Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

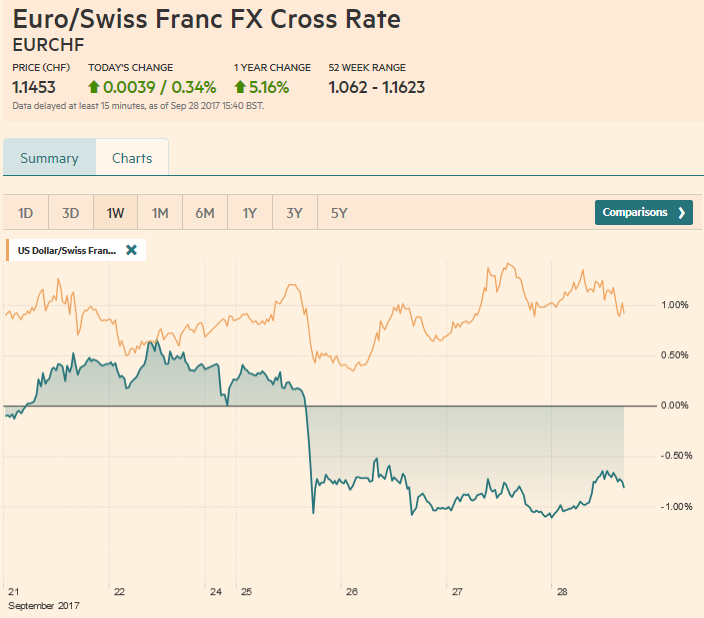

Swiss FrancThe Euro has risen by 0.34% to 1.1453 CHF. |

EUR/CHF and USD/CHF, September 28(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is consolidating inside yesterday’s ranges against the euro and yen while extending its gains against sterling and the dollar-bloc currencies. The sell-off in the US debt market continues to drag global yields higher. The 10-year Treasury yield reached 2.01% on September 8 and now, nearly three weeks later, is near 2.35%. It had finished last week at 2.25%. With today’s three basis point increase, the 10-year yield is above the 200-day moving average. The 10-year German Bund yield moved above 50 bp today for the first time since early August. In early September, it reached a low near 29 bp. The US premium reached 1.88% today, the most since July. The two-year premium reached almost 2.2% earlier today, its largest since March. The US 10-year premium over Japan has risen sharply as well. It bottomed on September 7 just below 2.03%. It tested 2.30% today, moving above its 200-day moving average (~2.26%) for the first time since mid-July. There are only two major currencies that have appreciated against the dollar over past month, sterling and the Canadian dollar. The gains in both can also be traced to interest rate expectations. The market has moved to discount a strong chance of a BOE hike as early as the November 2 meeting (~75% chance). The two-year Gilt yield has risen nearly 30 bp over the past month, nearly twice the increase of the US two-year Treasury yield. The yield on the 10-year Gilt is up 35 bp, again nearly twice as much as the US increase. |

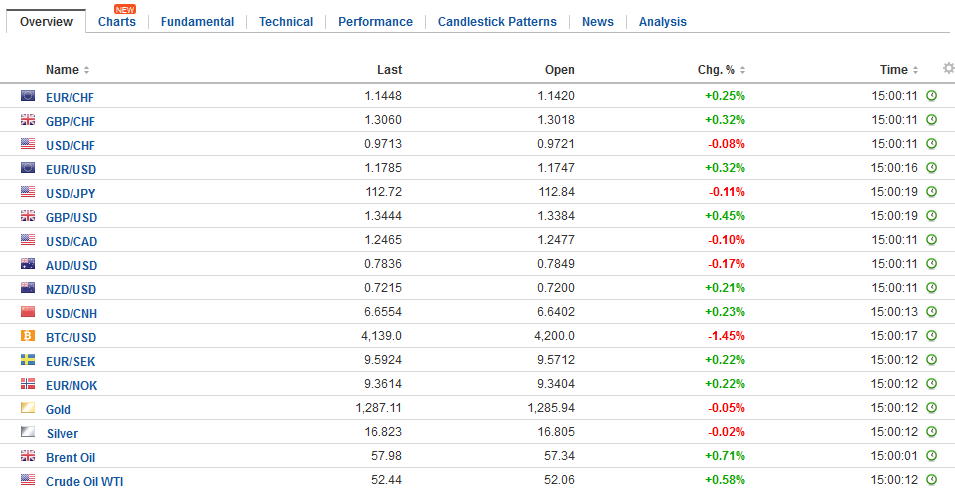

FX Daily Rates, September 28 - Click to enlarge |

| Canada is a similar story. Its 10-year yield is up 27 bp, and the two-year yield is up 31 bp. Over the past two weeks, first the deputies and yesterday the Governor seemed to signal to the market that it will not likely raise rates next month, as some had thought likely given the continued strength of Canadian real sector data.

The euro is trading inside yesterday’s ranges. Yesterday’s high was just shy of $1.18. A move above there could see gains toward $1.1830. We’ll be watching the price action to see if the market’s bias has shifted from buying euro dips to selling into rallies. Between $1.1750 and $1.1755 today there are 1.6 bln euro options set to expire. The firmer US rates are not lifting the greenback against the yen today. It was turned back from yesterday’s highs near JPY113.20. Initial support is pegged in the JPY112.40-JPY112.60 area. Sterling is slipping lower after closing below $1.34 yesterday.At $1.3350 it retraced 61.8% of its BOE-spurred rally. Additional support is seen near the 20-day moving average that is found near $1.3310. After selling off hard yesterday as Bank of Canada, Governor Poloz confirmed not set the course of Canadian rates and sounded a bit cautious. The US dollar rose above CAD1.25 today for the first time this month and was turned back amid the dollar’s general consolidative tone. The CAD1.2430-CAD1.2450 may offer initial support. After filling a gap from September 12 on Monday and consolidating Tuesday, the S&P 500 rose to a new record of 2511.75 yesterday. It was not sufficient to lift Asian shares, where the MSCI Asia Pacific Index fell for the sixth consecutive session, and this is even with the bounce back in Japanese stocks after yesterday’s ex-dividend dip. The MSCI Emerging Markets Index is off 0.6% a, and it is has fallen for the sixth session. European shares are faring better, and the Dow Jones Stoxx 600 is edging higher, led by financials, industrials, and energy. Utilities and consumer sectors are drags. |

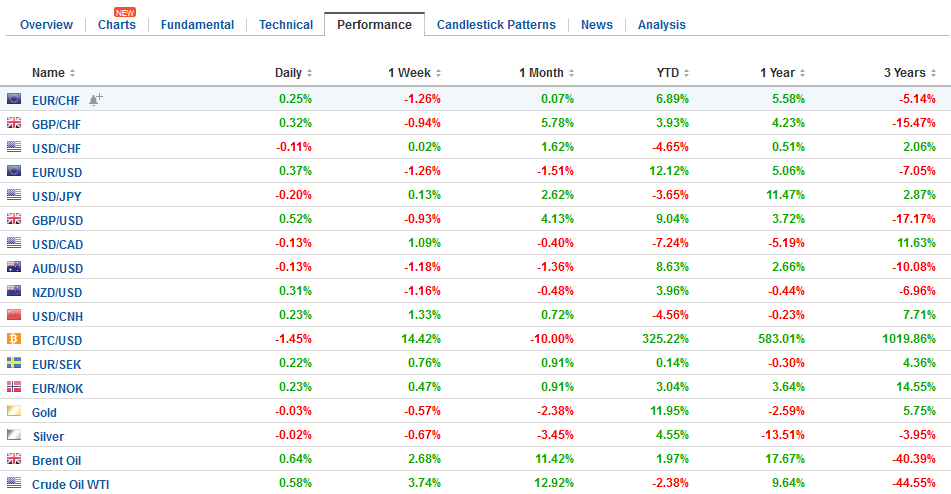

FX Performance, September 28 - Click to enlarge |

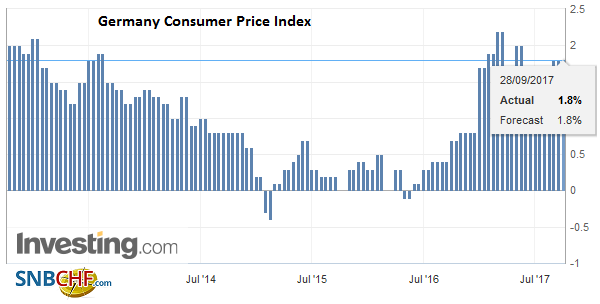

GermanyThe immediate focus is on inflation reports. Spain and German states have reported a mixed bag ahead of tomorrow’s preliminary regional estimate. Spain’s harmonized measure rose 0.6% in September, which is a touch less than expected, and due to the base effect, the year-over-year pace ticked down to 1.9% from 2.0%. Five German states reported inflation figures today. The year-over-year rates increased in two states, fell in one state, and was unchanged in the remaining two. The composite will be reported shortly and is expected to tick up to 1.9% from 1.8%. |

Germany Consumer Price Index (CPI) YoY, September 2017(see more posts on Germany Consumer Price Index, ) Source: Investing.com - Click to enlarge |

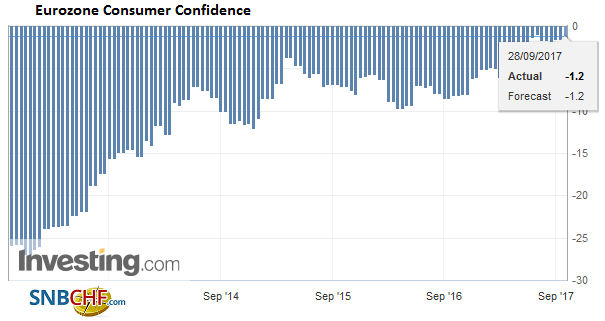

EurozoneThe eurozone preliminary September CPI is expected to have increased to 1.6% from 1.5%, mostly due to energy costs. The core rate is expected to be unchanged at 1.2%, for the third month. It is most unlikely to change Draghi’s assessment that continued substantial monetary accommodation is necessary. |

Eurozone Consumer Confidence, September 2017(see more posts on Eurozone Consumer Confidence, ) Source: Investing.com - Click to enlarge |

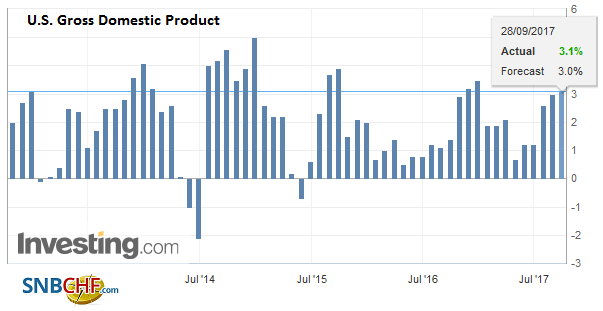

United StatesThe US reports a revised estimate for Q2 GDP today alongside trade and inventory data that will help shape expectations for Q3 GDP. Weekly initial jobless claims too will be reported, but the disruption caused by the storms has not completely washed out. Tomorrow, the US reports personal income and consumption data, which includes the core PCE deflator. The core deflator is expected to have risen 0.2% in August, the most since January. However, the year-over-year rate may stabilize after falling in five of the first seven months of the year. There are a couple of other developments to note. First, the Reserve Bank of New Zealand left rates on hold as widely expected. It did not shed fresh light on the course of policy but signaled no hurry whatsoever. It was cautious on growth and expected inflation to soften. From a technical point of view, we still like the Kiwi against the Aussie. We anticipated an Aussie bounce at the start of the week but saw that as a selling opportunity. Today, the cross returned to nearly the low of the week. We suspect there is room for the cross to drop another 1-2% in the coming weeks. |

U.S. Gross Domestic Product (GDP), Q2 2017(see more posts on U.S. Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

United Kingdom

Second, reports suggest that the EC could make a small gesture toward the UK on Brexit and that is to change the negotiators’ mandate to also include a transition period. The EU Parliament is already reportedly drafting a motion that could be voted on next week. One of the issues with that is what is the status of the European Court of Justice during the transition. Earlier this week, UK’s Davis argued against its jurisdiction during the transition, but of course, the EC will insist on it.

There is a large BOE conference today as it celebrates its 20-years of independence. The conference is well underway, and it poses some headline risk, but this is not the venue for new policy announcements or hints. Three Fed officials are speaking today as well. We have already heard from Atlanta’s Bostic, and George heads up the hawkish wing of the Fed (we suspect she was the dot plot that thought two rates hikes this year would be appropriate, meaning she thinks the Fed is already slipping behind the curve). That leaves the outgoing Vice Chairman Fischer who is speaking at the BOE conference that may be the most interesting of Fed speakers today.

Japan

Japan will report August inflation figures tomorrow. The headline rate is expected to rise to 0.6% from 0.4%. It would be the highest in two years. The core rate, which excludes fresh food is expected to accelerate to 0.7% from 0.5%. This would also be the highest reading in two years. The measure that excludes fresh food and energy belies the challenge. It is expected to edge higher from 0.1% in July. It would match the fastest pace reported this year (January).

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,Eurozone Consumer Confidence,Eurozone Consumer Price Index,Germany Consumer Price Index,newslettersent,SPY,U.S. Gross Domestic Product,U.S. Gross Domestic Product QoQ,USD/CHF