Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

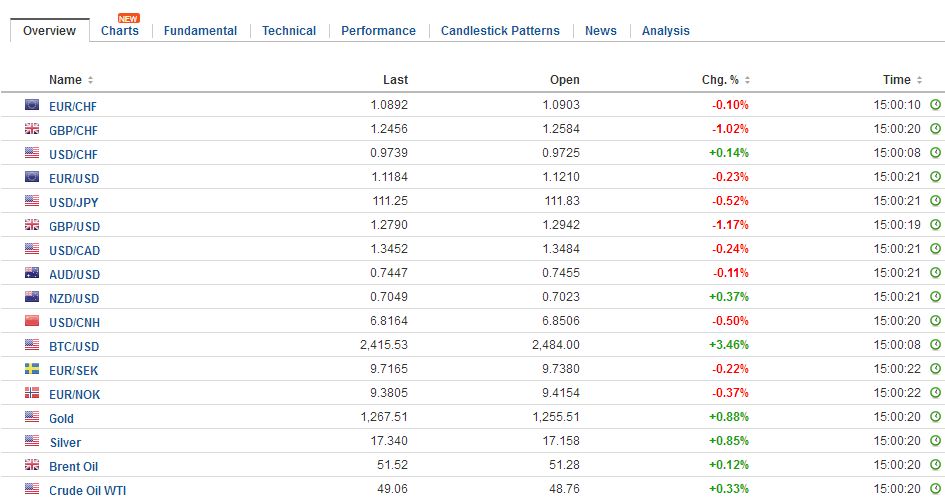

Swiss FrancThe Euro has fallen by 0.01% to 1.0902 CHF. |

EUR/CHF - Euro Swiss Franc, May 26(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe markets are unsettled. It is not so much in the magnitude of moves as the breadth of the move. The nearly 1% rally in gold is a tell, but also the inability of equity market to follow the lead of the US markets, where the S&P 500 and NASDAQ set new records. US yields are softer, and the yen is the strongest of the major currencies, up 0.7% against the greenback. Sterling is on the other side of the spectrum. It is off 0.5% near $1.2880. The Telegraph reported the Manchester terrorist might have distributed other explosive devices. Separately, or at least a difficult connection, the latest YouGov poll, the first since the terrorist attack, have tightened, with the Tories lead down to five percentage points. A week ago, the polls showed a nine-point margin, which itself was already halved from levels seen in some polls last month. The US dollar is nursing mostly small net losses as the week draws to a close. Sterling was up slight on the week coming into today. Momentum traders were already getting frustrated with the inability to sustain the $1.30 level, let alone rise above the $1.3055 area. That said, sterling may find a bid ahead of the recent lows. These are roughly $.1.2845 from May 12 and $1.2830 from May 4. At $1.1215 the euro is up less than 0.1% against the dollar this week, that has been characterized by choppy trading back and forth around the figure. The triangle/wedge/flag pattern that appears to be traced is often seen as a continuation pattern. Above the almost $1.1270 high seen earlier this week, is the November election high of $1.1300. Next week, the eurozone flash May CPI will be released. We suspect it will see both the headline and core softer, which might lend credence to our suspicions that the market is getting ahead of itself on changes in ECB policy. |

FX Daily Rates, May 26 - Click to enlarge |

| The dollar is being pushed below JPY111.00 in late-morning turnover in Europe. The week’s low is near JPY110.85. A break of JPY110.70 could spur another leg lower toward JPY110.25. On the other hand, a move back above JPY111.20 would likely squeeze the intraday shorts.

There are three economic stories today to note. Reports suggest that the PBOC has informed local banks that it is changing the way it sets the daily fix. It says it will add a “counter-cyclical factor.” It is not exactly clear what this means. There are a couple of possibilities. It could be an explicit way to dilute market forces This seems unlikely. Why make it explicit? An alternative explanation is that it will formalize what is already taking place. The fix is a bit of a black box, and participants have long recognized a subjective element. The process of defining it also would seem to limit it. The yuan initially built on yesterday’s gains. According to Bloomberg, the dollar fell to CNY6.8465, its weakest level since January. It recovered late back to CNY6.8640. The greenback has slipped against the redback for the third consecutive week, the longest streak in four months. Third, oil prices (both Brent and WTI) posted key reversals yesterday when OPEC delivered precisely what was expected, a nine-month extension of their six-month program aimed at bringing inventory levels back to five-year averages. Initially, there was a marginal extension of yesterday’s dramatic drop, but prices have stabilized. The August Brent futures are 0.6% higher (~$52.05) and puts the weekly loss near 3.1%. The July light sweet futures contract is up 0.6% (~$49.20). It is off 2.9% this week. |

FX Performance, May 26 - Click to enlarge |

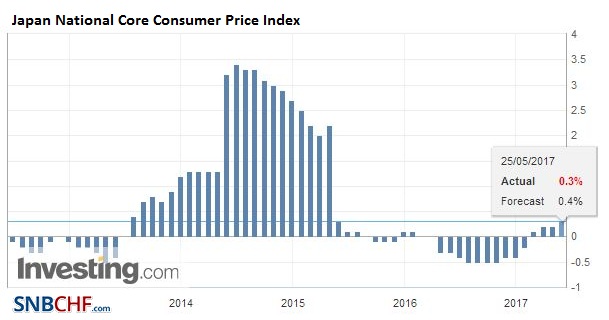

JapanThe second economic story today comes from Japan. It reported its April inflation. Consumer prices ticked up. Fresh food prices rose sharply, and when then excluded to get to what is the BOJ’s core measure, prices rose 0.3%. It was expected to rise a bit faster after 0.2% in March. In addition to fresh food, energy, which the BOJ says rose 4.5%, also contributed to the headline increase. Excluding both fresh food and energy, Japan’s CPI was flat after falling 0.1% in March. Separately, Japan that rising advertising, hotels, and construction lifted producer service prices 0.7% from a year ago, down from 0.8% in March. |

Japan National Core Consumer Price Index (CPI) YoY, April 2017(see more posts on Japan National Core Consumer Price Index, ) Source: Investing.com - Click to enlarge |

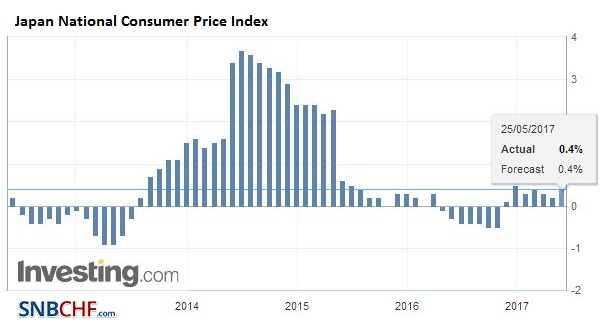

| Headline CPI rose to 0.4% from 0.2%, which was precisely what was expected. |

Japan National Consumer Price Index (CPI) YoY, April 2017(see more posts on Japan National Consumer Price Index, ) Source: Investing.com - Click to enlarge |

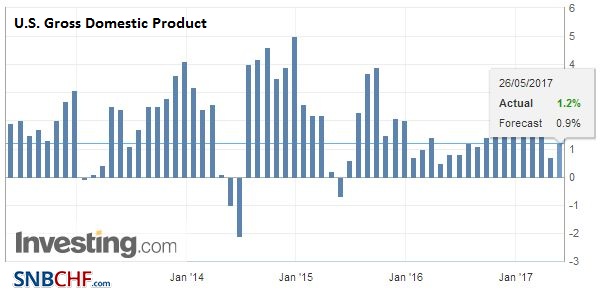

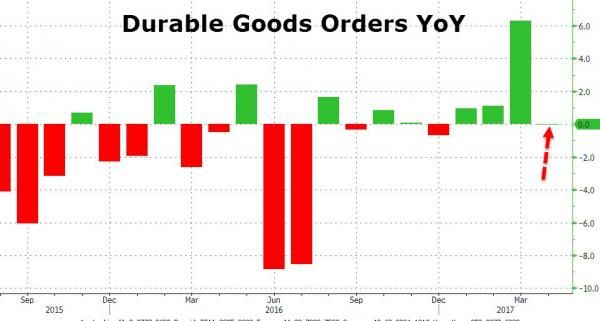

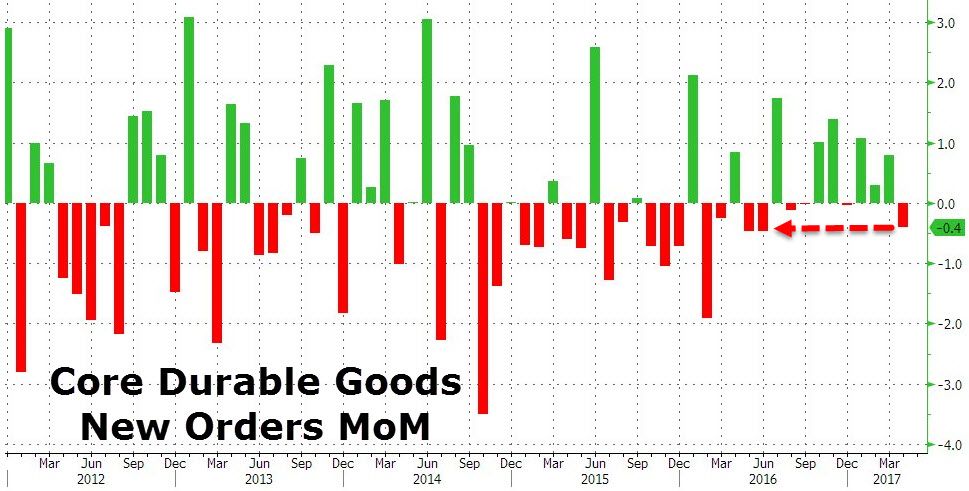

United StatesThe US session features a likely small upward revision to Q1 GDP, partly on slightly better consumption, April durable goods orders and the University of Michigan consumer sentiment and inflation expectations. The optics of durable good orders may be poor (1.5% decline expected after a 1.7% revised gain in March), but the details (and components that feed into GDP) may be more constructive.

|

U.S. Gross Domestic Product (GDP) QoQ, Q1 2017(see more posts on U.S. Gross Domestic Product QoQ, ) Source: Investing.com - Click to enlarge |

U.S. Durable Goods Orders YoY, April 2017(see more posts on U.S. Durable Goods Orders, ) Source: Zerohedge.com - Click to enlarge |

|

U.S. Core Durable Goods New Orders MoM, April 2017(see more posts on U.S. Core Durable Goods Orders (ZH), ) Source: Zerohedge.com - Click to enlarge |

|

U.S. Michigan Consumer Sentiment, May 2017(see more posts on U.S. Michigan Consumer Sentiment, ) Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CNY,$EUR,$JPY,EUR/CHF,FX Daily,Japan National Consumer Price Index,Japan National Core Consumer Price Index,newslettersent,SPY,U.S. Core Durable Goods Orders (ZH),U.S. Durable Goods Orders,U.S. Gross Domestic Product QoQ,U.S. Michigan Consumer Sentiment