Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

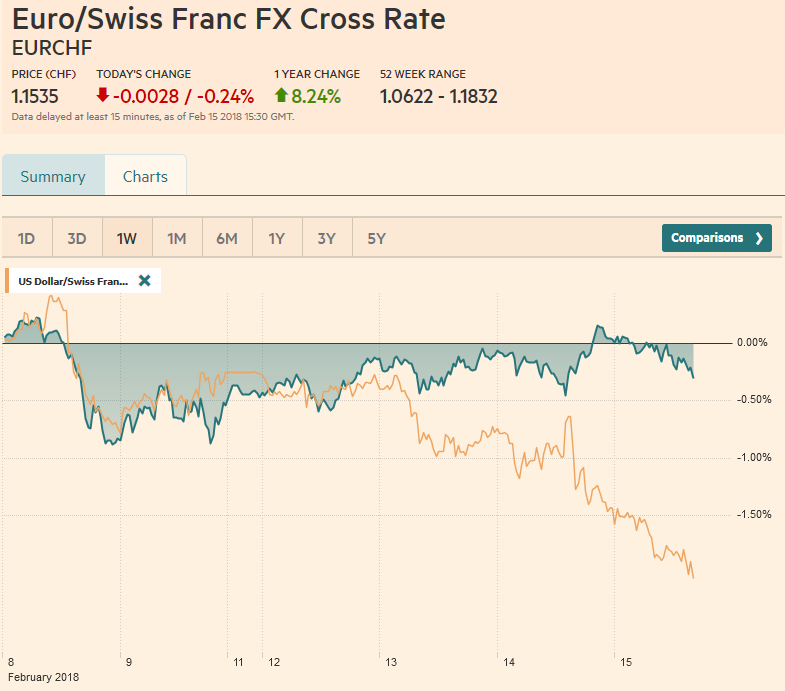

Swiss FrancThe Euro has fallen by 0.24% to 1.1535 CHF. |

EUR/CHF and USD/CHF, February 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe significant development this week has been the recovery of equities after last week’s neck-breaking drop, while yields have continued to rise. The dollar has taken is cues from the risk-on impulse from the equity market and the sales of US bonds more than the resulting higher yields. Asia followed US equities higher. The MSCI Asia Pacific rose 1.37%, though several markets were closed for the Lunar New Year. With today’s gains, it has retraced 38.2% of the drop that began in late January. Unlike yesterday, Japanese stocks held on to early gains and snapped a three-day losing streak. The continuing rise in the Japanese yen runs contrary to the rise in US yields and the rise in equities. Many appear to be switching from yen-funding to dollar-funding, which in turn runs contrary to expectations that higher US interest rates and the Treasury’s issuance a large number of T-bills, now that the debt ceiling has been lifted, increases the cost of that dollar funding. European shares are also advancing. It would be the second gain in a row and the third this week. However, the recover seems muted. The Dow Jones Stoxx 600 peaked earlier (January 23) than the MSCI Asia Pacific (January 29), but the retracement is closer to a quarter than the more than a third. However, some national bourses have outperformed. Italy, for example, has nearly met the 38.2% retracement objective, and remains the best performing G7 equity market this year (+3.8%). |

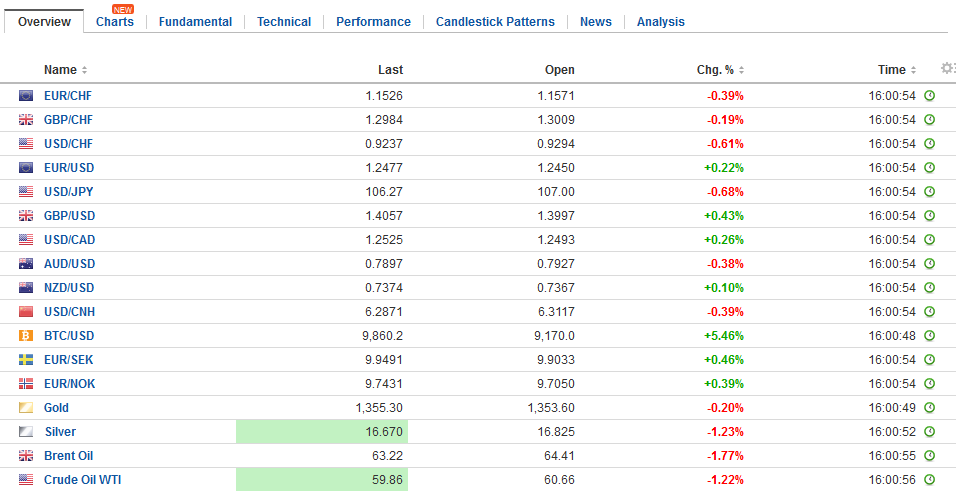

FX Daily Rates, February 15 - Click to enlarge |

| The MSCI Emerging Market Index has recovered best. Today’s 1.5% gain today lifts the weekly advance to over 5%. It is closing in on a 50% retracement of recent loss. This is consistent with at least one broad theme. The recovery from the last week’s equity market drop continues and some of the pre-drop favorites remain favorites.

Last week, the consensus view was the stocks were hit by an interest rate shock. This week, equities have traded higher, while yields continue to rise. The US two-year yield is up two basis points today, making it 11 on the week, and the US 10-year yield is also up two basis points today, and seven on the week. European yields are also mostly higher. The 10-year Bund yield is approaching the 80 bp high seen earlier this month, which was the highest since August 2015. On the other hand, peripheral bonds are in demand. Spain, Portugal, and Greece’s benchmark yields are lower today. Italy’s yield is nearly flat, as the looming election may deter investors from the debt market. While some hedge funds have indicated they are some Italian assets ahead of the election, we suspect, positioning is more complicated. Precisely that which may be the most negative for Italian bond, at least initially, may be good for Italian business and equities. That scenario is a majority win for the center-right coalition. The right-wing of it is talking about renegotiating Italy (and European) debt. While talk of exiting the euro appears to have slackened, talk of a parallel currency is not helpful. The center (Berlusconi) is taking about a flat tax. In this scenario, given the bank ownership of government bonds, shorting bank shares may be one expression. |

FX Performance, February 15 - Click to enlarge |

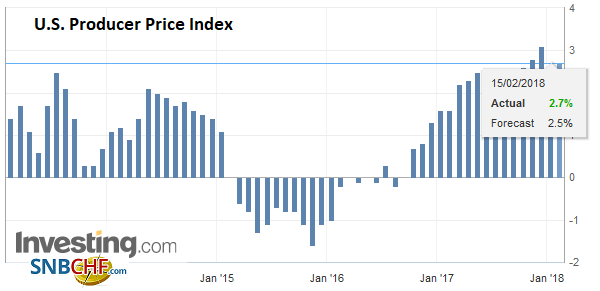

United StatesThe US economic calendar is chock-full today. The weekly initial jobless claims may be of passing interest. They remain near cycle lows. Producer prices likely recovery from the softness in December, but not enough to prevent the year-over-year rate from declining. The Empire and Philly Fed surveys offer earlier insight into February activity. Later industrial production and manufacturing output will be reported. The former is set to slow from a strong Q4 showing and a 0.9% increase in December. The latter may have accelerated from the 0.1% increase at the end of last year. |

U.S. Producer Price Index (PPI) YoY, Jan 2018(see more posts on U.S. Producer Price Index, ) Source: Investing.com - Click to enlarge |

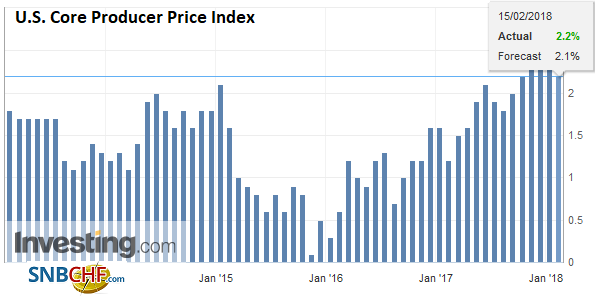

U.S. Core Producer Price Index (PPI) YoY, Jan 2018(see more posts on U.S. Core Producer Price Index, ) Source: Investing.com - Click to enlarge |

|

U.S. Initial Jobless Claims, 15 February(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

|

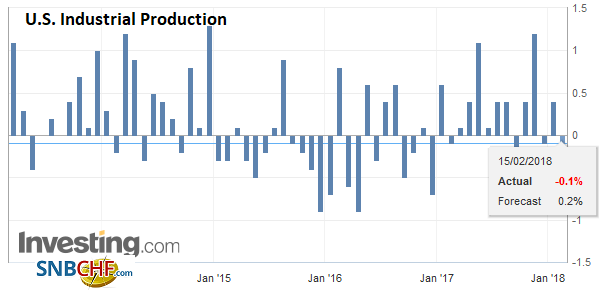

U.S. Industrial Production, Jan 2018(see more posts on U.S. Industrial Production, ) Source: Investing.com - Click to enlarge |

|

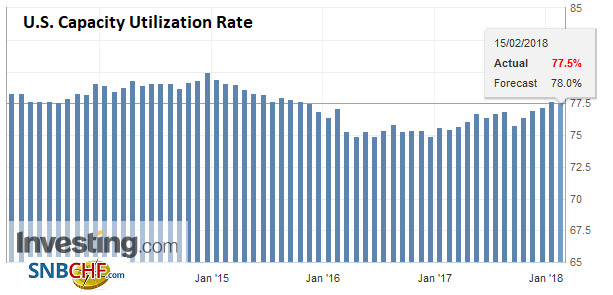

U.S. Capacity Utilization Rate, Jan 2018(see more posts on U.S. Capacity Utilization Rate, ) Source: Investing.com - Click to enlarge |

|

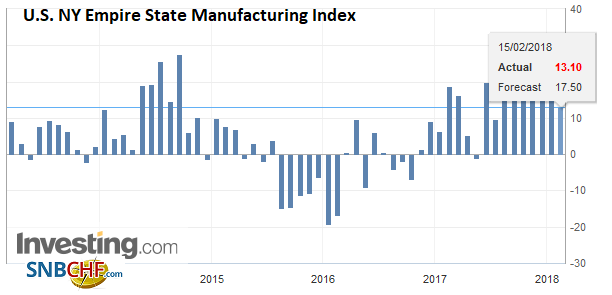

U.S. NY Empire State Manufacturing Index, Feb 2018(see more posts on U.S. NY Empire State Manufacturing Index, ) Source: Investing.com - Click to enlarge |

|

U.S. Philadelphia Fed Manufacturing Index, Feb 2018(see more posts on U.S. Philadelphia Fed Manufacturing Index, ) Source: Investing.com - Click to enlarge |

|

Japan |

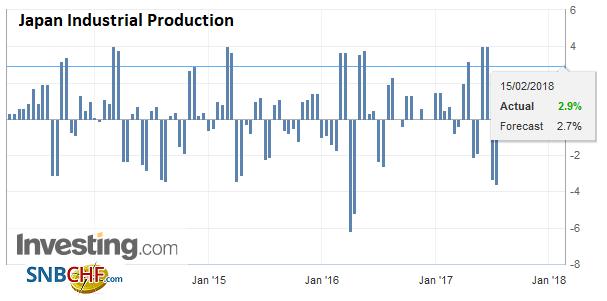

Japan Industrial Production, Jan 2018(see more posts on Japan Industrial Production, ) Source: Investing.com - Click to enlarge |

Japan Core Machinery Orders YoY, Dec 2017(see more posts on Japan Core Machinery Orders, ) Source: Investing.com - Click to enlarge |

|

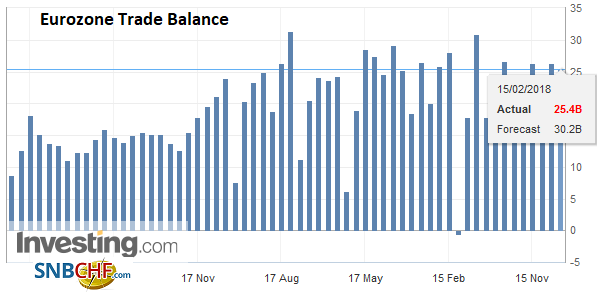

Eurozone |

Eurozone Trade Balance, Dec 2017(see more posts on Eurozone Trade Balance, ) Source: Investing.com - Click to enlarge |

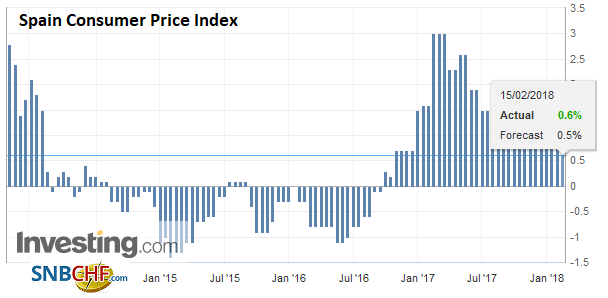

Spain |

Spain Consumer Price Index (CPI) YoY, Jan 2018(see more posts on Spain Consumer Price Index, ) Source: Investing.com - Click to enlarge |

Then, late in the day, the Treasury International Capital (TIC) report will be released. It covers the month of December. We know from the Fed’s custody holdings that foreign central banks that use this facility saw a $27 bln decline in December. The two-time series do not always line up, and the weekly Fed data is weekly not monthly. We note that the Fed’s custody holdings have completely recouped the December decline through the first week this month.

However, the data will likely be of tertiary concern. The key is the stock market. With yesterday’s gains, the S&P 500 retraced 61.8% of the recent drop. That objective is just shy of 2699. It is set to gap higher currently. Last Wednesday’s high near 2727.7 is the next immediate target, though how the market performs around the gap may offer a tell. Yesterday’s high (~2702.1) becomes important support. A push below it, would encourage ideas of an exhaustion gap, suggesting the correction is over. Many who had just discouraged investors from holding cash are now warning of a deeper and broader correction.

The dollar is suffering broad losses. The Dollar Index is within a stone’s throw of the low set in late January (~88.44), which was the lowest level since late 2014. The euro is testing its highs, and poked through $1.25 briefly in late Asia for slipping a little in Europe. The dollar eased to JPY106.20, but has stabilized after the close of the Tokyo markets. The rise of the euro and yen, not just against the dollar, but more importantly on a trade-weighted basis, may not be particularly desirable, but large current account surpluses and an American First agenda in Washington, prevent much official resistance. We saw that in Japan’s Finance Minister Aso’s comments and in the silence of European officials.

Sterling catches a bid, but this seem to be more a case of dollar weakness. The $1.4100-$1.4130 offers nearby resistance. The euro is pulling back after poking through GBP0.8900 yesterday, but the market may not have given up on retesting the upper end of the recent band.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,$TLT,EUR/CHF,Eurozone Trade Balance,Japan Core Machinery Orders,Japan Industrial Production,newslettersent,Spain Consumer Price Index,SPY,U.S. Capacity Utilization Rate,U.S. Core Producer Price Index,U.S. Industrial Production,U.S. Initial Jobless Claims,U.S. NY Empire State Manufacturing Index,U.S. Philadelphia Fed Manufacturing Index,U.S. Producer Price Index,USD/CHF