Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

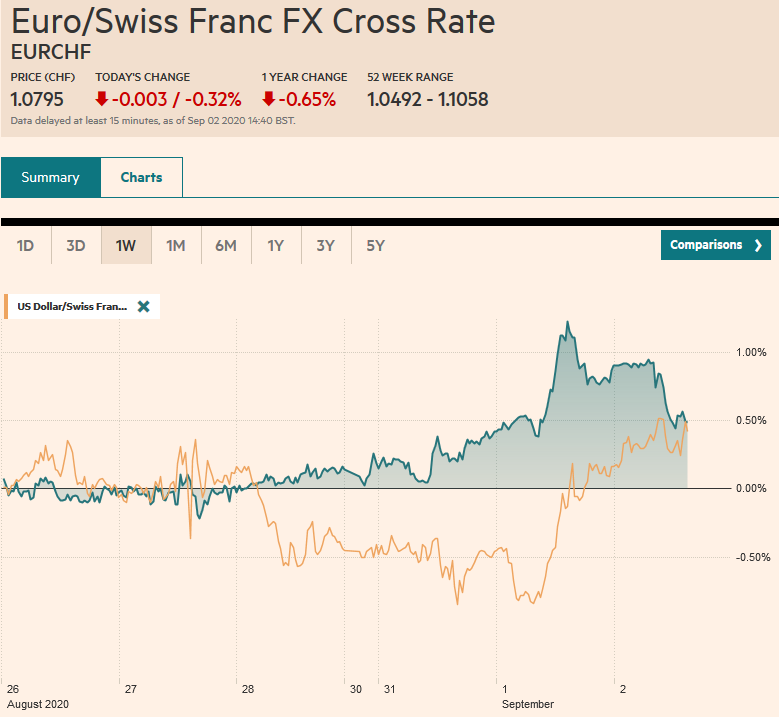

Swiss FrancThe Euro has fallen by 0.32% to 1.0795 |

EUR/CHF and USD/CHF, September 2(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: After poking above $1.20 for the first time in more than two years, the euro reversed lower yesterday and is continuing to succumb to profit-taking pressures today. Comments from ECB’s Lane appeared to trigger a reversal yesterday throughout the currency markets. Gold also reversed after approaching the $2000 level, and follow-through selling has been seen today too. The dollar is stronger against all the currencies today. The US benchmark 10-year bond yield is little changed at 69 bp, while European bond yields are off 3-5 bp. The stock markets have not been distracted. Asia Pacific bourses were mixed, but the yen’s pullback helped lift the Japanese equities. Korean, Australian, and Indian stocks led the advancers. In Europe, consumer discretionary, information technology, and materials are posting substantial advances to lift the Dow Jones Stoxx 600 more than 2% near midday. Financials are lagging. US equities closed on a high note yesterday, and the S&P 500 is poised to gap higher. Gold retreated to about $1956 in late Asia before finding a bid in early Europe. October WTI is firm, straddling the $43-level in a narrow range. API estimated another sharp drop in US crude inventories. If confirmed by the EIA today, it would be the sixth consecutive weekly decline. |

FX Performance, September 2 - Click to enlarge |

Asia Pacific

Australia’s Q2 GDP contracted by 7% quarter-over-quarter. It was larger than expected and follows a 0.3% decline in output in Q1. Year-over-year, the economy shrank by 6.3% after growing 1.6% in the year through Q1. The new outbreak of the virus will impact the strength of the recovery this quarter, and a small expansion is expected.

South Korea’s inflation picked up for the third consecutive month. In May, the year-over-year rate slipped below zero, but price pressures have been rising, and in August stood at 0.7% year-over-year, matching the 2019 year-end reading. Part of the force is coming from an unusually wet season that has pushed up fresh food prices. The core rate, which excludes food and energy, rose 0.4%, the same year-over-year pace as in July.

The dollar practically traded the entire August range (~JPY105-JPY107) last Friday. Although it was not subject to follow-through selling this week, it has remains well within that range. In fact, the greenback is edging higher for the third session today and is a little above the midpoint near midday in Europe. There is an option for $1.1 bln at JPY106.50 that expires today, but the intraday momentum indicators suggest the greenback is likely to be capped ahead of it. The Australian dollar set new two-year highs yesterday before reversing lower. A potential bearish shooting star candlestick signaled follow-through selling today and after poking above $0.7400 yesterday, has been pushed back to almost $0.7335 today. The downside momentum has slowed, and a move now above the $0.7365 area would help stabilize the technical tone. The US dollar initially ticked up against the Chinese yuan, but could not maintain the interest and slipped back to extend its losing streak to the fourth consecutive session. The PBOC set the dollar’s reference rate at CNY6.8376, a bit stronger than the bank models suggest.

EuropeAround the time the euro was pushing above $1.20 yesterday for the first time since May 2018, the ECB’s Chief Economist Lane said that while the central bank does not target the exchange rate, the euro-dollar exchange rate matters. Many see this as a sign of the ECB’s growing concern about the euro’s strength, especially after the preliminary August CPI report showed a deflation. The risk they see is some more talk along these lines from next week’s ECB meeting (September 10). The fact that Lane’s comments had such weight, though, may reflect market positioning. After all, the speculative positioning in the futures market was record-long euros. And it was not just the euro near key levels yesterday. The Australian dollar had risen above $0.7400, and sterling was approaching $1.35. Gold was near $2000 an ounce. Market talk suggested profit-taking orders were hit. Part of the fuel for the euro’s assault on $1.20 was coming from ideas that the ECB was in no position to trump the Fed’s move to an average inflation target, which after an initial wobble, was understood to be dollar-negative. |

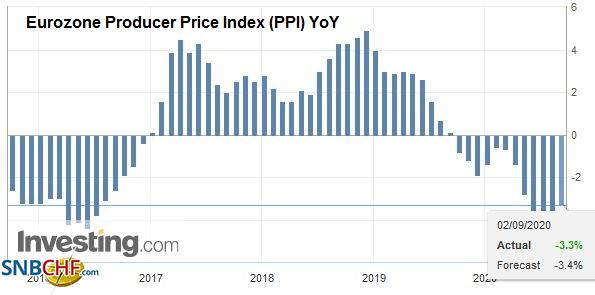

Eurozone Producer Price Index (PPI) YoY, July 2020(see more posts on Eurozone Producer Price Index, ) Source: investing.com - Click to enlarge |

Yesterday’s price action left a potential bearish shooting star candlestick in the euro, and follow-through selling saw it approach $1.1850 in early European trading today. The $1.1880-$1.1900 offers the nearby cap. The lower end of the range in the second half of August is around $1.1750, and that seems to be the risk. Given the recent string of US data, including yesterday’s ISM data, and the proximity of Friday’s jobs report, the dollar bears are likely to be restrained, not to mention next week’s ECB meeting. Sterling posted a similar potential candlestick yesterday after approaching the $1.35 technical objective. It has fallen back to around $1.3325 in late Asian turnover before finding better bids in the European morning. Monday’s low was closer to $1.3300, and that is where better support may be found. Initial resistance is seen near $1.3375 now.

America

Although many think that Federal Reserve Governor Brainard had an “Emporer is not wearing clothes” moment in a speech yesterday. “Had the changes to monetary policy goals and strategy we made in the new statement been in place several years ago, it is likely that accommodation would have been withdrawn later, and the gains would have been greater, she said regarding minority employment. It is hardly a state secret that in tight labor markets, employers hire people they would not usually hire. The fact of the matter is that when unemployment hit a 50-year low last year, so did the gap between white and black unemployment.

It is not just as Brainard says about a few years ago, but the same argument applies since 2012 when the Fed first adopted a formal inflation target. Part of the purpose of an inflation target was to narrow the scope for idiosyncratic elements in the setting of monetary policy. Purposely not defining the period that “the average” inflation is to apply, the Fed eschews the confines of rule-based decision making. Also, race-based disparities overlap in America with class-based disparities. The latter is not being addressed, and in practice appears to be a critical comorbidity, even though the old Humprey-Hawkins legislation that modernized the Fed’s charter recognized this element. Even though Brainard stopped shy of endorsing a bill in Congress to add racial equality to the Fed’s mandates, which Biden appears to have supported, she is a likely candidate for Treasury Secretary in a Democratic administration.

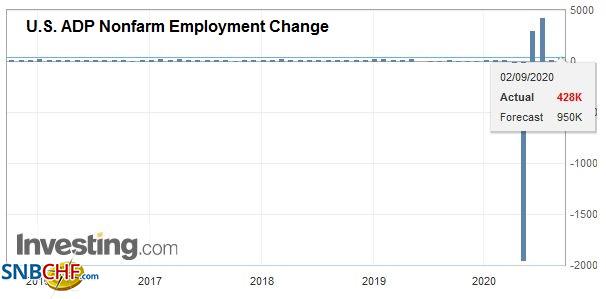

| US economic data today includes more from the seemingly rapidly recovering manufacturing sector in the form of factory goods orders and the final look at July durable goods orders. The API private sector jobs estimate will draw attention, though it has been having a difficult time during the pandemic, and back month revisions have been substantial. |

U.S. All Car Sales, August 2020 Source: investing.com - Click to enlarge |

| The market is looking for around one million jobs from ADP’s estimate, and July’s 167k estimate is bound to be revised higher. The Fed’s Beige Book is released late in the session, and more reports suggest that the US absorbed the loss of the $600 a week in federal unemployment insurance without much impact (yet). The Fed’s Williams and Mester speak before the Beige Book’s release, while Daly speaks after the markets close today. |

U.S. ADP Nonfarm Employment Change, August 2020(see more posts on U.S. ADP Nonfarm Employment Change, ) Source: investing.com - Click to enlarge |

Canada reports Q2 productivity. July’s trade figures are released tomorrow, and then the August jobs report on Friday. Mexico reported another stronger worker remittances yesterday, and today’s reports include the July leading economic indicator and August vehicle sales. After imploding in the first four months of the year, Mexican auto sales have been recovering, but in July, they were still off nearly a third from July 2019. In contrast, US August auto sales reported yesterday (~15.2 mln saar pace) was about 10.5% below August 2019. That said, year-to-date sales through August are around 20% below the year-ago period.

The US dollar briefly traded below CAD1.30 for the first time since January yesterday and bounced to almost CAD1.3090 in yesterday’s reversal. There has been no follow-through US dollar buying today, and it is chopping in a narrow range above CAD1.3050. Chart support is a little lower, but a consolidative North American session looks likely. The Mexican peso did experience yesterday’s dollar reversal. The dollar finished yesterday, almost 0.5% weaker against the peso. It is holding now a little above yesterday’s low (~MXN21.6770). The 200-day moving average is a bit below MXN21.50. Resistance is likely to be found near old support around MXN22.00.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Australia,Currency Movement,ECB,Featured,FOMC,newsletter,South Korea