Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.09% to 1.0755 |

EUR/CHF and USD/CHF, August 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

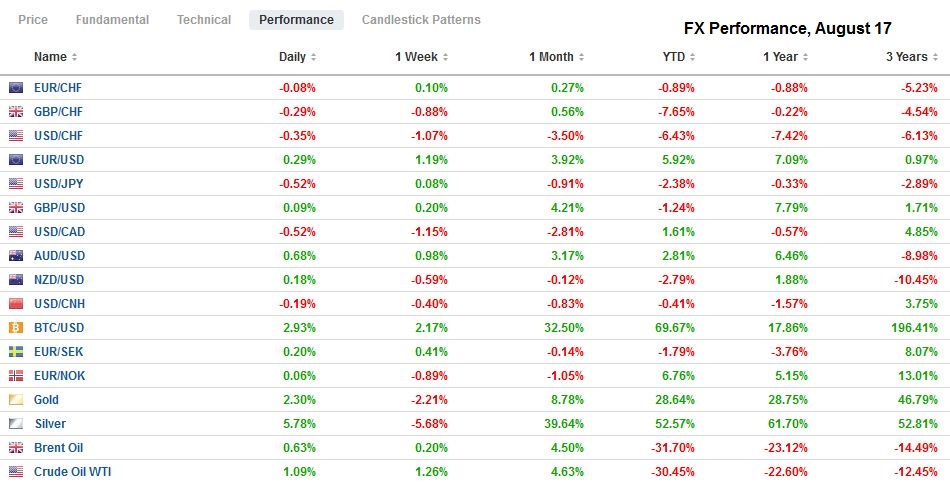

FX RatesOverview: The capital markets are looking for direction. Asia Pacific equity markets were mixed, with gains in China, Hong Kong, and Taiwan countering losses in Japan, South Korea, and Australia. European and US shares are trading slightly firmer. Benchmark bond yields are mostly 1-2 basis points lower in Europe, and the US 10-year yield is off nearly three basis points to 68 bp. The dollar itself is heavy. Only the New Zealand dollar has been unable to gain traction against the greenback. The liquid, accessible emerging market currencies, especially in eastern and central Europe (with the exception of the Polish zloty), are weaker, perhaps reflecting the threat of Russia aiding Lukashenko in Belarus, are leading the EM currency losses. The Chinese yuan’s small gain (~0.15%) makes it among the strongest emerging market currencies today. Gold is firm, overcoming early weakness to push against the pre-weekend high. Oil prices remain in well-worn ranges with the September WTI contract straddling the $42-a -barrel level prior to the US open. |

FX Performance, August 17 - Click to enlarge |

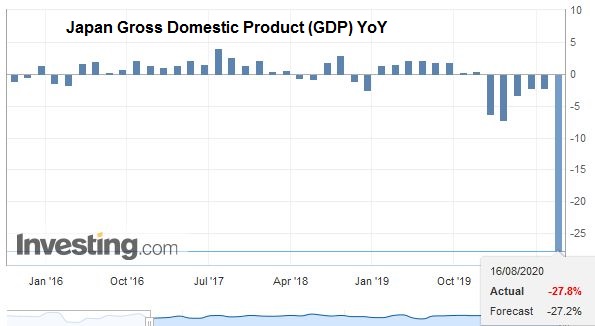

Asia PacificJapan reported Q2 GDP contracted by a 27.8% annualized rate in Q3, a bit deeper than expected, and the third consecutive quarterly decline. Consumption was, of course, hampered by the virus, and weaker exports sapped industrial output. On a quarter-over-quarter basis, the world’s third-largest economy shrank by 7.8%. Net exports subtracted about three percentage points from GDP. |

Japan Gross Domestic Product (GDP) YoY, Q2 2020(see more posts on Japan Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| The economy appears to be rebounding this quarter, and many look for around 10% annualized growth. |

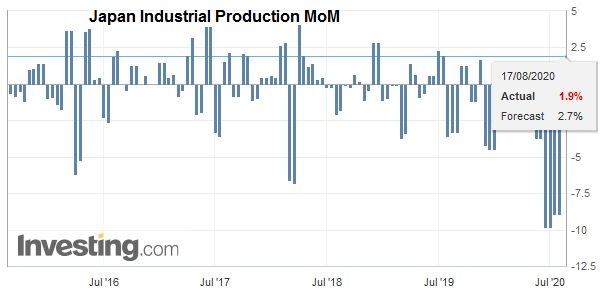

Japan Industrial Production MoM, June 2020(see more posts on Japan Industrial Production, ) Source: investing.com - Click to enlarge |

New Zealand’s Prime Minister postponed the national election by four weeks to October 17 due to the rise of infections. There is no fixed date for the election under the New Zealand parliamentary system. The government enjoys a lead in the polls, and the opposition called loudly for a delay. It is not nearly as controversial as say it would be in the US, where the Constitution provides for an election schedule, the incumbent is behind in national polls, and the opposition is not on-board. Meanwhile, several countries in the region are seeing new outbreaks, including Australia, which has extended its lockdown in Victoria for another four weeks to mid-September, Hong Kong, which has extended its social distancing rules for another week, and South Korea that is experiencing the most new cases since March.

The US-China review of the Phase 1 trade deal did not take place. The newswires report a scheduling conflict, but that rings hollow to many observers. China appears to be stepping up agriculture and energy purchases from the US. However, at the same time, it will sell advanced fighter jets (F-16s) to Taiwan for the first time since 1992 and is having naval exercises in the South China Sea, where China demonstrating its influence through exercises that include missiles and torpedos. The White House also took the formal step that requires TikTok’s parent to sell its US assets.

Today looks to be the first in four sessions that the dollar is unable to resurface above JPY107.00. Initial support is seen near JPY106.00, and there is an expiring option today for almost $440 mln at JPY106.02. A break could signal a test on the JPY105.60 area, which is about the midpoint of its range since the greenback bottomed around JPY104.00 at the end of July. The Australian dollar is firm and has poked through last week’s highs, though so far it has been unable to push through the $0.7200 area. It peaked earlier this month, near $0.7240. Support is now seen around $0.7160-$0.7170. The PBOC set the dollar’s reference rate a little softer than the bank models implied. It appeared to be generous in its provision of liquidity (CNY700 bln one-year medium-term lending facility–MLF), which may have helped lift stocks. The dollar held above last week’s low near CNY6.9310).

Europe

Several European countries are also experiencing a flare-up of the virus. Italy joined France and Spain in closing nightclubs. The economic highlight of the week comes at the end with the preliminary August PMI readings. A small gain in manufacturing may help offset the moderation in services to underpin the composite.

There is increasing pressure to extend government job support programs. In the UK, the furlough program that is keeping two million jobs is set to expire in October. In Germany, Finance Minister Scholz, who was picked last week by the new party leaders to be the SPD Chancellor candidate next year, argued to extend the government’s job subsidies to 24 months (from 12 months) and estimating the cost to be around 10 bln euros.

In the CFTC reporting week through August 11, speculators in the futures market extended its net long euro position to a new record high of almost 200k contracts. It represented an almost 10% increase from the previous week. However, the driving force was not the bulls, though they added 4k contracts to their gross long position. It was the bears that capitulated, buying back 15k contracts they previously sold. The gross short position of 66.3k contracts is the least in nearly seven years.

The euro is firm and has edged a few ticks above last week’s high in Asia, but has held below $1.1870. It found support in early Europe near $1.1830. The $1.19 area has proven resilient, and today there is an option struck there for nearly 940 mln euros that expires today. A higher close today would extend the euro’s advance for a fifth consecutive session. Sterling is higher for a third session. It found support near $1.30 last week and has not closed below there this month. The nearly GBP625 mln option at $1.3090 that expires today is less relevant now as today is the third session that sterling has traded above $1.31. Last week’s high was set before the weekend a little above $1.3140. So far, the month’s high is near $1.3185.

America

The Empire State manufacturing survey begins the monthly cycle of high-frequency economic data for the US. It has recovered smartly from -78.2 in April to +17.2 in July. Last month’s reading was the highest since November 2018 and likely overstates the recovery. A modest pullback in August to around 15 is expected. The US and Canada both report the June international portfolio flows. Canada also reports existing home sales. In both the US and Canada, the housing market, helped by low-interest rates, appear to be among sectors leading the recovery. The highlight of the week for Canada though, will be the retail sales and CPI reports. Mexico also reports retail sales later this week. For the US, highlights include the FOMC minutes, the Philadelphia Fed survey, and the 20-year bond auction ahead of the preliminary PMI report.

The Democratic Party convention will be held this week. While it may attract attention, the markets are unlikely to be particularly sensitive to the speeches. The same is likely true of the Republican convention next week. While President Trump is trailing in the national polls, voters give him a double-digit lead in better for the economy. This has spurred talk that a fiscal compromise with the Democrats is still possible, while the fight over the postal service is likely to ratchet up.

There has been much interest in Berkshire Hathaway’s purchase of Barrick Gold. The acquisition was funded by the sale of some of its bank holdings. We share two observations. First, investors ought not to confuse gold mining companies with gold bullion. The higher bullion prices raise the margin for the gold miners. All-in costs for mining is estimated to be around $800-$850 an ounce. With bullion prices near $2000 an ounce, the margins are plump, and that is what is likely the driver. Second, Berkshire Hathaway’s portfolio is still dominated by Apple (~44%). Barrick Gold accounts for less than 0.5%.

After bouncing a third of a percentage point against the Canadian dollar before the weekend, the US dollar is yielding to start the new week. In the middle of last week, the greenback dipped below CAD1.32 for the first time since January. The low for the year was set in early January a little above CAD1.2955. That is the next major target, but it seems well out of reach today. Instead, the intraday technical indicators warn of the risk that the greenback may recover toward CAD1.3260-CAD1.3270 today. The US dollar finished last week below the MXN22.00 support area and is holding mostly below there today. The greenback has a four-day drop in tow to start this week. Last month’s low was near MXN21.85 that is the next important chart area. Mexico’s high real and nominal rates continue to underpin the peso.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,COT,Currency Movement,Featured,Japan,newsletter