Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

![]() Introduction by

Introduction by

George Dorgan

My articles

My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary

Busiest week of Q4.

Fed, BOJ, and BOE, only the last is expected to change policy.

Flash EMU CPI and US jobs.

Positive developments in Italy, less so in Spain.

The week ahead will be among the busiest in Q4. In this note, we provide a brief sketch of the different events and data points that will shape the investment climate. Given the importance of initial conditions, we will begin with an overview of the current investment climate.

Equity markets continue to rally, helped by strong earnings season, this is particularly true of the developed markets. The MSCI Emerging Markets Index eased for the past two weeks. It had snapped an eight-month advancing streak in September.

To say that European bonds have outperformed the US is that same as saying that the US interest rate premium is increasing. It is true through the entire coupon curve. It is as if both blades of the scissors are moving. US rates are rising and, for the most part, European rates are falling. The US 10-year yield rose through the six-month cap around 2.40%, but finished the week, just above that threshold.

The dollar has been tracking US yields higher since early September. We argued at the time, and still believe, that the dollar’s setback, mostly from late April through early September is best understood as a correction of the dollar’s significant run since mid-2014. The correction was sparked by the easing of the political anxiety that had cast a pall over Europe after UK referendum and Trump’s victory in the US. There was the inflation scare in Europe, doubts about the Fed, and adjusting to the unorthodox US administration.

The dollar’s rebound has caught many short-term participants wrong-footed, and this appears to be contributing to the pace of the recovery. We think the market’s judgment about the end of divergence was premature. We do not expect the balance sheet divergence or the monetary policy divergence to peak until well in 2019.

Now, we turn to the brief description of the key events and data in the days ahead:

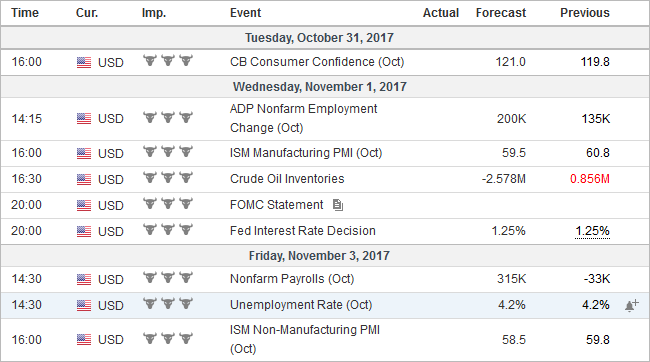

United StatesFOMC: There is no press conference following this meeting, and no change in policy is expected. At the end of last week, the Fed completed the first month of its balance sheet operations. The net seven basis point increase in 10-year yields this month are not seen as a function of the reduction of the balance sheet. The FOMC statement may be shorter with minor technical changes, though its assessment of the economy could be tweaked upward. Market Impact: Headline risk Fed Nominations: President Trump is expected to announce new nominations to the Board of Governors in the coming days. While the focus is on the Chair, the Vice Chair is also open as other two other Governor chairs. For a few weeks, the market has seen Powell as most likely. Chair Powell would not rule out a Taylor Vice Chair. The appointment of Quarles, who will vote at his first meeting on November 1, seemed to diminish the chances of Warsh, who are personal rivals, of getting the nod. We suggest that barring the innovation that is needed in a crisis, the general policy of the Fed is unlikely to change if Yellen is no longer the Chair. Monetary policy is in the process of normalization, and it seems more of a technocratic function than one of partisan politics. Market Impact: Minor, though vulnerable to a surprise. Taylor is seen as more hawkish than warranted, and Yellen more dovish. US Tax Reform: The House Ways and Means Committee is expected to provide the first detailed tax reform bill toward the end of the week. In the coming weeks, it will be debate and “marked-up” in committee. The committee will vote on it, and it will pass. It will then be debated, amended, and voted on by the entire floor. Officials hope to do this before the Thanksgiving break in late November. Market Impact: Even though the initial tax bill will subject to many changes, and the situation is very fluid, there will be winners and losers in the tax reform. The markets will likely respond accordingly despite the not knowing the final version. US Jobs Report: The 33k jobs the US lost in September was not a statement about the economy as the impact of the storms. October’s recovery is expected to be sharp. The median forecast in the Bloomberg survey is for a 310k increase in non-farm payrolls. We suspect the risk is on the upside. Before September, the non-farm payrolls averaged 171k a month this year, and that was the pace over the three months through August. We would not be surprised to see print more than 350k. Market Impact: Participants understand the skewed nature of the jobs report. The market is likely to continue to focus on average hourly earnings data |

Economic Events: United States, Week October 30 - Click to enlarge |

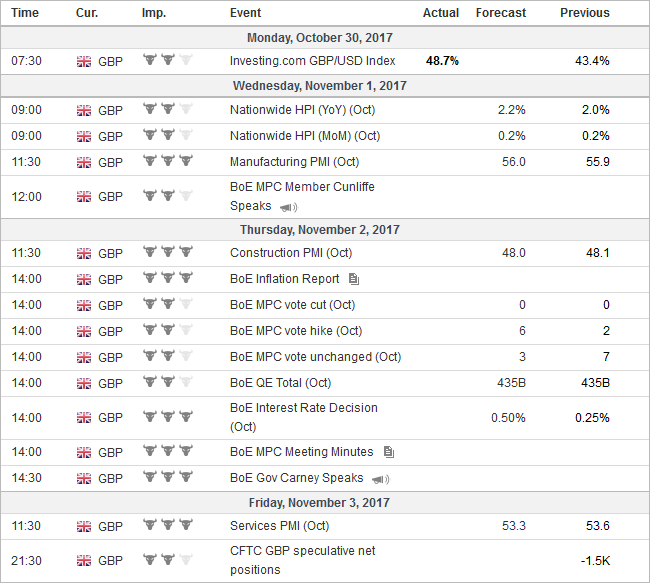

United KingdomBank of England: The market has been more confident of a BOE rate cut than we have been over the past several weeks. We had thought that the combination of slowing growth, expectations that CPI is near a peak, the continued risks associated with Brexit would allow the BOE to remain on hold. During his tenure, Carney has often resorted to hawkish rhetoric without delivering. We expect two-three dissents from a decision to raise rates. Market Impact: As the ECB delivered a dovish tapering, the BOE can deliver a dovish hike. Through its forecasts and minutes, the MPC can suggest that this meant to take back the rate cut delivered after last years referendum. It is not the start of a tightening cycle. Sterling could be sold, but it may depend on the broader dollar direction. We suspect the interest rate market will adjust. It seems out of alignment that the UK two-year Gilt is yielding almost half as much as the December 2018 short-sterling futures contract (46 bp vs. 88 bp). The December 2019 short-sterling contract yields 108 bp. |

Economic Events: United Kingdom, Week October 30 - Click to enlarge |

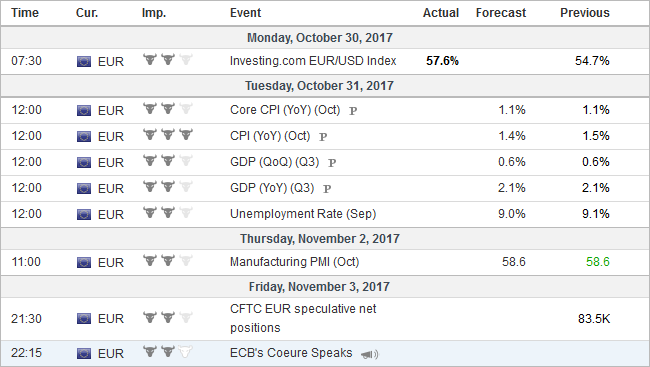

EurozoneEurozone Flash CPI: The ECB announcement of “less for longer” regarding its asset purchases, while keeping all of its other unorthodox measures, steals the thunder for this week report. Perhaps more accurately, it raises the bar to what constitutes a surprise. The market expects little change in CPI. In September, the headline rose 1.5% year-over-year, while the core rate was up 1.1%. Market Impact: Headline risk, but little implication in terms of policy. The market may be more sensitive to a stronger core than headline CPI. |

Economic Events: Eurozone, Week October 30 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week October 30 - Click to enlarge |

JapanBOJ Meeting: The BOJ is not expected to change policy. Headline line inflation is rising at half the pace of the eurozone. The BOJ could shave this year’s inflation forecast of 1.1%. It stood at 0.7% in September. One of the BOJ’s innovations was the yield curve targeting, with the deposit rate set at minus 10 bp and keeps the 10-year yield in a 10 bp range around zero. Its next move could be to adjust its yield curve strategy, and there has been some discussion of targeting the belly of the curve (5-year yields), but that may be a 2018 decision. Separately, the LDP recent electoral victory has bolstered the likelihood that Kuroda gets an unusual second term, according to local surveys. Market Impact: Limited market reaction barring a surprise. The key to the dollar-yen is the US 10-year yield. Meanwhile, foreigners have continued to increase exposure to Japanese equities. There has been strong buying in the four-week period ending October 20, according to MOF data. |

Economic Events: Japan, Week October 30 - Click to enlarge |

Spain: A small window for a de-escalation of Spain’s crisis closed largely it would seem due to the failure of vision and imagination. Puigdemont has played a weak hand poorly. He fell victim to the secessionist sentiment he fomented. Rajoy, leading a minority government, seemed to thrive in the application of power, without mercy. Puigdemont did not prepare Catalonia for independence and failed to secure support from a clear majority of Catalans, let alone a foreign power. Although candidate Trump encouraged the UK to leave the EU, the US quickly endorsed the territorial integrity of its NATO partner. Parliament has authorized invoking Article 155 that strips Catalonia of its autonomy. A new regional election is scheduled for early December. Even if the party representation in parliament is not significantly changed, it will likely move away from secessionist efforts. Spain can still move in a more federal direction.

Market Impact: Spanish 10-year bond yield rose more than five basis points before the weekend, but at 1.57%, it is more than 20 bp below the October 5 high. If anything, political crisis will serve as a mild economic headwind.

Italy: Two developments took place before the weekend that could lift Italian asset prices at the start of the new week. Italy’s sovereign rating was unexpected upgraded by S&P to BBB from BBB-. A politically-motivated attempt not to give Bank of Italy Governor Visco a second term was successfully repelled. The upgrade brings S&P to where the other two main rating agencies put Italy. S&P had regarded Italy’s sovereign risk one step above junk, and the rating increase is a positive development. It is the first the S&P has given Italy in three decades. The reasons it cited are also instructive: stronger growth outlook, better employment, and improving banking sector. Earlier this month, the Bank of Italy indicated that the banking system insolvent loans had fallen to three-year lows.

Market Impact: Italy’s 10-year bond yield has fallen 30 bp since earlier this month through the pre-weekend low, which approached the 1.90% area which has been a floor since January. However, with a roughly 60 bp premium over Spain, there is scope for additional outperformance. The Italian premium over Germany, however, is already near the least of the year (~150 bp). Further significant outperformance may be difficult to sustain. Italy’s FTSE- MIB set new two-year highs before the weekend but settled poorly. The bank index, in particular, was weak, losing nearly 1.7%. There may be scope for better a better performance.

Oil: Brent oil traded above $60 a barrel before the weekend, a level that has not been seen in a couple of years. US WTI reached an eight-month high near $54. Saudi Arabia signaled its agreement to extend the output restraint beyond next March, and the supply disruption from Iraq-Kurds continues to pinch. Strong global growth reports (PMIs) were also constructive. Several large oil companies reported earnings. Exxon and Chevron reported lower output than expected, while Total reported its best oil and gas earnings in a couple of years.

Market Impact: WTI for December delivery closed strongly with a 4% gain on the week. It is especially impressive given the appreciating dollar. It is the third weekly advance and a higher close for the eighth week of the past nine. The pace of the move has left the technical indicators stretched, and near-term consolidation is likely. However, the medium-term outlook looks constructive, and we target $58 in the coming weeks.

Are you the author?Tags: #GBP,#USD,$EUR,$JPY,$TLT,Italy,newslettersent,OIL,Spain,US