Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

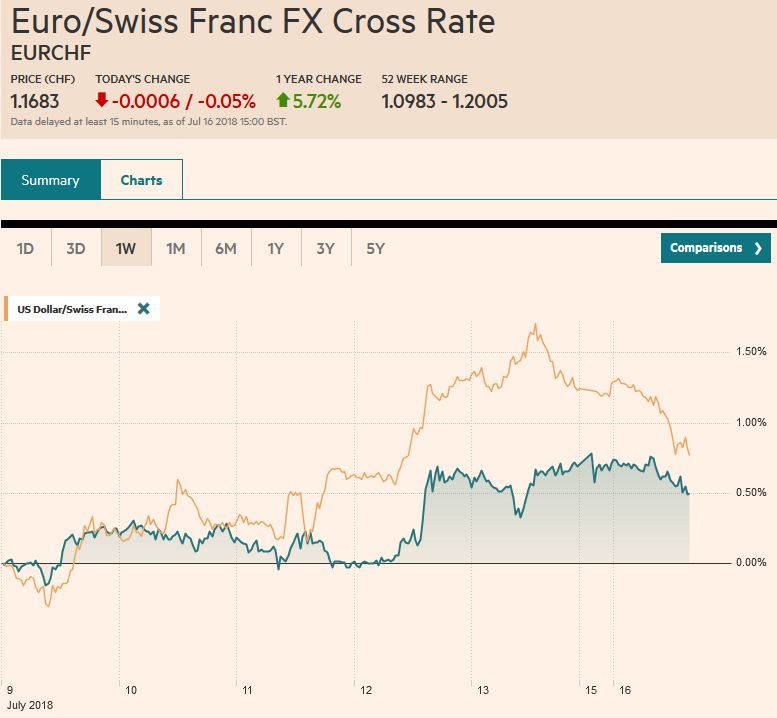

Swiss FrancThe Euro has fallen by 0.05% to 1.1683 CHF. |

EUR/CHF and USD/CHF, July 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is slightly softer against most of the major currencies but is in narrow ranges ahead of today’s key events, which include US retail sales and the debate in the UK parliament over Brexit. The yen is the main exception. The local markets are closed for a public holiday, and the yen did initially strengthen (the dollar eased to ~JPY112.10) but surrendered those gains and consolidating its biggest loss last week in 10 months. Sterling has hardly noticed. It is up about 0.25% near $1.3260, gaining for the third consecutive session. Investors’ attention may shift back to the economic data, barring an unlikely resolution for the UK internal debate, and the big fight might not take place until the fall.The economic data is likely to underscore expectations for a BOE rate hike next month. During this corrective, consolidative phase for sterling, we see potential toward $1.3350-$1.3400. After staging a recovery from two-week lows in the waning hours of last week, the euro has seen some follow-through buying today to lift it to $1.1710. It has retraced half of last week’s decline, and at $1.1725, it would have retraced 61.8%. There are around 1.26 bln euros in options struck at$1.1670-$1.1675 that expire today. There is also almost 730 mln euro in a $1.17 option expiring today. |

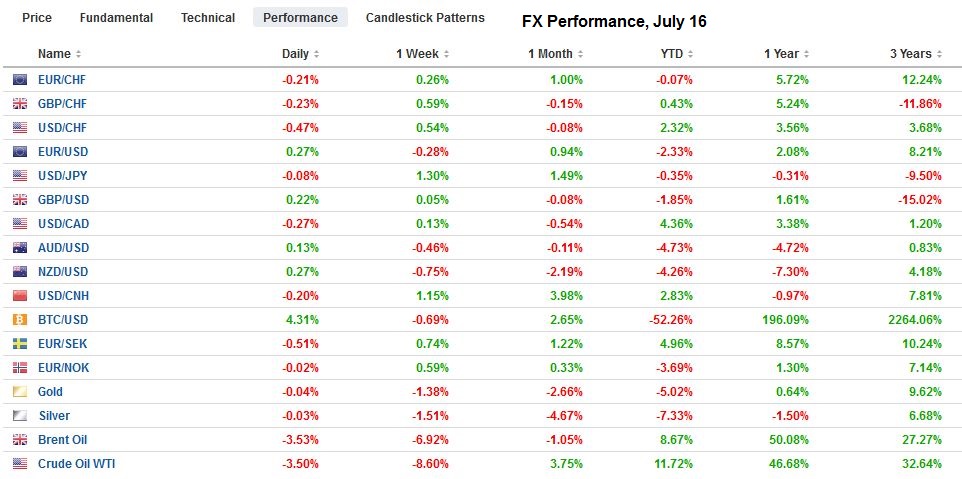

FX Performance, July 16 - Click to enlarge |

ChinaChina’s reported a mixed batch of economic data and this is before much impact from the trade tensions. Q2 GDP rose 6.7% year-over-year, in line with expectations, though quarterly growth appears a bit stronger than expected.

|

China Gross Domestic Product (GDP) YoY, Oct 2013 - Jul 2018(see more posts on China Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| Retail sales held up fine, rising 9.0% year-over-year in June, up from 8.5% in Q1. |

China Retail Sales YoY, Aug 2013 - Jul 2018(see more posts on China Retail Sales, ) Source: investing.com - Click to enlarge |

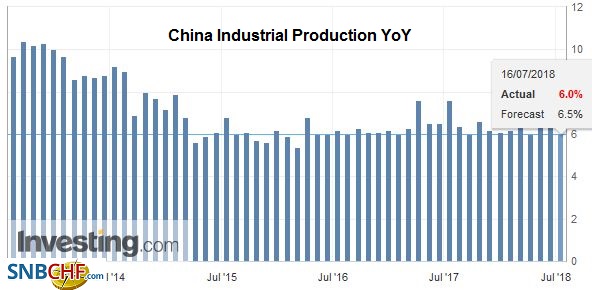

| Industrial production slowed to 6.0% year-over-year from 6.8% and compared with expectations for closer to 6.5%. Fixed asset investment also edged lower; from 6.1% to 6.0%. |

China Industrial Production YoY, Aug 2013 - Jul 2018(see more posts on China Industrial Production, ) Source: investing.com - Click to enlarge |

The UK’s internal Brexit debate is in high drama mode today. Ahead of the debate in the House of Commons, which will debate the amendments by Rees-Mogg which try to undermine Prime Minister May’s new proposals, former Education Minister Justine Greening endorsed a second referendum, she said to break the logjam in the government. Her idea is to offer three choices, May’s plan, no deal, and staying in the EU. Today’s vote on the amendments may provide more insight into the numbers for the hard Brexit camp. Separately, but related, note that two opinion polls over the weekend put Labour ahead of the Conservatives.

The main takeaway and this was also evident in the lending figures from last week, the Chinese economy is in transition. Officials and investors are wrestling with trying to facilitate a deleveraging while not wanting to slow the economy much more. Officials are trying to help the economy evolving toward higher value-added manufacturing and services while minimizing disruption. And now the heightened trade tensions. Still, our larger point should be kept in mind, So far, and including the 10% tariff on $200 bln of Chinese exports to the US, economists estimate the impact on the Chinese economy is about 0.3%-0.5% of GDP.

The PBOC was generous with its money market operation, where it injected CNY300 bln via reverse repos. It is the biggest provision in five months. The dollar initially tested the CNY6.70 level hat has been a bit of a cap this month and softened to about CNY6.67. Chinese shares closed lower but off the session lows. Chinese officials had barred, at least temporarily, mainland investors from investing shares in HK with different voting classes. Still, most markets in Asia finished lower, and the MSCI Asia Pacific, excluding Japan was off 0.3%, snapping a two-day rally at the end of last week that saw the benchmark gain nearly 1.1%.

European bourses are doing a little better. The Dow Jones Stoxx 600 is up about 0.15% in light late morning turnover. It is being led by financials, with the help of favorable news from the EMU’s largest bank. Utilities and industrials are also contributing. Consumer discretionary and telecoms are the laggards. This is the 11th session of the month, and this benchmark has only been down twice. That said, EPFR reports that European equity funds saw $4.2 bln in liquidation last week, the 18th consecutive week of outflows.

The Trump-Putin are unlikely to provide investors with fresh trading incentives, despite the potential for headline risk. Instead, the tone of today’s session may be driven by US economic data and earnings. The Empire State survey is among the first reports covering the start of Q3. Separately, we anticipate a firm retail sales report that will help undergird expectations for a strong Q2 GDP and a recovery in consumption, despite the stagnation of real hourly earnings. Attention then turns of the Fed, where Powell begins delivering his semi-annual testimony tomorrow to the Senate and on Wednesday to the House. The Beige Book, ahead of the August 1 FOMC meeting, will also be released in the middle of the week.

Canada reports it international securities transactions for May. May retail sales and June CPI are the data highlights, and they are due at the end of the week. The US dollar’s bounce fizzled just above CAD1.3200 in the second half of last week. The CAD1.3125 is the 61.8% retracement of the Bank of Canada rate hike bounce. Below that and the target is near the recent low CAD1.3065.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,China Gross Domestic Product,China Industrial Production,China Retail Sales,EUR/CHF,newslettersent,USD/CHF