Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

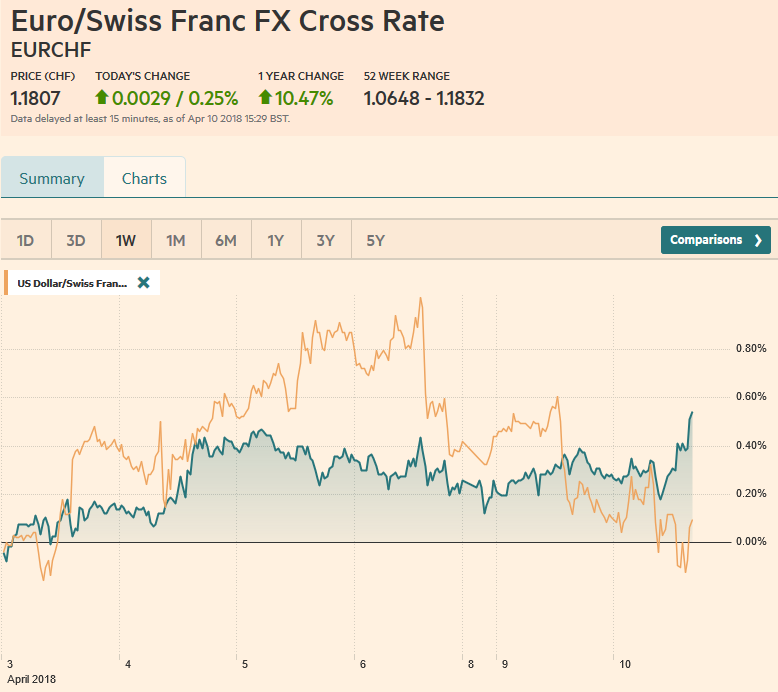

Swiss FrancThe Euro has risen by 0.25% to 1.1807 CHF. |

EUR/CHF and USD/CHF, April 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

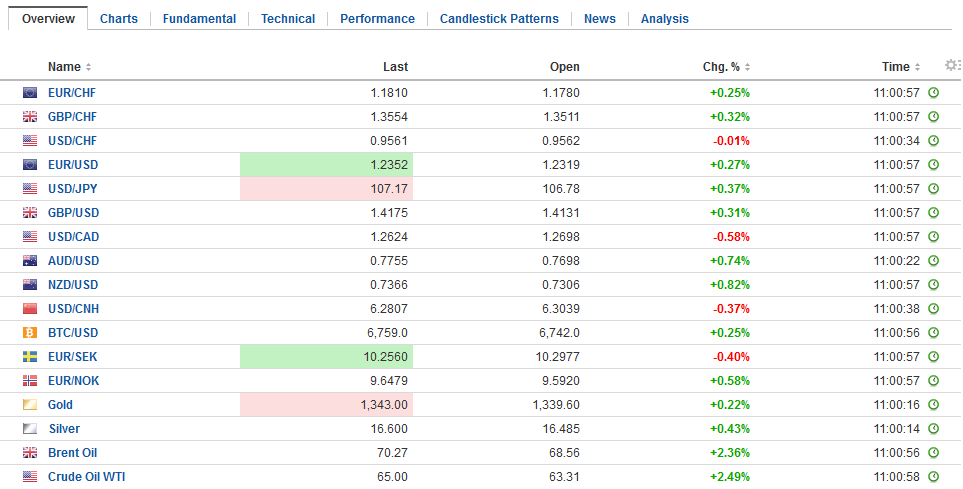

FX RatesIt did not look so good. The S&P 500 fell about 1.65% in the last couple hours of trading yesterday paring its gains. Press reports indicated that President Trump’s lawyer’s office, house and hotel were the subject of search warrants. A Bloomberg report citing people who knew said that China would consider devaluing the yuan. China’s President Xi’s speech at the Boao Forum today hit the right tone today and the market have reacted positively. The MSCI Asia Pacific Index rose 0.75%, the most in two weeks to test the 20-day moving average. It is approaching a trendline drawn off the late January and March highs. Chinese shares, both mainland and that trade in Hong Kong led the region with around a 2% advance. Europe is following suit. The Dow Jones Stoxx 600 is up 0.55% near midday on the Continent, led by consumer discretionary and materials sector. Real estate and utilities are weaker. The benchmark is at its highest level since March 16. US shares are higher in Europe and the S&P 500 is about 1% higher. |

FX Daily Rates, April 10 - Click to enlarge |

| The Canadian dollar posted a big outside day yesterday, trading on both sides of the pre-weekend range and closing well below that low. The US dollar has carved a potential head and shoulders top against the Canadian dollar and the neckline is at CAD1.28. The pattern projects toward CAD1.2475. The greenback is finding some bids today near CAD1.2680.

The euro is building on its pre-weekend recovery from approach on $1.2200. Initial resistance is seen in the $1.2340-$1.2360 area. The dollar has recovered from the JPY106.60 area to resurface above JPY107.00. Nearby resistance is seen near JPY107.50. Sterling, which had dipped below $1.40 in the second half of last week, is pushing closer to $1.4200 today. Last month’s high was near $1.4245 and is the next important technical target. The Australian dollar is trading above its 20-day moving average (~$0.7710) for the first time since mid-March. It has run into offers near $0.7740. |

FX Performance, April 10 - Click to enlarge |

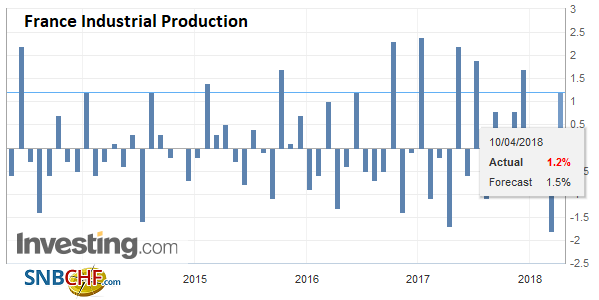

FranceAlthough French industrial output for 1.2% (instead of 1.4% of the survey median forecast), which did not offset the 1.8% fall in January, manufacturing output fell 0.6%. The market had looked for a gain of a similar magnitude. It is the fourth consecutive month that French manufacturing output has fallen. It cannot simply be dismissed as weather-related or a technical issue. Note too that France is being hit by a rolling strike among rail workers that is also a new source of disruption. |

France Industrial Production, May 2013 - Apr 2018(see more posts on France Industrial Production, ) Source: Investing.com - Click to enlarge |

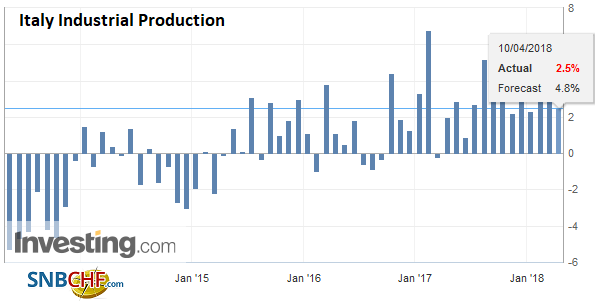

ItalyItaly reported that February industrial output fell 0.5%. The median forecast was for a 0.8% increase, following a 1.8% decline (revised from -1.9%) in January. The workday-adjusted year-over-year rate slowed to 2.5%, the lowest since last April, and identical with last February’s pace. The political backdrop remains unresolved. It had looked like the Five Star Movement was going to form a pact with the Northern League, but its demand to jettison Berlusconi, appears to be proving too big of an ask. Meanwhile, the center-left PD shows no interest in forming an alliance with the Five Star Movement, which ironically seems to share some of its social democratic ideas. |

Italy Industrial Production YoY, May 2013 - Apr 2018(see more posts on Italy Industrial Production, ) Source: Investing.com - Click to enlarge |

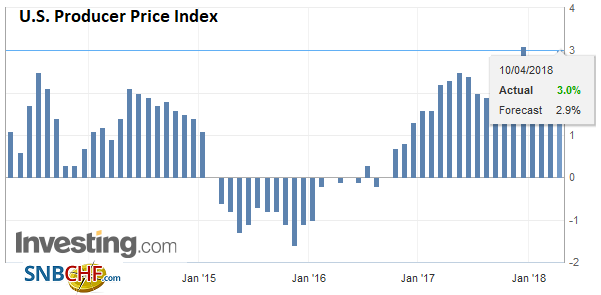

United StatesThe US reports March producer prices and February wholesale sales/inventories. These are second-tier reports even in the best of times. Tomorrow’s CPI is more important, and it could see the first move in the core rate back above 2% in a year, as some of the factors that Fed had identified as transitory drop out. Canada reports housing starts (March) and permits (February). Both likely softened. |

U.S. Producer Price Index (PPI) YoY, Apr 2013 - 2018(see more posts on U.S. Producer Price Index, ) Source: Investing.com - Click to enlarge |

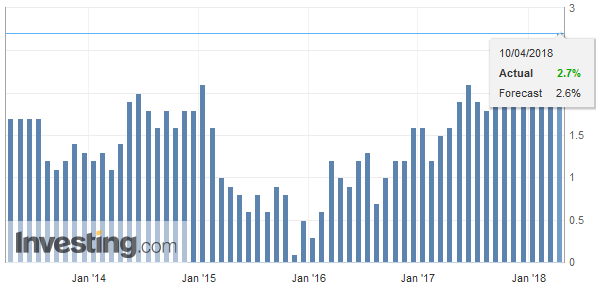

U.S. Core Producer Price Index (PPI) YoY, Apr 2013 - 2018 Source: Investing.com - Click to enlarge |

President Xi did not appear to break new ground, though he announced, “a new phase of opening up.” He suggested China would allow more foreign participation in autos, manufacturing, and banking. That it would do more to protect intellectual property, and expand imports. There was nothing not to like. However, the rub lies not with the declaratory policy but with putting the words in to action.

The US confrontation with China is only partly idiosyncratic. It may be a serious misjudgment if China does not recognize that its emergence on the world stage and its trade practices are of widespread concern. The Trump Administration’s tactics may be off-putting, but the signal and frustration are shared. It is not simply one of few issues that bring together large elements of both US political parties, but as will likely become more evident in over the next week or so, is that Germany, France, and Japan share similar misgivings. That said, a multilateral effort goes against the thrust of the Trump Administration and may require reduced tensions within such a coalition.

The US and China are negotiating and the $50 bln in sanctions initially announced for the intellectual property violations do not going into effect until after a 60-day public comment period. Part of the negotiations are taking place in the public and part in private. Reports about the private negotiations, which may has stalled following Trump’s threat of tariffs on another $100 bln of Chinese goods, saw China willing to take measures to reduce trade imbalance by $50 bln by importing more liquefied natural gas, agriculture, semiconductors, luxury goods, and open the financial sector.

If investors took seriously the risk that China would devalue the yuan, what would they do? We suspect they would sell the yuan, not on the mainland (CNY) where the currency continues to be managed (even if not through intervention) but would express the views in the offshore market (CNH). Today both rose, with CNY edging slightly higher than CNH (0.23% vs. 0.20%).

Russia is not having it nearly as good. The latest US sanctions have dealt Russia a blow. The ruble had been weakening, declining in February and after January’s gain. It gained about 0.5% Q1. The dollar rose 4.2% against it yesterday and another 3.5% today. Both the dollar and local currency bond yields are jumping. The 10-year dollar bond yield is up 28 bp today to almost 5.0% after a similar rise yesterday. The ruble bond yield is up 24 bp to 7.50%, after finishing last week near 7.05%.

Between the latest turn in investigation of Russia’s attempt to influence the US election, and the new unrelated sanctions, and the US-China trade confrontation, most of the economic oxygen has been exhausted. In Europe, both France and Italy reported the February industrial output figures. They disappointed, like Germany did last week, and this give the EMU report (due Thursday) downside risks.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,France Industrial Production,Italy Industrial Production,newslettersent,SPY,U.S. Core Producer Price Index,U.S. Producer Price Index,USD/CHF