Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

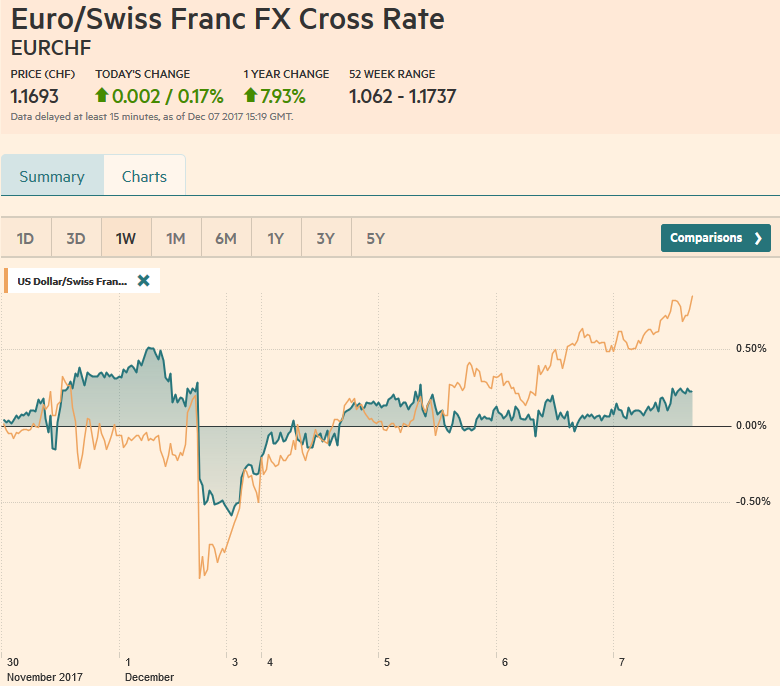

Swiss FrancThe Euro has risen by 0.17% to 1.1693 CHF. |

EUR/CHF and USD/CHF, December 07(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesGlobal equities are stabilizing today after the recent downside pressure. The MSCI Asia Pacific Index snapped an eight-day slump with a 0.4% gain, led by a rebound in Tokyo and India. European markets are firm, with the Dow Jones Stoxx 600 up around 0.25% near midday in London. All sectors are higher but telecom and real estate are performing best, while energy and health care are laggards. The S&P 500 will likely trade higher, at least in early turnover. There was intraday penetration of the 2628 support area we noted, but the index closed back above it. If the recent swoon was spurred by concern that the Alternative Minimum Tax had been retained in the Senate tax reform, then some investors may be more relaxed as several leading Senators, including Hatch, have indicated that it will be dropped in the final bill. The Senate and House have now named the members of the reconciliation committee. While they sort it out, the focus shifts to the spending authorization, which if not renewed, will lead to a government shutdown on Saturday. The House may vote on a measure today to extend the spending authorization until December 22. The Senate may vote on the short-term extension tomorrow. |

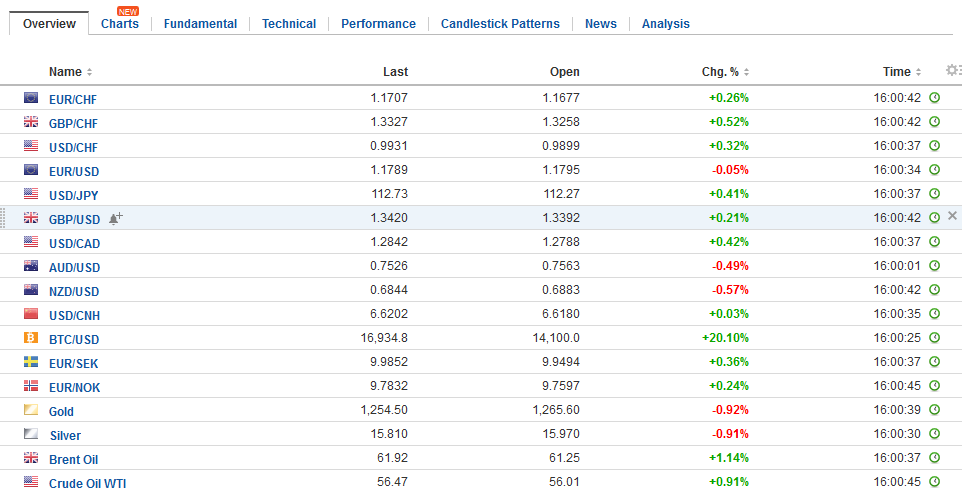

FX Daily Rates, December 07 - Click to enlarge |

| The narrow Republican majority in the Senate may get even smaller if they do not hold on to the seat in Alabama, which will hold its special election on December 12. Consider that the Senate tax bill passed with a one vote majority. The deal that Collins struck over health care reform apparently is not supported by House Speaker Ryan. If she were to vote against the final bill and the GOP loses the Alabama seat, it could jeopardize the tax changes. Separately, Democrat Senator Franken is expected to resign today. The Democratic governor would like ensure the seat stays in the Democrat hands.

Meanwhile, investors await new proposals by UK Prime Minister May. The worst suspicions were confirmed by top government officials. Chancellor of the Exchequer Hammond acknowledged that there has not been a formal discussion by the cabinet of what kind of post-Brexit trade relationship the UK wants. And not to be outdone, Brexit Secretary Davis revealed that there have not been quantitative studies of the impact of Brexit (only qualitative, whatever that really means), and no industry-level study. The dollar held JPY112.00 yesterday and has traded firmer today. At JPY112.65, it is near the middle of this week’s range. Sterling is flat, within yesterday’s ranges. A bounce in late morning trading appears to be more order-driven than data-inspired, and the gains were quickly unwound. The Canadian dollar retain the soft tone seen yesterday after the Bank of Canada meeting, which we did not see as providing fresh news. |

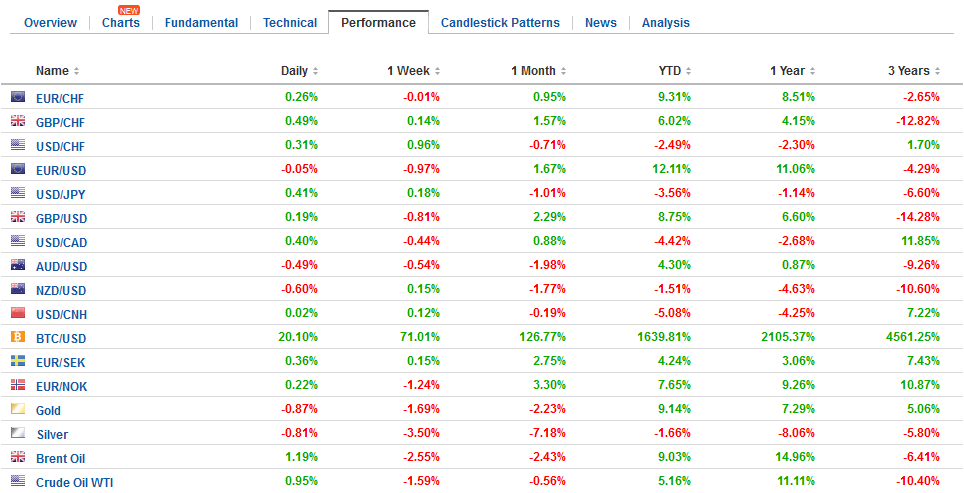

FX Performance, December 07 - Click to enlarge |

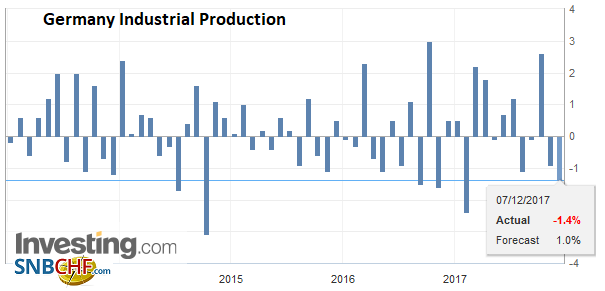

GermanyGerman industrial production unexpected fell for the second consecutive month. Economists had been looking for a rebound after a 1.6% decline in October. October was revised to -0.9%, but the November reading showed a 1.4% decline. It appears that there were some distortions caused by holidays and bridge vacations. Manufacturing output fell 2% led by investment and consumer goods. Energy output jumped 5%. |

Germany Industrial Production, Oct 2017(see more posts on Germany Industrial Production, ) Source: Investing.com - Click to enlarge |

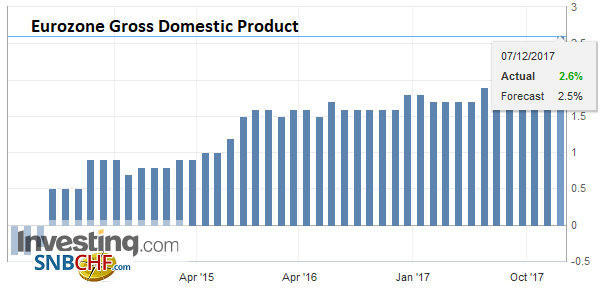

Eurozone |

Eurozone Gross Domestic Product (GDP) YoY, Q3 2017(see more posts on Eurozone Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

United States |

U.S. Initial Jobless Claims, 7 December(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

Nine-months after triggering Article 50, the UK still sees to be without a rudder. It has belated made some progress on its financial commitment, but has made little headway apparently on the rights of EU citizens post-Brexit and the Irish border. And if the first stage of negotiations has been difficult, to say the least, the second stage is unlikely to be much better. UK officials appear not to have given it the level of thought and analysis that even the most adamant Leaver would have rightfully expected. The EU seems to want offer the UK and trade agreement like the one struck recently with Canada. The UK, of course, will want more, even if it does not know it yet.

There are three economic data points to note. First, Australia reported a much smaller than expected trade surplus, which followed the softer Q3 GDP figures that were released yesterday. The October trade surplus was A$105 mln. Economists expected surplus ten-times larger. Imports rose 2% and exports fell 3% on the month. Iron ore exports fell 10% and coal exports were off 3%.

The Australian dollar was punished on the news and it is trading at its lowest level in about six months as it approaches $0.7500. On Tuesday, after strong retail sale, the Aussie ran into a wall of selling near the $0.7655 resistance.

Second, China’s reserve rose for the 10th consecutive month. The $10 bln increase was a bit smaller than expected. Given its continued preference for Treasuries, an increase in China’s reserves often means an increase in its demand for US securities. This may not be the case with increase in November reserves. Given the developments in the foreign exchange and bond market, the increase in reserves is likely a function of valuation adjustment rather than new inflows.

Separately, we note that China’s Sinopec is suing Venezuela’s PDVSA to recover unpaid bills. What is interesting is that the case will be heard in US courts. This follows China’s previous decision to offer dollar-denominated bonds. These developments should give pause to those who think that China can replace the US on the global stage or that the yuan is going to replace the dollar as the main reserve assets in any kind of meaningful timeframe.

After a slow start and narrow ranges in Asia, Europe is pressing the euro lower. It is the fifth consecutive day of lower lows and the fourth session of lower highs. Since violating the November uptrend earlier in the week, the euro has pushed lower. The next immediate target is near $1.1760 and then $1.1710. There are two large option strikes that expire today. One is at $1.1750 (~975 mln euros) and $1.1810 (1.1 bln euros).

Some suggested that the rally in the BA futures was a sign that the market was moving away from a January hike. Color us skeptical. We do not think the market was expected a January hike even before the BOC meeting. And the BA futures are not a particularly useful guide, and the cleaner read, the Overnight Index Swaps showed a somewhat greater chance at 23% vs. 16% previously. We do not expect a hike until closer to the middle of 2018. The US dollar had frayed the lower end of its recent range (~CAD1.2660) earlier in the week and now it’s moving above CAD1.2800. The upper end of the range is seen near CAD1.2900-CAD1.2920.

Lastly, we note that oil prices are stabilizing after yesterday’s nearly 3.0% decline. US oil inventories fell, but gasoline inventories rose more than expected. It suggests that the oil surplus is shifting to a gasoline surplus and this may signal lower refinery demand going forward. Refiners have boosted their operating rates for seven weeks. WTI for January delivery reached nearly $59 toward the end of last week and is now poking back above $56.

Graphs and additional information on Swiss Franc by the snbchf team.

Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$JPY,EUR/CHF,Eurozone Gross Domestic Product,Germany Industrial Production,newslettersent,SPY,U.S. Initial Jobless Claims,USD/CHF