Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

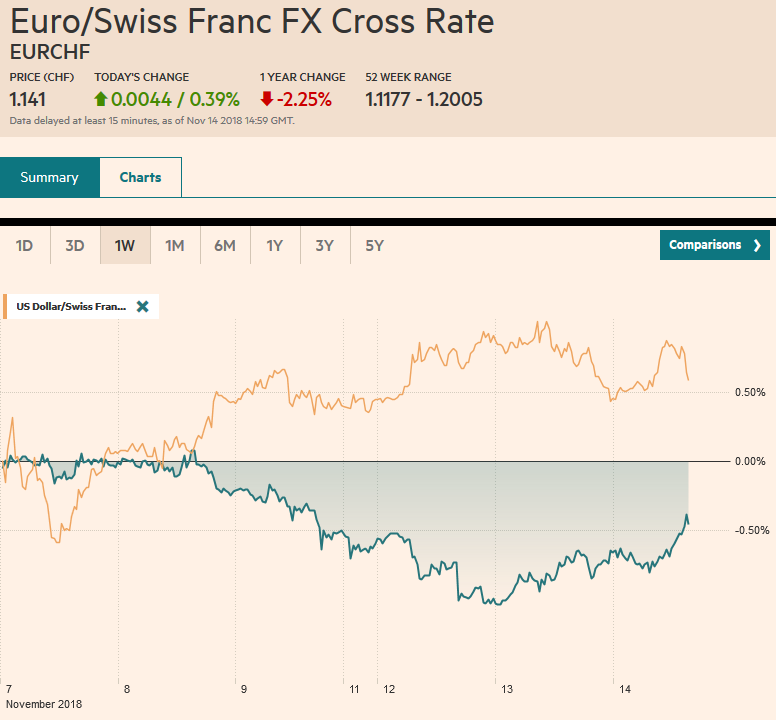

Swiss FrancThe Euro has risen by 0.39% at 1.141 |

EUR/CHF and USD/CHF, November 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Investors are on pins and needles today. Oil prices are trying to stabilize after WTI’s outsized 7% fall yesterday, its largest in three years. Global equities are heavier, dragged down by energy, but also larger than expected Q3 contractions in Japan and Germany, and a mixed bag of Chinese data that showed possible stabilization of the industrial sector though weaker consumption. The economic data, the drop oil, and equities are weighing on yields, but Italy’s confrontation with the EC is spurring a rise in Italian yields. Meanwhile, there is high drama in UK politics as the cabinet will approve the agreement worked out with the EC, and the issue is at what cost (resignations?). It is not clear that the government has the support in Parliament. The US dollar is higher against most of the major and emerging market currencies, but it is not enjoying the momentum that had carried it to new highs for the year at the start of the week. |

FX Performance, November 14 - Click to enlarge |

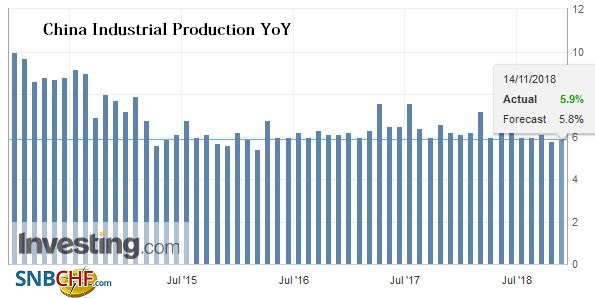

Asia PacificThere are two headwinds on the Chinese economy. There are both domestic factors, like the past tightening of financial conditions, and foreign pressures (tariffs) that are drags. If official efforts to strengthen the economy, investors should expect a mix of data that shows the stabilization of the industrial sector with consumption lagging. And that is exactly what was reported earlier today. Industrial output rose 5.9% a bit more than September’s 5.8%. Fixed asset investment rose 5.7% in October, up from 5.4%. Retail sales slipped eased to 8.6% from 9.2%. It is the weakest since May, and some suggest it may have been held back as some consumers waited for the Singles Day sales (11/11). The yuan is firm but in narrow ranges. After the US dollar tested CNY6.97 in the last couple of sessions, briefly traded below CNY6.95 today. |

China Industrial Production YoY, Oct 2013-Nov 2018(see more posts on China Industrial Production, ) Source: investing.com - Click to enlarge |

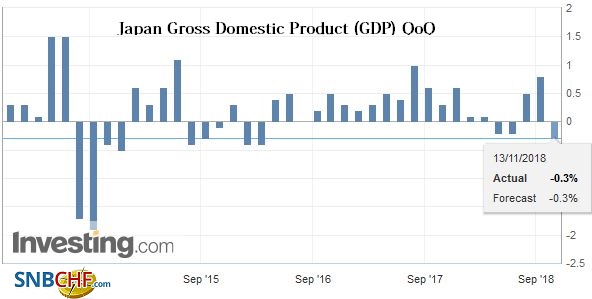

| Japan’s economy contracted 1.2% at an annualized pace in Q3 and 0.3% on the quarter, which was a bit more than expected. Exports (-1.8%), business investment, and consumption all fell in the quarter. This is largely a function of the natural disasters that hit. Data from early Q4, like the PMI and vehicle sales, suggest the world’s third-largest economy is already recovering. For the fifth session, the dollar remains in a narrow JPY113.50-JPY114.20 range. There are $1.3 bln in options struck JPY113.90-JPY114.00 that will expire today.

The drop in oil prices is seen as especially good news in India and helped lift the rupee to its best level since late September. The US dollar rose more than 9% against the rupee from the beginning of the second half through early last month amid concerns that the high price of oil was widening the current account deficit. The greenback poked through INR74.48 on October 11, and today is gapped lower and dipped briefly below INR72.00. However, the short squeeze in the rupee may have run its course. |

Japan Gross Domestic Product (GDP) QoQ, Dec 2013 - Nov 2018(see more posts on Japan Gross Domestic Product QoQ, ) Source: investing.com - Click to enlarge |

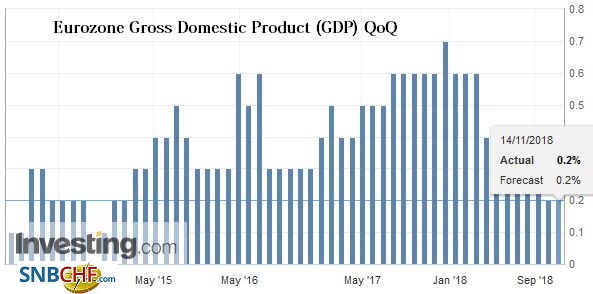

EuropeThe world’s fourth-largest economy, Germany, contracted in Q3. The Bundesbank had warned of stagnation, so the 0.2% contraction was worse than expected. The main problem emanated from the lower auto output related to the change in emission standards. Like Japan, the German economy is already showing some signs of recovery (factory orders, industrial production, and PMI). The preliminary EMU Q3 GDP rose 0.2%, in line with expectations and matches the Q2 pace. Recall the eurozone economy grew 0.7% each quarter last year before slowing to 0.4% in Q1. The ECB seems to view the slowing growth as a return to a more sustainable level, but more worrisome may be the slowing of employment growth. Employment growth slowed to 0.2% in Q3 (1.3% year-over-year) after 0.4% growth in Q2 (1.5% year-over-year). ECB’s Draghi grounded his economic optimism to the tightening of the labor market. |

Eurozone Gross Domestic Product (GDP) QoQ, Q3 2018(see more posts on Eurozone Gross Domestic Product QoQ, ) Source: investing.com - Click to enlarge |

Italy’s government stood fast in the face of the EC’s push back against its budget proposals. It made a minor revision to the amount of money it will raise through privatizations. The Italian government accepts that it is violating the EU rules, but claims that it is necessary because the economy is below its pre-crisis levels. Even if one is sympathetic to Italy’s plight and believe that weak growth is the main culprit that is driving debt ratios higher (as the country continues to run a primary budget surplus), it is not obvious that rolling back pension reforms and lowering the age of retirement, and a new welfare program will boost growth. The tax cut may help, but the concern is that higher rates (from the fiscal stimulus and break-up/redenomination risks) that result offset the benefits. In addition, some economists suggest that government spending in Italy could have a negative multiplier effect (crowding out some private sector initiatives).

The UK has reached an agreement with the EC on the pending divorce. Now comes the hard part. Prime Minister May has to sell it domestically. Today it will go before the cabinet. This will allow a special EU summit to be held on November 25. The biggest challenge will be Parliament’s approval. Here the issue is whether the government can secure sufficient opposition votes to offset the contingent of Tories that are expected to oppose. The government is offering a fait accompli–either the UK-EC way or a disorderly and disruptive Brexit without an agreement. The Brexit drama overshadowed the UK’s inflation report. October CPI rose 0.1% the same as September, leaving the year-over-year rate steady at 2.4%, and the core unchanged at 1.9%. Both input and output producer prices were a little firmer.

The euro bounced higher yesterday after approaching $1.12. It stalled in front of $1.1300 but squeezed up to $1.1320 in Asia today. Monday’s high was just above $1.1330. There is a 1.4 bln euro option at $1.1350 that expires today. On the downside, there is an option half the size at $1.1250 that will be cut. Note that large $1.12 options are expiring over the next couple of sessions. The euro has been sold since the beginning of the European session. Sterling rallied yesterday from nearly $1.2840 to almost $1.3050 on apparently short-covering on the Brexit news. However, it failed to close above $1.30 and is under pressure today and has already given back nearly two-thirds of yesterday’s gains. Given the uncertainties, new sellers may not be too aggressive. Initial support is seen in the $1.2900 area. Meanwhile, the Swedish krona is the weakest of the major currencies. The defeat of the attempt to form a center-right government failed, leaving businesses and investors uncertain of the policy outlook.

North America

The US will report October CPI figures today. It is expected to rise by about 0.3%, which would lift the year-over-year rate to 2.5%. With the fed funds targets below it and growth solid, the case for gradual rate hikes remains in place. Indeed, Fed Chair Powell speaks late today in Dallas and will likely reiterate the point that he and most Fed officials have made. Also late in the session, API will provide its oil inventory estimate, a day later than usual due to Veterans Day holiday at the start of the week. The EIA will provide its estimate tomorrow. In addition to supply issues, OPEC warned yesterday that demand for its oil is likely to fall by as much as 1.5 mln barrels a day next year. The IEA reduced its projections of demand growth from emerging markets next year by about 20%, though the new forecast is for a 1.1 mln barrel increase in demand.

Mexico’s central bank meets and is expected to hike the overnight rate by 25 bp to 8.0%. The decision is announced around 2:00 pm ET. It would be the third hike this year. The reason for the hike is not so much current inflation but rather the weakness of the peso that threatens pass-through pressures. The dollar has risen by about 11% against the peso since the beginning of last month. The central bank is also concerned about the trajectory of fiscal policy under the new government that takes office next month. The dollar is probing the recent highs against the peso near MXN20.40. The year’s high was set in August just below MXN21.00. The technical indicators are stretched, but not yet indicative of an imminent top.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,China Industrial Production,EUR/CHF,Eurozone Gross Domestic Product QoQ,Japan Gross Domestic Product QoQ,MXN,newsletter,SEK,USD/CHF