Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

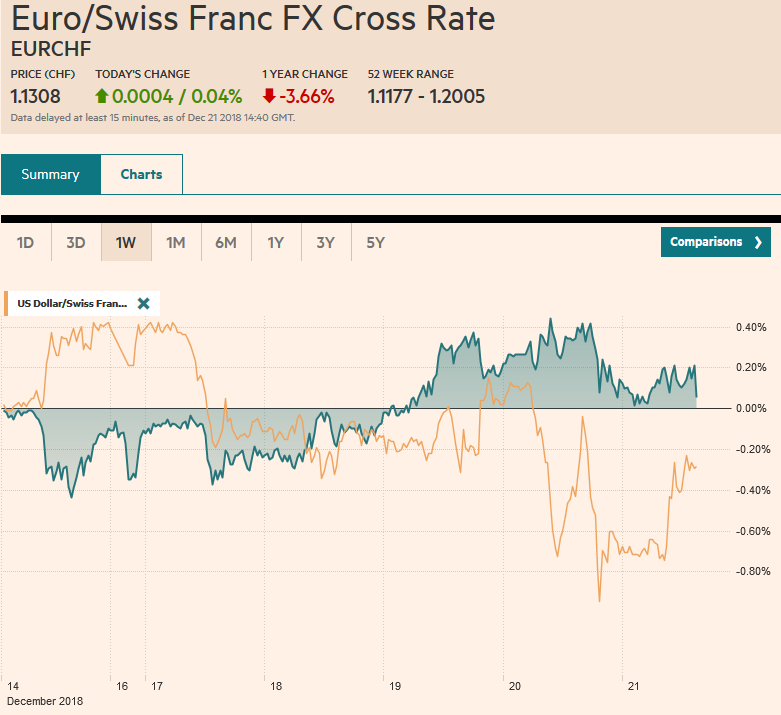

Swiss FrancThe Euro has risen by 0.04% at 1.1308 |

EUR/CHF and USD/CHF, December 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: There is little reprieve from the equity meltdown ahead of the weekend. Major markets in the Asia-Pacific region, including Japan, China, India, and Australia pushed lower. The MSCI index of the region is near 15-month lows. The Dow Jones Stoxx 600 is off about 0.6% near midday in London to make new two-year lows. US shares are also trading lower in Europe. Bonds are not finding much love despite the continued sell-off in equities. This was evident in the US yesterday and in Asia and Europe, where benchmark yields are firmer. The dollar has stabilized against most of the major currencies today, though the yen and sterling are holding their own. The Dollar Index is off about 1% this week, which is what it gained last week. |

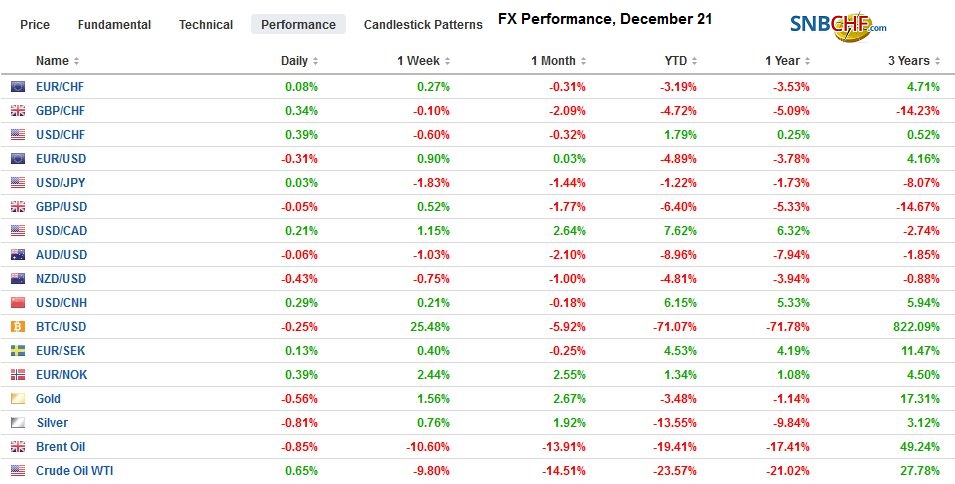

FX Performance, December 21 - Click to enlarge |

Asia Pacific

Japan reported November CPI and the cabinet approved next year’s draft budget, which includes extra stimulative measures to offset the retail sales tax hike next October. Headline CPI fell to 0.8% in November from a year ago. It was at 1.4% in October. The decline reflects mostly the drop in energy. The core rate, which excludes fresh food, slipped to 0.9% from 1.0%. Excluding both fresh food and energy, consumer prices are up 0.3% from a year ago, down from 0.4% in October. The JPY101.5 trillion (~$900 bln) budget increases spending on welfare, public works, and defense. The extra stimulus provided this year, including the new JPY3 trillion spending package, and next appears to be around JPY6.5 trillion to blunt the impact of the sales tax hike that is expected to raise JPY5.6 trillion.

Chinese officials seem increasingly concerned about its economy. They are preparing to offer a TLTRO facility like the ECB, it appears. Specifically, reports suggest the PBOC will build on the medium-term lending facility but offering lower cost liquidity for three years for funds lent to small companies. Many observers expect the PBOC to cut the required reserve ratios at least a couple of times next year. Chinese reports suggest tax cuts and fee reductions will also be rolled out in the coming months.

The dollar neared the technical support we noted yesterday near JPY110.75. It is consolidating the drop today and is holding above JPY111.00. Immediate resistance is seen near JPY111.50, but to begin repairing the technical damage, JPY112.00 needs to be retaken. Several large expiring options are in play. Consider there is around $6 bln in options stuck between JPY111.35 and JPY111.65. There are also about $500 mln at JPY110.75 and nearly three times that amount at JPY111. The Australian dollar is making new lows for the move today (~$0.7070) and is at levels not seen since November 1. While we correctly anticipated the Aussie’s weakness, we had expected it to signal broader gains for the greenback, but this has yet to be seen. The Australian dollar has is off about 1.3% this week, and it is the third weekly decline. The New Zealand dollar has fared a little better but is off 1% this week. It has returned to levels last seen in mid-November. The dollar rose against the Chinese yuan today to snap a four-day slide. On the week, it was virtually unchanged.

Europe

The weekend cannot come soon enough for the battered European markets. The UK confirmed Q3 GDP at 0.6% for a 1.5% year-over-year pace. Separately, but related, it reported a widening of the current account deficit to GBP26.5 bln shortfall from GBP20.0 bln in Q2. The average quarterly deficit this year is about GBP20 bln up from a little more than GBP17.0 bln in 2017. In France, reports suggest that Macron’s moral suasion on businesses to give bonuses appears to be working. Many large businesses are giving bonuses up to 1500 euros. The Yellow Vest demonstrations have already lost some momentum, and the bonus payments seem to be pushing further in this direction. However, the risk is that out of the metropolitan areas, where big business may afford the bonus payments, small business and more rural communities may be excluded, and this is where the Yellow Vest protests of the petrol tax began.

The euro reached its best level yesterday (~$1.1485) since November 7. It is retracing those gains today and has returned toward $1.1400. Support extends to $1.1380. There are also large option expirations today. At $1.14, there are 1.6 bln euros, and strikes between $1.1435-50, hold another 3.2 bln euros. There are also 1.7 bln euros in expiring option between $1.1460-85. Sterling is mostly in a half-cent range below $1.2700, where nearly a billion-pound option will be cut today. There is also an option for about GBP300 mln at $1.2675 that is in play. On the week, the euro is up about 1% and sterling, half as much.

North America

The North American calendar features US November durable goods orders and personal income and consumption data, which contain the Fed’s targeted measure of inflation, the core PCE deflator. There will be practically no evidence in the data that the US economy is on the verge of an economic contraction. In fact, yesterday’s leading economic indicator rose 0.2% in November, and 4.4% over the past six months at an annualized pace. November income and consumption are expected to have risen by 0.3%, which, while slower than October, is still healthy by any stretch. The core deflator is expected to have risen by 0.2% for a 1.9% year-over-year pace. Canada reports October GDP and November retail sales. GDP is expected to have risen by 0.2% for a 2.2% year-over-year pace. Recall that in Q3, the economy expanded, but excluding trade and inventories, final domestic demand fell. Retail sales are expected to have rebounded after 0.2% in October with the help of auto purchases.

The failure of the US House of Representative to allocate more money to fund the wall on the Mexican border that the President insists on could lead to a partial shutdown of the government at the end of the day. Nine departments are vulnerable. The optics and disruption are more significant than the economic consequences. It is political theater.

As widely expected Mexico’s central bank delivered a 25 bp rate hike yesterday. It was expected to hike rates regardless of the Federal Reserve’s decision the day before. The peso is consolidating yesterday’s gains and is finishing higher for the fourth consecutive week and at its best level since late October. The US dollar is up a little more than 1% against the Canadian dollar this week, setting a new high for the year. The greenback has fallen against the Canadian dollar in only one week here in Q4. With the move above CAD1.35 this week, the next important target is seen near last year’s high, closer to CAD1.38.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,MXN,newsletter,SPX,USD/CHF