Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

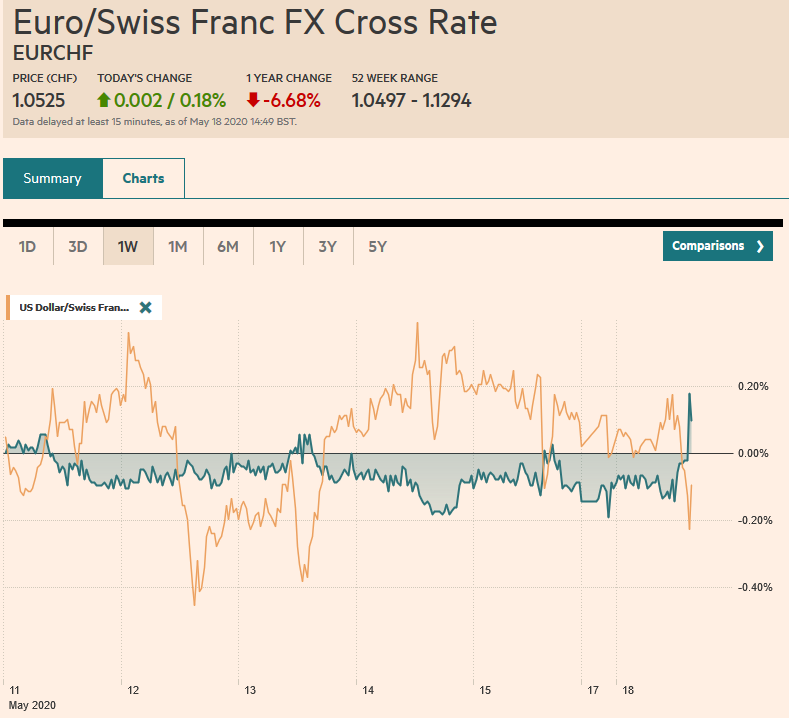

Swiss FrancThe Euro has risen by 0.18% to 1.0525 |

EUR/CHF and USD/CHF, May 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

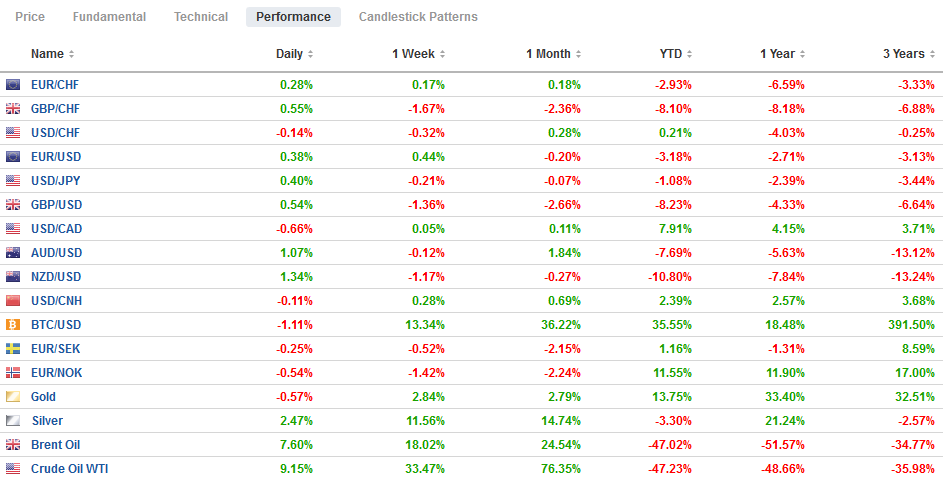

FX RatesOverview: Despite somber warnings that the US economic recovery can stretch to the end of next year, investors have begun the new week by taking on new risks. Most equity markets in the Asia Pacific region rose, with Australia leading the large bourses with a 1% gain. India was an outlier, suffering a 2.4% loss, and Taiwan’s semiconductor sector was hit, and the Taiex fell 0.6%. European markets are off to a strong start with a 2% gain in the Dow Jones Stoxx 600 to cut last week’s loss in half. The benchmark is approaching a two-week downtrend line near 399. US shares are higher, and this could lift the S&P 500 to test the key 2945-2955 area. The US 10-year yield is little changed near 64 bp, but European bonds are lit with peripheral yields off 4-8 basis points. The dollar is mixed. The dollar-bloc currencies and Scandis are firm, while the European complex and yen are heavier. Risk appetites are also evident among emerging market currencies, where the South African rand, Mexican peso, Turkish lira, and Hungarian forint are higher. The JP Morgan Emerging Market Currency Index is in a sawtooth pattern of alternating gains and losses for more than a week. It fell before the weekend and is higher now. The Russian rouble has been helped by the continued recovery in oil prices, where the July WTI traded above $31. Gold racing higher after pushing to new multi-year highs at the end of last week. The yellow metal is extending is advance for a fifth session and tested the $1765 area in Europe. |

FX Performance, May 18 - Click to enlarge |

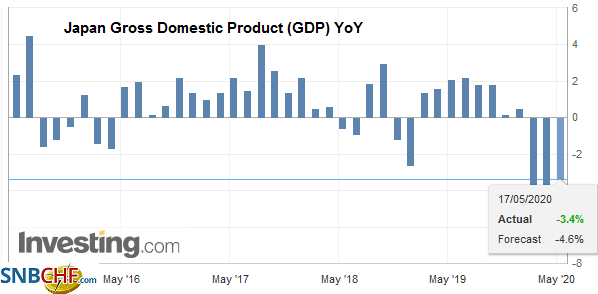

Asia PacificJapan reported its GDP contracted by 0.9% in Q1 or 3.4% at an annualized rate. It was a little better than expected though the Q419 loss was revised slightly to show a 1.9% quarterly contraction (earthquake and sales tax increase). This quarter understood to be considerably worse with expectations of a quarterly decrease of around 5.0-5.5%. Separately, even if not totally unrelated, the latest Asahi poll shows support for Prime Minister Abe is off about eight percentage points to 33%, the lowest in two years. The two big knocks include the handling of the virus and efforts to secure the power to appoint senior prosecutors. |

Japan Gross Domestic Product (GDP) YoY, Q1 2020(see more posts on Japan Gross Domestic Product, ) Source: investing.com - Click to enlarge |

At the same time that the US has announced a tighter ban on the sales of chips to Huawei, China took steps to dramatically increase its output of 14-nanometer wafers. Taiwan Semiconductor Manufacturing Corporation (TSMC) plans to build a wafer fabrication plant in Arizona needs to also be understood in this context too. The US prohibited without a license the sales of chips to Huawei if designed or made by US-produced technology and hardware. That would apply to TSMC, whose biggest customer is Huawei. The US export controls were circumvented by servicing Huawei out of foreign fabrication facilities. The new actions seek to close the loophole, and it seems that China had been preparing for this be stockpiling in semiconductor chips.

The dollar is confined to less than a third of a yen range above JPY107.00 and is within the pre-weekend range. So far, it is the first session in four that the dollar held above JPY107.00, though this could be challenged in the North American session today. On the top side, a $2.2 bln option at JPY107.50 expires today. After settling on its lows before the weekend, the Australian dollar bounced back to test the $0.6455 area. Resistance is around the pre-weekend high near $0.6475. The option for roughly A$635 mln at $0.6495 that expires today looks safe. A close blow $0.6440 would likely signal that the corrective forces remain in control. Given the heightened tension between the US and China and the greenback’s strength seen late last week, today’s PBOC fix was closely watched. The dollar’s reference rate was set at CNY7.1030, which was a bit stronger than the bank models suggested. The dollar reached its highest level since it peaked on April 2 near CNY7.1280. The highest close was on March 25 near CNY7.1150 and is under threat today.

Europe

Bank of England Governor Bailey reportedly denied that zero interest rates were under consideration last week. And the BOE’s chief economist Haldane seemed to suggest that negative interest rates were among the unconventional measures that were being considered. We suspect that the contradictory signals are more apparent than real. With the base rate at 10 bp, unconventional policy options are being discussed. Haldane was making this more academic point. Bailey was signaling the policy thrust, which is to say that expanding its asset purchase program holds more promise. The UK 2-year yield, which fell below zero last week, is now near minus five basis points.

The economic data highlight of the week is the preliminary PMI reports. The aggregate composite is expected to rise from the record low of 13.6 in April to 27.0 in May, according to the median forecast in the Bloomberg survey, as both the manufacturing and service sectors are forecast to improve. Ahead of the report, the European Commission is slated to announce its policy recommendations for a recovery package for next month’s meetings.

The euro is trading heavily but within the pre-weekend range. It has found a bid at $1.08, where a nearly 530 mln option will expire today. On the topside, the pre-weekend high was near $1.0850, and the 20-day moving average is just below there, likely keeping the $1.0875, expiring option for about 565 mln euros out of play. Sterling gapped lower (below $1.21) on the back of the talk of negative rates, but recovered to $1.2125 in the European morning. It is struggling to maintain the downside momentum that has seen it fall for five consecutive sessions coming into today. Note that the lower Bollinger Band is found near $1.2115 today. The Turkish lira’s short-squeeze is extending for its eighth consecutive session. News that Clearstream and Euroclear will not settle lira trades appears to have encouraged further buying back of previously sold lira positions. The US dollar found support near TRY6.81, as domestic demand (for debt servicing?) emerged.

America

The US calendar is light today. The highlight of the week includes the Philadelphia Fed survey (the Empire State manufacturing survey rose to -48.5 from -78.2) and the preliminary PMI (which is also expected to improve). April housing starts, and existing home sales will also be reported, and no fewer than eight Fed officials speak, including Powell (and Treasury Secretary Mnuchin) before the Senate Banking Committee tomorrow. Canada reports April CPI and retail sales figures this week. Mexico’s data highlight is the April retail sales report.

Conventional wisdom sees the negative yields in the US fed funds futures and concludes that investors are betting that the Fed cuts the target rate again. Some suggest that investors may be trying to push the Fed hand, deliver it a fait accompli, force it to cut, perhaps against its wishes. It is hard to argue against this. It seems intuitively true. Yet, the markets are not only about betting and taking on risk, but they are also for hedgers and people trying to layoff risk. The negative yields can be explained, even if no one thought the Fed would adopt negative rates. Imagine businesses that need to protect themselves against the chance. They buy “insurance” from the seller, who then goes to the market to layoff the risk. Financial intermediaries may also choose to hedge the risk of sub-zero rates. Negative rates in the US appear to be more about swapping from floating to fixed rates and the related hedging then actually reflecting expectations of negative Fed policy rates.

Brazil is being punished. The currency and equity market are among the hardest hit, losing a third of their value. It is not simply a function of macroeconomics. Policy matters. The self-inflicted political crisis adds to the challenge posed by the crippling pandemic. President Bolsonaro has lost the confidence of investors who had been prepared to like him after several tumultuous years. The loss of the second health minister in a month during a pandemic that appears to give Brazil the fourth most cases in the world.

The US dollar is consolidating within the pre-weekend range against the Canadian dollar (~CAD1.4020-CAD1.4120). A six-week downtrend line is found today near CAD1.4160. With stronger risk appetites today, initial support near CAD1.4060 would be pressured in North America. The greenback is also consolidating against the Mexican peso with a heavier bias. Lows from the end of last week around found near MXN23.75. Below there, support is seen around MXN23.50, which also corresponds to the lower Bollinger Band. The dollar posted a key downside reversal on May 14 against the Brazilian real. Still, the follow-through dollar selling ahead of the weekend was reversed in late turnover, and the greenback finished on session highs (~BRL5.8560). The dollar’s record high was set near BRL5.9715.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Bank of England,Brazil,Currency Movement,EUR/CHF,Japan Gross Domestic Product,negative rates,newsletter,USD/CHF