yen. After falling to about JPY110.80 at the end of last week, it is trading near JPY111.50 today. Last week’s high was near JPY112.15. Options at JPY111.55 for $570 mln will roll-off today. The Chinese yuan strengthened for the first time in nine sessions.

Europe

There is one overriding issue today, and it is Brexit. The House of Commons is scheduled to vote later today on the Withdrawal Bill. There are claims that a new concession was made by the EC, but this is spin. The Withdrawal Bill was not re-open or changed. What has changed is that parts of the Withdrawal Bill are being emphasized to ease fears that the Irish backstop locks the UK indefinitely. However, the Withdrawal Bill does have clauses that spell out conditions on which the UK’s obligations could cease, including if an independent panel judges that the other side is not negotiating in good faith and is seeking to make the backstop permanent. Moreover, as a sovereign power, the UK reserves the right to unilaterally decide on its own to leave the backstop.

The Withdrawal Bill lost by a historic margin a couple months ago. The events markets (PredictIt.Org) are still favoring some kind of postponement. Sterling’s three-cent advance off yesterday’s lows warns of the vulnerability of a defeat of the bill today. If it is defeated, the House of Commons will vote tomorrow on leaving without an agreement. If that too fails to secure a majority, then a vote Thursday will be held to seek an extension.

Separately, the UK reported a series of better than expected data. Consider that January monthly GDP rose 0.5%. The median call was for a 0.2% increase after a 0.4% decline in December. This reflected the 0.6% gain in industrial production and a 0.8% rise in manufacturing output. Both were expected to be up 0.2% after falling 0.5% and 0.7% respectively in December. Construction output rose 2.8% after falling 1.8% at the end of last year. The exception to the better than expected news was the trade balance. It deteriorated, which might have been exaggerated by the quicker UK economic bounce back, compared with some of its main trading partners (see EU and US).

Despite the economic data, sterling continues to pare the gains scored on the initial news of a “deal” and is near European session lows as US dealers return to their posts. There are about GBP555 mln options in the $1.3150-$1.3165 area that expire today but may be in play. There is also almost GBP260 mln at $1.33. Sterling had fallen seven sessions in a row before yesterday. It reached almost $1.3290 today after recording a low near $1.2950 yesterday. The high from the end of February was near $1.3350. The euro is advancing for the third consecutive session. The dovish ECB last week saw the single currency dip below $1.12. It traded near $1.1285 today, just above the $1.1280 strike for nearly 570 mln euros that expires today. As we have noted there are large amounts struck at $1.1250. Today the expiring option is for 1.3 bln euros. Tomorrow there are 1.4 bln euros struck at $1.1250.

America

Over the weekend, Fed chief Powell indicated he was watching the January retail sales data for signs that the consumer bounced back. And they did. Retail sales were well above expectations. The downward revisions to the December series make the bounce back all the more impressive and underscore our sense that the collapse of the world economy at the end of last year was exaggerated. Today the US reports February consumer prices. The median forecast is for a 0.2% increase in both the headline and core rates, which would keep the year-over-year rates steady at 1.6% and 2.2% respectively. The markets may be more sensitive to an upside than a downside surprise.

The US Treasury brings $24 bln 10-year notes to market today. Yesterday’s $38 three-year note sale produced a five basis point decline in the high yield compared with last month, but this did not dissuade investors as the bid-cover was slightly firmer and indirect bidders took 49.5%, up from a little less than 46% last time. The last 10-year note sale saw a high yield of almost 2.69% and produced a bid-cover of 2.35. The indirect bidders took down almost 60% of the issue. The average over the last ten auctions is closer to 63%.

Despite firm equity and oil prices, the Canadian dollar is underperforming. One weight may be coming from interest rate differentials. The two-year spread favors the US by 83 bp. It saw 85 bp last week before easing, but this is really the upper end of where the US premium has been since before the Great Financial Crisis. After shooting up from around CAD1.3150 at the end of February to almost CAD1.3470 last week, the US dollar is consolidating around CAD1.34. Support is seen near CAD1.3350. The US dollar is pulling back from last week’s high near MXN19.62. Initial support is seen today around MXN19.29.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$AUD,$CAD,$CNY,$EUR,$JPY,Bank of Japan,Brexit,EUR/CHF and USD/CHF,newsletter