Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

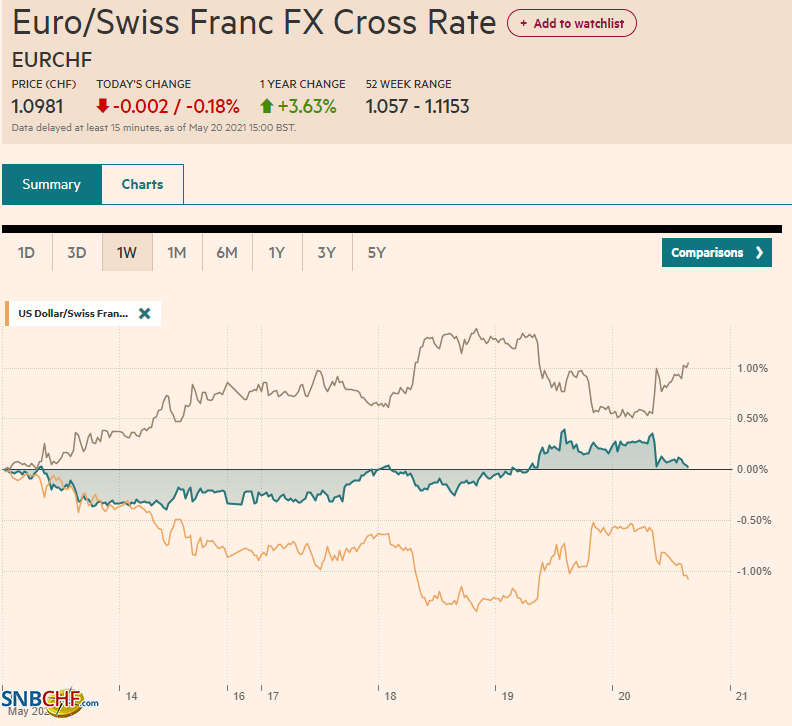

Swiss FrancThe Euro has fallen by 0.18% to 1.0981 |

EUR/CHF and USD/CHF, May 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: US equity indices finished lower, but the real story was their recovery. Asia Pacific equities were mixed, with Australia’s 1.5% rally leading the recovery in some markets, including Tokyo and Singapore. Europe’s Dow Jones Stoxx 600 is up a little more than 0.5% near mid-session, led by information technology and industrials, while energy and financials lagged with small gains. US futures are narrowly mixed. The other main development was the jump in US Treasury yields as the market (over) reacted to the FOMC minutes that showed that the discussion of tapering has already begun. The rising yield lent the dollar support. The US 10-year yield is hovering around 1.65%, while European yields have edged a little higher. The German two-year bond yield is at the high for the year near -66 bp. The dollar has come back offered, falling against most of the major currencies. The Swiss franc and Japanese yen are leading the move advancers with around 0.25% gains, while the Scandis are lower. The euro and sterling are firmer but little changed. Emerging market currencies are split, with most of the Asian currencies softer and the European currencies higher. Yesterday’s 0.4% drop in the JP Morgan Emerging Market Currency Index ended a four-day advance, but it is recovering a little today. Gold is consolidating in yesterday’s broad range (~$1852-$1890) and is holding above $10 inside both extremes. After falling around 4.5% Tuesday-Wednesday, July WTI is trading quietly between about $63.20 and $64. Iron ore prices tumbled 6.3% in China, but copper prices that fell more than 3% yesterday have stabilized today. July lumber futures prices snapped a seven-day 25% slide yesterday with a nearly 5% gain. |

FX Performance, May 20 - Click to enlarge |

Asia Pacific

Japan’s net exports shaved 0.2 percentage points off Q1 GDP, but today’s figures suggest Q2 is off to a strong start. Led by autos and parts, exports surged 38% year-over-year in April, well above expectations. The year-over-year comparison is, of course, distorted by last year’s covid shock, but exports were up 8% from 2019. Shipments to the US are up 45% year-over-year and nearly 34% higher to China. Exports to Europe rose by almost 40%, the most since 1980. Imports rose by 12.8% compared with the median forecast in Bloomberg’s survey for a 9% gain. The net result was a trade surplus of JPY255 bln rather than JPY148 bln.

Australia’s April employment report was mostly disappointed. Overall it lost around 30k jobs when economists expected a 20k increase. Still, the number of full-time positions grew by almost 34k after a 21.1k loss in March. The participation rate fell to 66.0% from 66.3%, and that explains most of the drop in the unemployment rate to 5.5% from a revised 5.7% (initially 5.6% in March). The JobKeeper wage subsidy program ended, and it may take another month or so to have a better sense of the pace of recovery in Australia’s labor market.

The dollar peaked yesterday near JPY109.35 and has come back offered today. It was sold below JPY108.90 in the European morning but appears to be finding a bid. A move above the JPY109.50-JPY109.80 area that has capped the greenback over the past month likely requires higher US rates.

The Australian dollar fell by around 0.8% yesterday and has stabilized today. A$1.6 bln in options between $0.7760-$0.7775 that expire today may help cap the upside. There is another option for A$500 mln at $0.7730 that also expires today.

The greenback edged higher against the Chinese yuan today for the second consecutive session. It appears to have entered a consolidation phase between about CNY6.41 and CNY6.46. The PBOC set the dollar’s reference rate at CNY6.4464, and Bloomberg’s survey of bank models had a median projection of CNY6.4467. The yuan is at three-year highs against its CFETS basket. SWIFT reported that the yuan’s share of transactions fell to 1.95% in April, which is its lowest this year and follows a nearly 2.25% share in March. The small share underscores that the bulk of Chinese trade is still conducted in dollars, which, given the size of trade flows, makes managing the foreign exchange exposure a significant challenge.

Europe

The European Parliament has called on the EC to formally suspend ascension negotiations with Turkey over human rights and Ankara’s foreign policy. The vote was overwhelming: 480-64 with 150 abstentions. The ultimate decision is in the hands of the European Council (heads of state), and it will decide next month. Austria and France are sympathetic, while Germany, Bulgaria, and Hungary are opposed. Greece is still at odds with Turkey over gas exploration and Cyprus, but the US and some European countries are torn over Turkey’s strategic importance.

Europe appears to have more success in getting the US and Iran back into compliance with the nuclear agreement. EU sources were reported indicating progress toward a deal has been achieved. Talks will resume next week in Vienna. A deal is needed in the coming weeks, ahead of the June 18 Iranian election; otherwise, a longer delay is likely. If an agreement is reached, it does not mean that Iran’s full oil capacity will hit the market. Instead, it is likely to be small steps to allow for verification of the progress. Speculation is that at first, maybe 500k barrels of Iranian oil will come back to the market. OPEC+ has indicated it will make room for it without giving specifics.

Tomorrow, the eurozone’s flash PMI for May will be released. The Bloomberg survey shows expectations for a small dip in the manufacturing PMI while the service component is expected to improve as some social restrictions have been eased. After reaching $1.2245, the euro reversed yesterday to around $1.2160. It is consolidating within that range today. However, the attempt to take it above $1.2200 was met with new selling in the European morning. The 1.28 bln euro option at $1.2175 that expires today may pull the single currency down. There is another option for 680 mln euros at $1.2160 that also will be cut today.

The UK reports April retail sales and May preliminary PMI tomorrow. Both are expected to be solid as the British economy continues to recover from the contraction in Q1. Sterling is trading at a three-day low in Europe, near $1.4100. A convincing break could spur a move toward $1.40, around last week’s low. Initial resistance is seen around $1.4140.

America

The market reacted dramatically to the FOMC minutes, which is not often the case. The record showed there was indeed some discussion of tapering, and some members were open to having the debate in the “coming months.” Shortly after the discussion, Chair Powell said it was too early to talk about tapering at his press conference. The reaction by the market may reflect sentiment and positioning rather than the information content of the minutes. First, the open to discussion is not the same thing as a discussion. Second, that openness was predicated on continued rapid progress, and that was before the disappointing employment, retail sales, and housing starts reports. Third, it confirmed ideas, as we have suggested before, that the Jackson Hole confab in late August and the September FOMC meeting is a reasonable and recognized timeframe to expect such discussion. Separately, the minutes also gave the Fed the opportunity to reiterate what we argue is an important shift in its reaction function: actual performance is needed to meet the test of significant further progress to its goals, not forecasts.

Yesterday’s 20-year bond auction saw a lower bid cover (2.24 vs. 2.42) despite a higher yield (2.28% vs. 2.14%). Dealers were left with 23.8% compared with 21.1% last month. Today, the US Treasury auctions $13 bln of 10-year TIPS. At least two Fed presidents have argued that the housing market is sufficiently robust that it does not need the central bank’s support of buying mortgage-backed bonds from the Fannie Mae and Freddie Mac. Similarly, the Fed’s buying of TIPS is exacerbating an apparent shortage and, arguably, distorts the signal of inflation expectations used by policymakers and investors. Outside of the auction, the May Philadelphia Fed’s manufacturing survey and weekly jobless claims are on tap. The Philly Fed’s survey is expected to see the outlook slip to 41.0 from a little above 50. However, it should not be exaggerated. Even at 41.0, it is still at strong levels. Recall that in 2019, it was not above 18, and in 2018 it peaked below 32. Weekly initial jobless claims are expected to have eased to around 450k last week, which would be the second consecutive print below 500k. That would still leave it around twice the level seen in late 2019, though the trend seems clear. Canada and Mexico have light economic calendars today, but both report March retail sales tomorrow.

The US dollar bounced off the CAD1.20 support on Tuesday and traded around CAD1.2140 yesterday. It is consolidating so far today between CAD1.2100 and CAD1.2145. There is an option for around $340 mln at CAD1.2130 today. Last week’s high was near CAD1.2200, and the 20-day moving average is a little higher (~CAD1.2215), which the greenback has not closed above in a month.

The US dollar has risen against the Mexican peso for the past two sessions and is trading inside yesterday’s range so far today. Yesterday’s high was just shy of MXN19.98, and the 20-day moving average is even closer to MXN20.00. A move above MXN20.02 could signal a retest of last week’s high near MXN20.21. Separately, S&P took away Colombia’s investment-grade rating yesterday, downgrading it to BB+ (with a stable outlook), citing fiscal deterioration. It was not a complete surprise, though the outlook was mixed. The peso has appreciated about 1.5% this month to pare this year’s decline to about 6.6%.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Australia,Currency Movement,EUR/CHF,Featured,federal-reserve,inflation,Iran,Japan,newsletter,Turkey,USD/CHF