Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The S&P 500 fell more than 12% in a few weeks. The 10-year Treasury yield fell nearly 40 bp. There were cries that the sky was falling. A recession is imminent, we are warned by prognosticators. The Fed went ahead and raised interest rates on March 21, 2018, and the S&P 500 proceeded to gap lower the next day and continued to sell-off the following day. Investors did not like the unanimous decision. Yet far from the apocalypse, the US economy was on the verge of a growth surge.

As the economy rounded out a 4.2% annualized pace of growth in Q2, the Federal Reserve hiked rates again in mid-June. The S&P 500 at the time was at the upper end of the range seen since the January-February slide (~2800), and again investors did not like the hike and took the S&P 500 down around 3.5% by the end of the month.

The real Fed funds rate was below zero (until H2 18). The economy was growing above trend, the labor market was strong (no need to wade into the weeds to discuss the technicalities of the meaning of full employment), and inflation was near the Fed’s target. On top of this, the federal government was providing a combination of tax cuts and spending increases that surpassed what was delivered during the Great Financial Crisis.

After crying wolf of an impending recession, a year ago, market fundamentalists tell us, again a recession is looming, and the Fed made a policy mistake by hiking rates in December. Many who had been critical of the Fed expanding its balance sheet now want to it reconsider the pace of the unwind.

The US cycle is getting old in the tooth. Weakness in housing, for example, is often associated with late business cycle activity. The 12-month moving average of non-farm payrolls typically peaks in the middle of a cycle, and it appears to have peaked in 2015. However, this does not mean a recession is imminent.

In fact, beginning with last week’s employment data and service PMI, we expect a string of more upbeat US economic data. The ongoing government shutdown will impact some releases, but the general picture in broad strokes we expect to emerge is something like this: October data was poor, but the economy picked up in November. The deterioration in the US trade balance partly reflected a boost in imports to beat tariffs, and the drag on GDP appears to be largely offset by an increase in inventories. The sharp drop in oil prices may push headline CPI below 2% in December, the core measure is expected to remain firm (2.2%).

While the regional Fed manufacturing surveys were weaker in December, and the manufacturing ISM dropped by the most in a decade, two nuggets warn that the headline weakness is exaggerated. First, the new export orders of the ISM rose in December, which is particularly notable given the slowdown among many US trading partners. After falling in October, new exports orders stabilized in November and turned higher in December. Second, manufacturing job growth in last year was the strongest in 20 years, and Q4 was the strongest, and December was best.

If there is a key point that many investors and pundits may be missing, it is the resilience of the US economy. Yes, the economy has lost some momentum, and it feels horrible for growth to be nearly halved, as growth returns to trend, but the expansion is intact.

The same cannot be said for Europe, where ill-winds blow. With the collapse in the price of oil, headline inflation in December was softer than expected, and there is downside risk in the core rate in the coming months. The service sector PMI was dismal. It fell more than the flash PMI suggested as both Germany and France readings were revised lower. France is ailed by an economy that has lost competitiveness (illustrated by the decline in the share of world exports) and is led by an unpopular leader after years of Hollande’s paralysis.

China’s slowdown appears to have hit Germany’s export sector. Investors will get the latest reading on factory orders, industrial output, trade and retail sales in the day ahead. The PMI hint at disappointing data. Merkel’s last years as Chancellor appear safe as her ally took the reins of the party, but she seems to be engaged in a rearguard action to secure her achievements. One success that goes unheralded is the integration of the wave the immigrants into the German economy, and the labor market remains firm. Merkel’s command of the center is contrasted by the AfD, which appears to be trying to breathe fresh life into its movement ahead of the European Parliamentary elections in the spring by considering calling for the unilateral withdrawal from EMU.

United KingdomBrexit continues to loom large. A new debate in the House of Commons will begin in the coming days, with a vote penciled in for January 15. By most reckoning, the bill will lose. A modest defeat could encourage the government’s brinkmanship tactics: block other potential courses and give the House of Commons the choice again next month—May’s plan negotiated with the EC or an unceremonious exit at the end of March with no deal or transition period. The idea is to deny a third alternative, like a second referendum. There is the risk that facing defeat, May could downgrade the vote or postpone it again. At the same time, legislation is still needed to be approved to implement a no-deal exit, and the House of Commons could block it, adding another potential twist to the circuitous plot. The UK reports trade figures, industrial output, and manufacturing, culminating in the November monthly GDP estimate. The broad picture may be similar to the US in that weakness in October was likely followed by stronger activity in November. Still, the uncertainties surrounding Brexit keeps the BOE out of the picture. Some observers were focused on whether the BOJ would intervene to knock the yen back after the flash surge last week, but such concerns were exaggerated. If it did not intervene in the immediate aftermath of those telling few minutes, the intervention would be aimed to reverse the dramatic gains, and this is terribly more difficult to do than smooth out the move. The era of overactive BOJ intervention is over. Also, Abe, who has been careful to avoid antagonizing the mercurial US President or being baited by him, would risk incurring his anger with unilateral intervention. Other countries, including the UK and New Zealand, did not intervene when their currencies were subject to quick sharp moves. |

Economic Events: United Kingdom, Week January 07 - Click to enlarge |

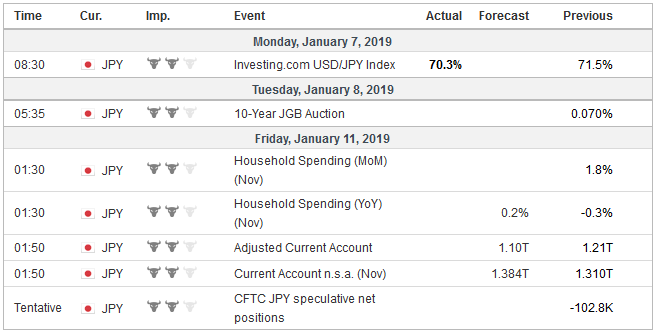

JapanIf intervention in the foreign exchange market is not particularly likely, the BOJ may have had a more telling internal debate about the drop in the benchmark JGB yield to minus five basis points. Previously, the upward pressure on the 10-year yield saw the BOJ increase its range under its Yield Curve Control policy to +/= 20 bp, with the cap understood to be more relevant than the floor. The big jump in US yields ahead of the weekend will likely ease the BOJ’s dilemma. Japan reports labor cash earnings, household spending, and trade figures in the days ahead. The data will likely confirm that the world’s third largest economy returned to growth in Q4 after the natural disaster-induced contraction in Q3. However, the recovery seems unimpressive. Japan’s trade figures offer another reminder of a major change that has taken place. Japan’s current account surplus, like Switzerland’s, is not driven as much by trade as investment income—the yield and dividends from portfolio investment, and profits, licensing fees, royalties, and the like from foreign direct investment. |

Economic Events: Japan, Week January 07 - Click to enlarge |

ChinaChina responded to the contracting manufacturing PMIs with a cut in required reserves that will be implemented in two steps in the coming weeks. Officials continue to take measures aimed at stabilizing the economy. They appear resolved and determined, realizing, among other things, that a weak economy limits the range of options in dealing with the threat posed by US trade actions. The debate continues about who is winning the trade war, but short-termism is coloring the issue. The US trade actions may hurt China in the short-term, but over the medium-term, it will provide incentives to it to move up the value-added chain, diversify its markets away from the US, find new sources of supply (soy?) and reduce its tariff schedule. China is fortunate that a unilateralist is at the US helm. Another may have been tempted to lead a coalition against it. The trade tensions with the US may serve as a powerful wakeup call to China, exposing its isolation. The US is sending a mid-level team to China next week. Investors seem to like talks, but besides claims of progress, little of substance will likely come from it. Instead, the groundwork will be laid for the next meeting. It is difficult to imagine an agreement can be struck by March 1. US Trade Representative Lighthizer has already hinted that it may take more tariffs to get the PRC to agree to more substantive actions. China reports reserve figures, the latest inflation readings, and lending figures. Price pressures are easing. Lending likely slowed, which is why the PBOC is taking measures to encourage it. China’s reserves are expected to have increased a little in December, as the currency’s strength suggests easing of capital outflows. Given that the dollar appears to be around 60% of the PBOC’s reserves, an increase in reserve means that US data may show an increase in China’s Treasury holdings. Early 2018, Chinese officials appeared to draw a line in the sand at CNY7.0. Economic circumstances change, and it seemed like it was de-emphasized. However, once again Chinese officials appear to be citing its significance. |

Economic Events: China, Week January 07 - Click to enlarge |

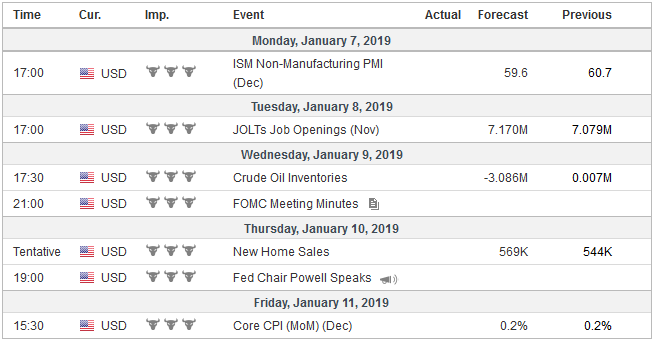

United StatesEquities remain the wild card. The explosive rally before the weekend on the back of the US jobs data, service PMI, and the success of Powell to strike the right chord while not changing the essence of his message will likely help global markets at the start of the new week. Counterintuitively, large rallies are associated with bear, not bull markets. The top dozen advances by the S&P 500 all took place in bear markets (20% decline from the peak), while 21 of 25 of the biggest moves were also in bear markets. The remaining four occurred during 10% corrections. That said, the S&P 500 met the minimum retracement (38.2%) of December’s losses (~2520). The advance ran out of time before the weekend as the 20-day moving average was approached (~2549). The S&P 500 has not closed above the 20-day moving average since December 3. The next target is around 2573, and a push through 2626 would be constructive. |

Economic Events: United States, Week January 07 - Click to enlarge |

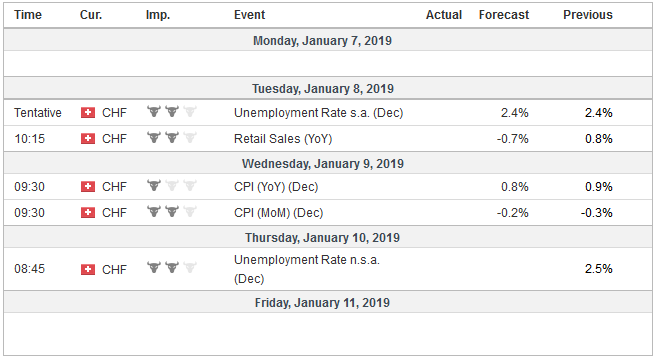

Switzerland |

Economic Events: Switzerland, Week January 07 - Click to enlarge |

Tags: $CNY,Brexit,China,Europe,Federal Reserve,Germany,newsletter,SPX,Trade,U.K.