Read More »

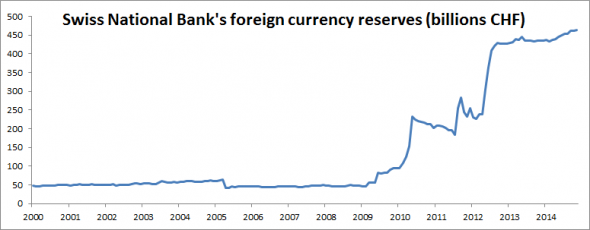

On Swiss National Bank

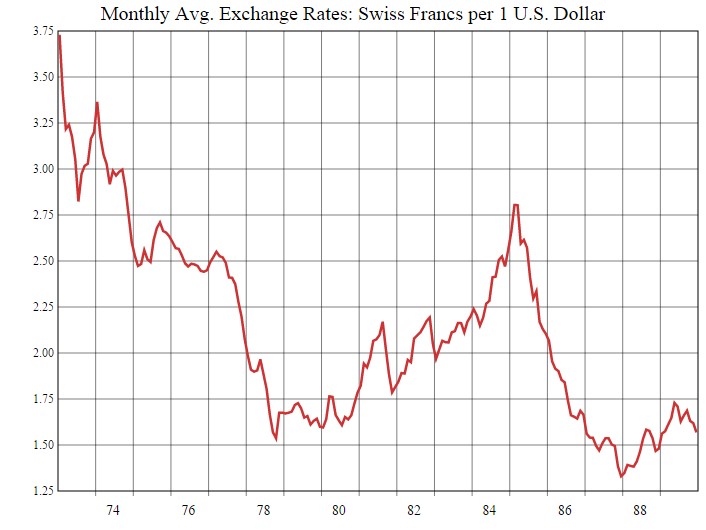

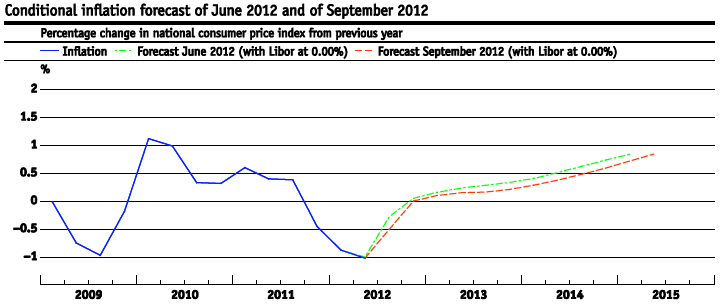

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

MintID Silver Bars and Rounds Up Close with Money Metals

MintID Silver Bars and Rounds Up Close with Money Metals3 Apr 2026

Linksextreme schäumen vor WUT! AfD gelingt weitere Sensation in Sachsen-Anhalt!

Linksextreme schäumen vor WUT! AfD gelingt weitere Sensation in Sachsen-Anhalt!3 Apr 2026

Wann zahlt die BU nicht?

Wann zahlt die BU nicht?3 Apr 2026

Was bedeutet das PFOF-Verbot?

Was bedeutet das PFOF-Verbot?3 Apr 2026

Money Metals Gold Bar In Space

Money Metals Gold Bar In Space2 Apr 2026

4-2-26 The Fed Is TRAPPED… And Oil Is The Problem

4-2-26 The Fed Is TRAPPED… And Oil Is The Problem2 Apr 2026

4-2-26 Dynamic Learning Series – Tax Strategies: Beyond Filing: Avoid Penalties & Plan Smarter

4-2-26 Dynamic Learning Series – Tax Strategies: Beyond Filing: Avoid Penalties & Plan Smarter2 Apr 2026

Will China be the real winner from the Iran war? | The Economist

Will China be the real winner from the Iran war? | The Economist2 Apr 2026

Achtung: Merz will CHAT-Kontrolle nun in Deutschland umsetzen!

Achtung: Merz will CHAT-Kontrolle nun in Deutschland umsetzen!2 Apr 2026

Artemis II: Our expert analyses the launch

Artemis II: Our expert analyses the launch2 Apr 2026

10 Ounce Sandblasted Silver Bar from Money Metals Exchange

10 Ounce Sandblasted Silver Bar from Money Metals Exchange2 Apr 2026

KI Hype wie Dotcom Crash? ️ Mehr dazu auf meinem Kanal!

KI Hype wie Dotcom Crash? ️ Mehr dazu auf meinem Kanal!2 Apr 2026

Blitzmeldung: Jetzt schlägt Ulmen zurück! SPIEGEL Story bricht zusammen! Hubig unter Druck!

Blitzmeldung: Jetzt schlägt Ulmen zurück! SPIEGEL Story bricht zusammen! Hubig unter Druck!2 Apr 2026

4 Libertad Silver Coin Sizes You Need to See at Money Metals

4 Libertad Silver Coin Sizes You Need to See at Money Metals2 Apr 2026

Waren Immobilien früher wirklich günstiger?

Waren Immobilien früher wirklich günstiger?2 Apr 2026

Lasst alles stehen und liegen und schaut dieses Video!!

Lasst alles stehen und liegen und schaut dieses Video!!2 Apr 2026

4-2-26 Fed Trap? Markets Face Inflation, Oil & Treasury Sell-Off

4-2-26 Fed Trap? Markets Face Inflation, Oil & Treasury Sell-Off2 Apr 2026

Is the private-credit meltdown the next financial crisis? | The Economist

Is the private-credit meltdown the next financial crisis? | The Economist2 Apr 2026

Benzinpreis-DESASTER mit Ansage! Neues Gesetz führt direkt zur Katastrophe an Tankstellen!

Benzinpreis-DESASTER mit Ansage! Neues Gesetz führt direkt zur Katastrophe an Tankstellen!2 Apr 2026

Diese Einstellung VERDOPPELT deinen Profit?

Diese Einstellung VERDOPPELT deinen Profit?2 Apr 2026