Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

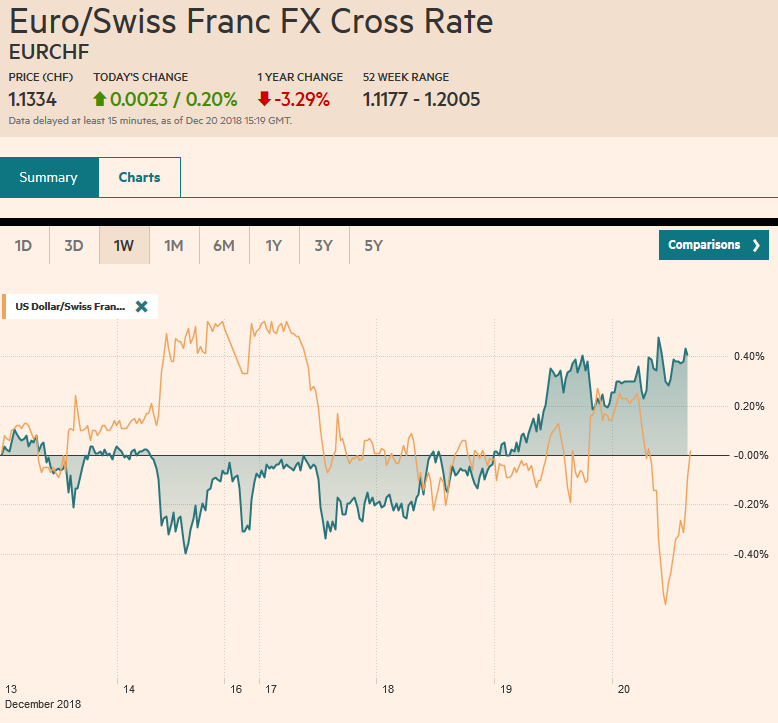

Swiss FrancThe Euro has risen by 0.20% at 1.1334 |

EUR/CHF and USD/CHF, December 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

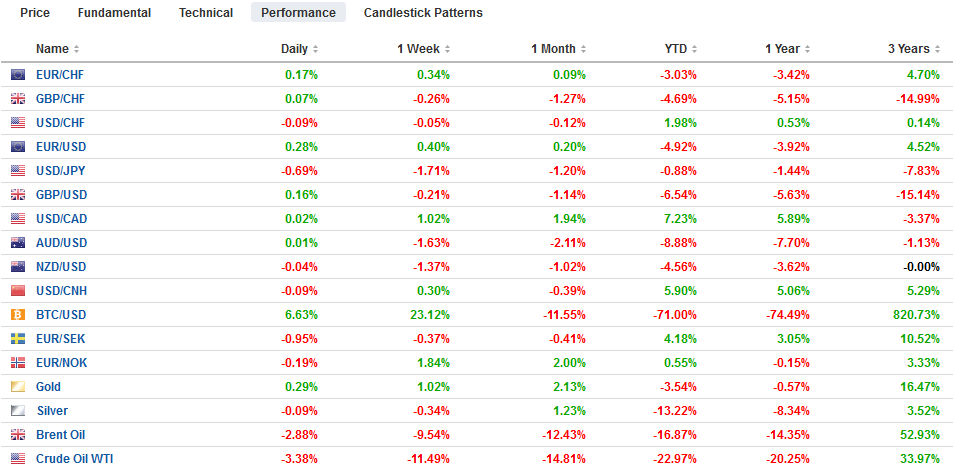

FX RatesOverview: Once again the US equity market failed to hold on to even minimal upticks. The sharply lower close spurred follow-through selling in global equities. Few have been spared the wrath of investors who apparently were disappointed with the Fed and its reluctance to consider stopping the balance sheet unwind. The US benchmark 10-year yield is consolidating yesterday’s drop to 2.75%, a nine-month low, while the 10-year German Bund yield is slipping through 25 bp for the first time in 20 months. Italian bonds, often treated as a risk asset, are leading the yield decline in Europe following the agreement with the EC. Sweden’s Riksbank surprised the market with a 25 bp rate hike, leaving the repo rate at minus 25 bp and signaling the next hike in H2 19. The BOJ held steady as widely anticipated. The outcome of the BOE meeting is awaited, but no change is widely expected as Brexit uncertainty looks large. The US dollar is broadly lower against most of the major and emerging market currencies. The greenback is at two-month lows against the yen and six-week lows against the euro. |

FX Performance, December 20 - Click to enlarge |

Federal Reserve

A common narrative holds the Fed responsible for the Global Financial Crisis for fueling excesses by keeping rates too low for too long in the early part of the noughts. Bernanke and Yellen were often dismissed by the commentariat for being too dovish. Yet for at least the last couple of years, the market has been more dovish than the Federal Reserve.

This was again the case yesterday as the Fed delivered the fourth hike of the year, as the median had indicated was likely to be the case a year ago. It raised the interest on reserves by 20 bp, so the effective cap is 2.40% rather than the top of the target range (2.50%). The most important changes in the economic projections (dot plot) were the median now sees two hikes next year rather than three and the median estimate neutral rate fell to 2.75% from 3.0%. This risks overstating the case, the average forecast for the neutral rate eased 2.84% from 2.88%.

The median GDP forecast for next year was shaved to 2.3% from 2.5%, which is still above its assessment of trend growth (1.9% vs. 1.8% in September). The Fed’s statement appeared to put emphasis on two potential headwinds that speak to many investors’ concerns. By identifying the weakening global growth picture, the Fed recognized that what happens outside the US still impacts it and is determining the appropriate policy. The Fed’s statement also indicated that it was monitoring financial conditions, broadly understood to mean more than a euphemism for the stock market.

The median Fed forecast looks for one hike in 2020. Between the statement, the Summary of Economic Projections, and Powell’s press conference, below trend US growth and/or a rise in unemployment would appear to be the two considerations facilitate an earlier end to the tightening cycle.

The market appeared to have its most dramatic response to Powell’s comments that the balance sheet unwind is practically on automatic pilot and that the Fed funds target is the main tool of monetary policy. In some ways, it is similar to the reaction to the US decision to pull its troops out of Syria. Partly because of the unilateral aspect and what it means for Iran’s confrontation with Israel, many American peaceniks seem to be critical of the decision. Many who were critical of the QE and the expansion of the Fed’s balance sheet, are now critical that it will continue to be unwound.

Some argue that unwinding the balance sheet is tightening monetary policy, but we are not convinced. First, the buying itself did not seem to always ease financial conditions, especially after the initial surprise factor wore off. Second, to the extent the asset purchases worked, arguably there was a large placebo effect or signaling aspect. The Fed said it intended to ease credit conditions. Intentions do matter Now its says do not pay much attention to it. The Fed’s policy signals come from how it manages the Fed funds rate, not from the asset swap (excess reserves for Treasuries and MBS) that inflated its balance sheet.

Many observers are stumped by the Fed’s hike with inflation a little below target and the stock market getting whacked. Yet the decision to hike was not even close. It was unanimous. Arguably Bernanke and Yellen would also have hiked rates. Why? The policy rate is still accommodative and the economic conditions, which can be summarized as above-trend growth and full employment, do not warrant such low rates. While Japan and parts of Europe have negative nominal rates, the US has negative real rates. Given the over-developed US financial markets and the penchant for serial bubbles, prudence dictates a gradual increase in rates.

Asia Pacific

The Bank of Japan did not surprise the market and left policy settings alone. BOJ Kuroda did not seem bothered at all that the 10-year JGB yield is back near zero. Recall that the cap was lifted several months ago to 20 bp from 10 bp. After closing below 21000 support yesterday, the Nikkei gapped lower today and finished at its lowest level in 14 months. The next important level is seen near 20000. Meanwhile, evidence that the Japanese economy is expanding again as it recovers from the natural disaster-led contraction in Q4. The All-Industries Activities Index (a rough proxy for GDP) rose 1.9% in October after a 1% decline in September.

Australia’s jobs data were soft even though the headline of 37k new jobs beat expectations. These were all part-time positions. Full-time jobs fell by about 6.5k (after rising 39.5k in October). The unemployment rate ticked up to 5.1% from 5.0%. This seemed to be a function of the rise in the participation rates to 65.7% from a revised 65.5% (initially 65.6%). The Reserve Bank of Australia is expected to leave policy on hold all next year. Although the central bank continues to insist that the next move is a hike, the market is less convinced.

New Zealand reported half the growth in Q3 that the market expected and the New Zealand dollar is a laggard in the move against the US dollar today. The New Zealand economy expanded by 0.3% in Q3, It follows a 1.0% expansion in Q2. The median forecast in the Bloomberg survey was for a 0.6% expansion. The year-over-year pace slowed to 2.6% from a revised 3.2% in Q2. Separately, New Zealand reported November trade figures, which were in line expectations.

Last week, the dollar was approaching JPY114. Today it has been sold through JPY112.00 and is at its lowest level since October 26. Support is seen in the JPY111.40-60 area, and below there is a technical retracement target near JPY110.75. There is a JPY112.25 option for about $610 mln dollar that expires today but may be too far away to be particularly relevant today. Tomorrow there is a $3.6 bln option at JPY111.50 that will be cut and nearly $2 bln at JPY112.00. The Australian dollar is posting some corrective upticks in the wake of the US dollar’s erosion. A move above $0.7160 would signal a retest on previous support that now may act like resistance near $0.7200. The New Zealand dollar is also recovering from its initial slide. Initial resistance now is pegged near $0.6800.

Europe

Sweden’s Riksbank surprised investors today with a 25 bp rate hike, which lifts the repo rate to minus 25 bp. It last raised rates in 2011. It claimed that with inflation and inflation expectations anchored, the need for extreme accommodation was not needed. It also recognized underlying strength in the labor market. That said, it is in no hurry to remove more stimulus until H2 19. The central bank had indicated a rate hike would be forthcoming either this month or in February. Most expected February. As one would expect, the krona strengthened against both the dollar and euro on the news.

The Bank of England must consider the implications of the UK leaving the EU in 99 days without an agreement as it concludes its meeting today. No change in policy is expected. Yet if it were not for the Brexit risks, the BOE would likely be closer to lifting rates. Previously investors and officials learned that base wages (excluding bonuses) were rising at their fastest pace since the financial crisis. Today, the UK reported a blockbuster retail sales figures. Retail sales jumped 1.4% in November, the second most of the year. The median forecast in the Bloomberg survey was for a 0.3% gain.

The euro is rising for the fourth consecutive session. It is approaching $1.15, which it has not seen since November 7. There is a large (~5.6 bln euro) option that is expiring today struck there ($1.15). Note that there is another significant option even if smaller (1.6 bln euros) at $1.1450 that will also rolls off today. We had expected the euro to pullback after a hawkish hike by the Fed. Apparently, it was hawkish enough to send stocks reeling and long-end yields falling, but not sufficient to lend the greenback support. Sterling found bids near $1.26 and is challenging the 20-day moving average (~$1.27), which, before today, it has not traded above since November 22. The intraday technicals of both euro and sterling suggest the North American operators may find it difficult to extend the dollar’s losses.

North America

The US reports the Philadelphia Fed’s manufacturing survey for December, weekly initial jobless claims and the Leading Economic Indicator. Any disappointment will provide more grist for the Fed’s critics, which seem to be in the majority. The breakdown of US stocks and the outside down day in the S&P 500 and NASDAQ keeps the holiday spirit at bay. The break of the February low near 2580 in the S&P 500 was another blow to the technical outlook. The next technical target is near 2440. In the 10-year US Treasury yield, the 2.75% area is important and convincing break would encourage a test on 2.50%.

Between the drop in oil prices, weakness in risk assets, and the softer Canadian CPI figures yesterday, it is little wonder the Canadian dollar is sitting on its 18-month lows, with the greenback near CAD1.35. Initial support for the US dollar is seen near CAD1.3440, and the intraday technicals favor an initial push higher.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,Federal Reserve,newsletter,SPX,USD/CHF