Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

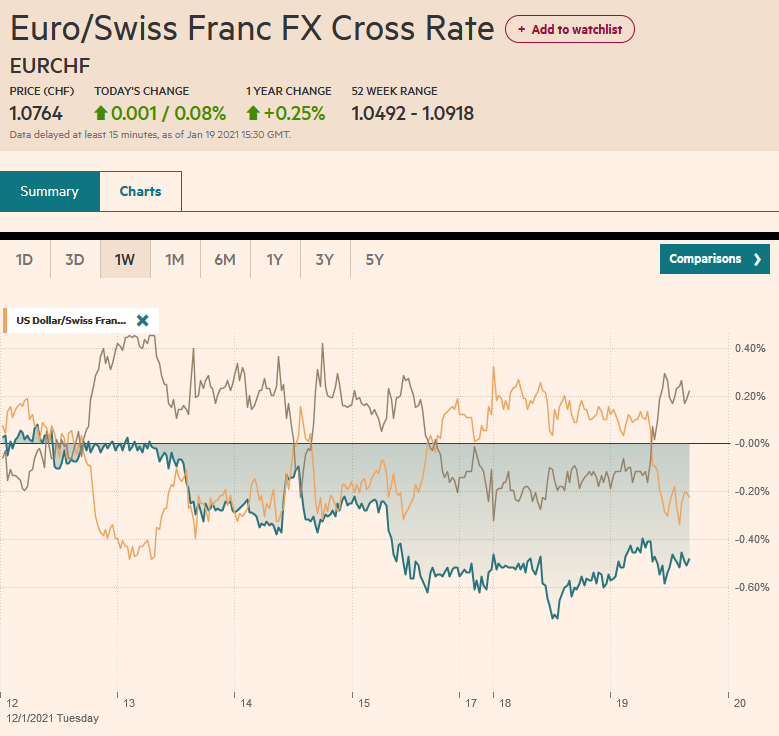

Swiss FrancThe Euro has risen by 0.08% to 1.0764 |

EUR/CHF and USD/CHF, January 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The animal spirits are on the march today. Equities are mostly higher, peripheral European bonds are firm, and the dollar is mostly softer. After posting the first back-to-back decline this year, the MSCI Asia Pacific Index bounced back today, led by a 2.7% gain in Hong Kong (20-month high) and a 2.6% rise in South Korea’s Kospi. The Nikkei and Taiwan’s Stock Exchange rose by more than 1%. Europe’s Dow Jones Stoxx 600 eked out a small gain yesterday and is a little higher today. The S&P 500 fell in the last two sessions for a loss of a little more than 1% and is trading about 0.6% better now. The US 10-year is firm at 1.11%, while European bonds are little changed, and the periphery is doing better than the core. Of note, France’s 50-year bond sale was greeted with a record reception. The dollar is lower against all the major currencies, but the yen. Most emerging market currencies are firmer as well. We see the dollar’s pullback as part of the larger correction that began almost two weeks ago. Gold recovered smartly from yesterday’s test on $1800 to return to the 200-day moving average (~$1845). February WTI reversed lower ahead of the long holiday weekend and made a marginal new low today (~$51.75) before recovering nearly a dollar. |

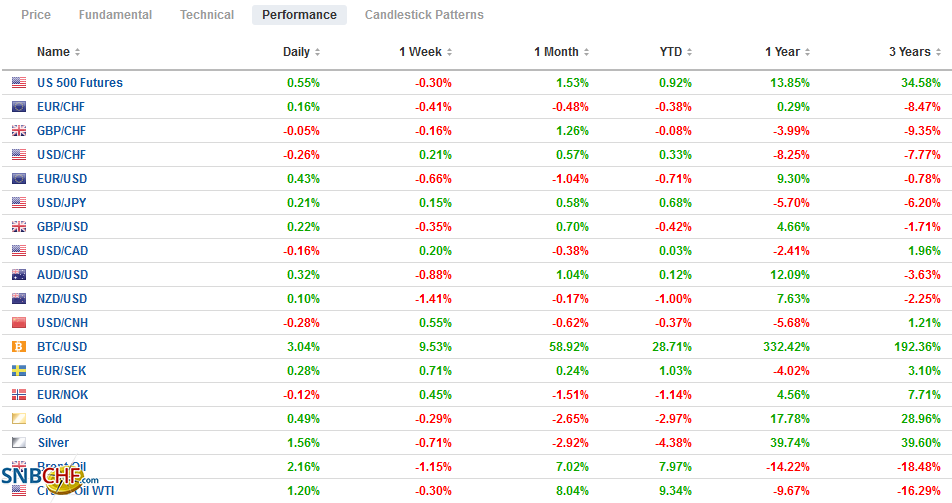

FX Performance, January 19 - Click to enlarge |

Asia Pacific

According to the recent government data, China’s rare earth exports fell by more than a quarter to what Reuters estimates are the lowest in five years. China attributed it to weaker global demand, but there is something else going on. Yesterday, China indicated that a new mechanism will be created to decide, coordinate, and regulate the rare earth supply chain (including mining, processes, and exporting). Rather than exporting rare earths, China’s industrial policy aims to export products containing rare earths. Move up the value-added chain. The big push now apparently is for batteries for electric vehicles. The PRC has become a net importer of rare earths that it processes. Its imports often come from mines it owns outright or has an important stake. For example, the Democratic Republic of Congo is responsible for 60% of the world’s cobalt. There are 12 mines, and reports suggest China has a stake in each, and more than 85% of the cobalt exports are headed to China. In 2018, China provided around 80% of US rare earths, and at least one mine in the US sends the material to China to be processed.

For the past several sessions, the dollar has forged a base in the JPY103.50-JPY103.60 area and is probing the JPY104.00 level. The high from January 14 was about JPY104.20, and there is an option for roughly $360 mln at JPY104.35 that expires later today, just shy of last week’s high near JPY104.40. The Australian dollar closed below its 20-day moving average yesterday (~$0.7100) for the first time in a little more than two months. It rebounded earlier today to $0.7725. The session high may not be in place, and we suspect there is potential toward $0.7740. The dollar’s reference rate was set at CNY6.4883, practically spot-on median expectations in the Bloomberg survey of bank models. The dollar’s four-day advance was snapped today. It has risen from almost CNY6.45 and stalled in front of CNY6.50. Faced with an increase in interbank borrowing costs for the ninth consecutive session, the PBOC injected CNY75 bln in seven-day cash via repo agreements. It is the first injection after draining for the past six sessions, and it was the largest supply of funds this month. Some liquidity appears to be going into equities, and Chinese traders reportedly bought a record $3.4 bln of HK shares today.

Europe

Despite Germany’s social restrictions, which may be tightened and extended, business sentiment held in better than feared. The ZEW survey assessment of current conditions did not deteriorate as economists expected, though it did not really improve, either. The -66.4 reading compares with -66.5 in December. However, the expectations component rose to 61.8 from 55.0. This is the highest since September and more than anticipated.

The UK Prime Minister, who holds the rotating G7 presidency, has invited South Korea, India, and Australia to the summit in June. Moreover, reports suggest Johnson intends on getting them involved right away, which seems aggressive. It appears to be causing some consternation among other members. Germany, Japan, France, and Italy are opposed.

Italy’s Prime Minister Conte survived the vote of confidence in the Chamber of Deputies yesterday, and today’s challenge is in the Senate. The government support is thinner. However, the ability to secure a majority is somewhat easier given that Renzi’s party will abstain, though it will still be close. A defeat could see Italian bonds sell-off, but Conte will seek to broaden the coalition in the existing parliament before elections are required. This could include independents or members of center-right parties.

Two central bank intervention announcements last week caught our attention. First, Sweden’s Riksbank announced a three-year plan to purchase SEK5 bln a month. The purpose is to fund reserve purchases in SEK and pay down the SEK178 bln fx loans from the National Debt Office, which is thought to be about 70% in US dollars. The krona was trending lower this year against both the dollar and euro, which follows the krona’s appreciation in the last few months of 2020. The impact is minor in terms of average daily turnover, estimated to be around SEK300-SEK320 bln almost equally divided between euros and dollars.

Second, the Israeli shekel soared in recent months and reached levels not seen since Q1 1996. The Bank of Israel intervened and bought $21 bln in all of 2020, with almost $4.5 bln in December alone, and still the shekel appreciated by 7.5% and nearly 3%, respectively. Businesses and investors were crying for relief. The central bank announced it would buy $30 bln this year, which triggered a powerful short-covering rally that carried the dollar from nearly ILS3.11 to almost ILS3.29 by the end of last week. Dollar sellers emerged yesterday. It is steadier today, but in wider ranges than typically seen before. Its preannounced intervention war chest may ultimately prove insufficient to prevent shekel appreciation. The $30 bln is roughly twice its current account surplus, but foreign direct investment inflows are nearly the same size as the current account surplus. And yet, net portfolio inflows should be expected, but most importantly, how Israeli offshore investment is managed can be impactful. Profit-taking on foreign investments or hedging the currency risk, even on a small fraction of the roughly $470 bln of foreign stocks and bonds owned by Israelis, can be a significant force rivaling the current account and direct investment-related flows.

The euro was sold a little below $1.2060 yesterday, its lowest level since December 1st. It reached $1.2130 in the European morning, and the $1.2140 area is the halfway point of last week’s decline. The bounce has left the euro’s intraday momentum indicator stretched. We expect North American dealers will take advantage of the upticks for a better selling opportunity. Also, note there are around 4.1 bln euros of $1.2190-$1.2200 options that roll-off today. Sterling recovered a little more than a cent from yesterday’s lows (~$1.3520) to today’s high. It faces resistance near $1.3635. Tomorrow the UK reports December CPI figures, and a small uptick is expected.

America

The Senate holds the confirmation hearing for Yellen. She was the first woman to head the Federal Reserve, and she will be the first woman to lead the US Treasury, and the first person to have held both posts. It is a reflection of our age. Like the current Federal Reserve, the former Chair can be expected to recognize the need for fiscal support, while at the same time acknowledging that deficits will decline on the other side of the emergency. The stock of debt is elevated, but it not extreme in relative or absolute terms. Despite higher debt in 2020, the servicing costs appear to have fallen. Moreover, as the economy grows faster than the level of interest rates, debt will decline as a percentage of GDP. Her remarks on the dollar will be scrutinized. To demonstrate the Biden Administration’s multilateral thrust, at this juncture, it is sufficient for Yellen to acknowledge the G7/G20 position that exchange rates are best set by the market. At the end of last year, the US Treasury cited Switzerland and Vietnam as currency manipulators. She may be asked about those, and of course, the yuan. The new US Treasury model had the yuan a few percentage points undervalued. However, it is interesting to note that when adjusted for GDP per capita, The Economist Big Mac index of purchasing power parity has the yuan slightly (~2.5%) overvalued.

The economic calendars for North America are light today. The Treasury’s International Capital (TIC) for November will be reported today at the end of equity trading. Capital flows were volatile at the onset of the pandemic, but long-term inflows averaged $23.56 bln in the first ten months of 2020 compared with an average of $27.21 bln in the same period in 2019 and $54.32 bln in the Jan-Oct period in 2018. The week’s highlight includes the January Philadelphia Fed survey Thursday and weekly jobless claims, as well as Friday’s preliminary PMI. Canada reports the December CPI tomorrow, shortly before the outcome of the Bank of Canada meeting is announced. Although the consensus is for a standpat outcome, a “mini-cut” cannot be ruled out given the official rhetoric. The current overnight target rate is 25 bp. The main feature for Mexico is the December unemployment figures on Thursday. Brazil’s central bank meets tomorrow, and the is little chance of a change in the 2% Selic rate.

Last Thursday, the US dollar recorded its lowest level against the Canadian dollar since April 2018 (~CAD1.2625). Between the modest greenback strength seen yesterday and expectations that Biden cancels the XL pipeline, the US dollar tested CAD1.28. It has come back offered today and is testing the CAD1.2720 area in the European morning. It can fall a bit further in the North American session, but we look for support in the CAD1.2690 area to hold. That said, a break could signal a move toward CAD1.2640. The greenback held below MXN20.00 yesterday and reversed lower, closing a little under MXN19.69. It has taken out yesterday’s low (~MXN19.66) but struggles to maintain the downside momentum. A move above MXN19.75 would suggest a return to MXN20.00 is likely. The dollar fell from BRL5.5160 last week, its highest level since mid-November, to BRL5.20. The low from earlier this month was around BRL5.12, and there is scope for a re-test.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brazil,China,Currency Movement,EUR/CHF,Featured,Israel,newsletter,Sweden,USD/CHF