Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

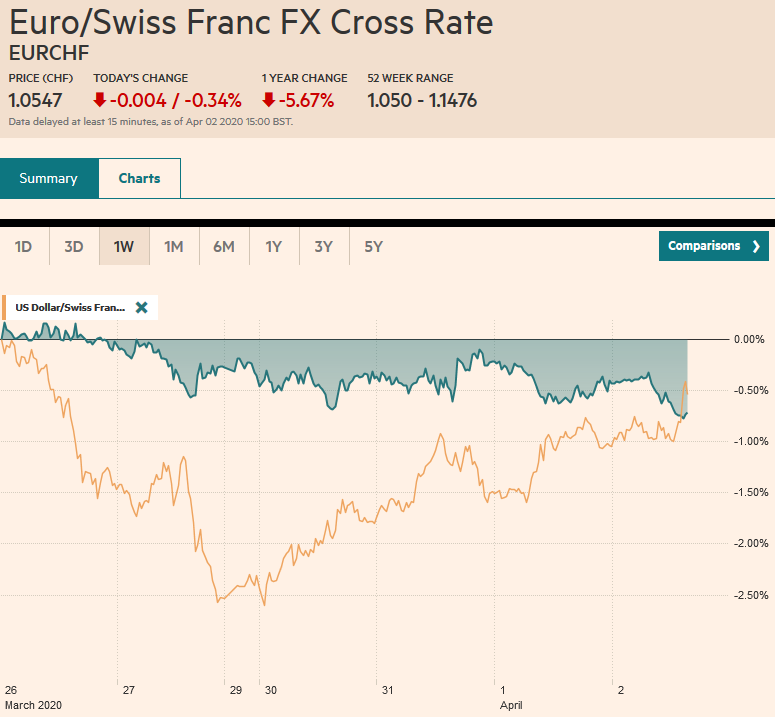

Swiss FrancThe Euro has fallen by 0.34% to 1.0547 |

EUR/CHF and USD/CHF, April 2(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

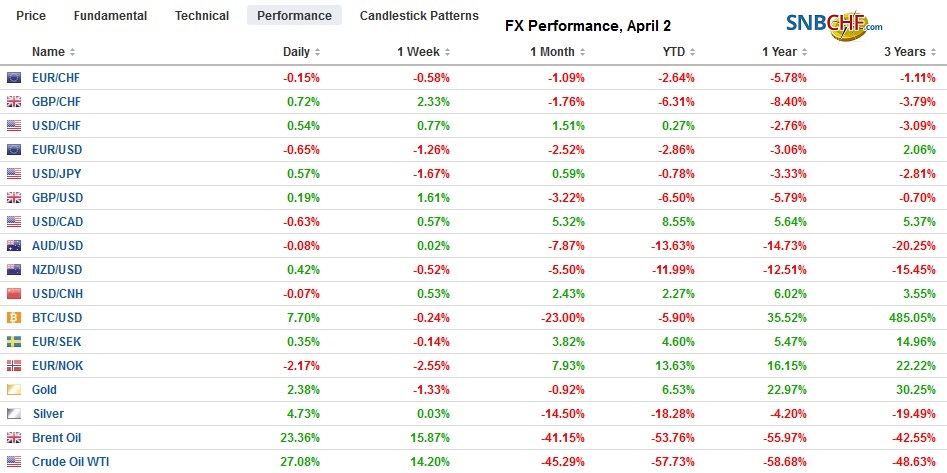

FX RatesOverview: After US stocks dropped more than 4% yesterday, investor sentiment has improved, apparently sparked by ideas that the pain will force oil producers to find a way to reduce supply. Oil prices have surged, with the May WTI contract rallying around 7%. Asia Pacific equities were mostly higher, with Japan and Australia the notable exceptions. The Dow Jones Stoxx 600 is a little firmer, but for the seventh consecutive session, it is chopping around the 300-320 range. US shares are stronger. The S&P 500 gapped lower yesterday, and that gap (~2522.7-2571.2) may offer a reference point today. Benchmark bond yields are two-five basis points higher, though the European peripheral bonds are performing a bit better in this environment. US 10-year yield is up a couple of basis points at 0.60%. The dollar is mixed among the majors with Norway and the dollar-bloc gaining ground, while yen, and especially the euro, have moved lower. The large liquid and accessible emerging market currencies are firmer, including the Russian rouble, Mexican peso, Turkish lira, and South African rand. Eastern and Central European currencies appear to be dragged lower by the euro’s weakness. Gold is holding below $1600. |

FX Performance, April 2 - Click to enlarge |

Asia Pacific

Foreign investors continued to divest themselves of Japanese assets last week, according to MOF data. Over the past two weeks, foreign investors sold about $56 bln (JPY6.1 trillion) of Japanese bonds. It appears to be the largest two-week liquidation on record. Foreigners have also been large sellers of Japanese equities. They have been selling for the past seven weeks (JPY5.6 trillion, or ~$50 bln), but accelerated in the past three weeks (accounting for JPY4.1 trillion of sales).

The US dollar rose to a six-month high against the Chinese yuan near CNY7.1280. The PBOC, which has been setting the dollar’s reference rate a bit weaker than the bank models suggest, set it stronger today (CNY7.0995 vs. the model average of about CNY7.0950). By the end of the local session, though, the dollar moved back into its old range. Tomorrow’s reference rate will be watched closely for signals of China’s intent. The offshore yuan did not show the same kind of movement. The dollar firmed but only to about a seven-day high (~CNH7.1425).

The dollar is in one of the narrowest ranges in weeks against the Japanese yen (~JPY107.05=JPY107.55). There are large options expiring today. In the JPY107.25-JPY107.50, there are options for $5.2 bln. Moreover, there are two other sets of options set to expire today. Below is the JPY106.90-JPY107.00 band that holds options for about $2.4 bln. Above are around $2.2 bln in options struck between JPY107.80 and JPY108.05. These option expirations may make for a quiet North American morning. The Australian dollar is around the middle of the $0.6000-$0.6200 range that has largely confined it for the past several sessions. The range is likely to hold today.

EuropeWhile we look at US jobs data below, European data often is less readily available, and several countries have followed Germany’s example of state-subsidized wages for workers put to part-time employment rather than let go. The UK recently announced such a program. However, reports indicate that between March 16 and March 31, the UK saw 950k people apply for universal credit benefits. This is a nearly 10-fold increase from a normal two-week period. The debate about Europe’s collective response is set to continue into next week when the Eurogroup of EMU finance ministers are due to propose to the heads of state the range of options. On the one hand, is the call for corona bonds. Southern European countries, including France, have been pushing for a collective bond since at least the sovereign crisis a decade ago. The creditor nations have balked at the mutualization of debt. Although this crisis has little to do with moral hazards, because several countries have not addressed their large debt levels, the creditors remain reluctant. The Dutch proposed a 20 bln euro fund, which seems wholly inadequate. German Finance Minister Scholz has proposed 200 bln euro funding from the European Stabilization Mechanism, of which half would be loaned to Italy. There is also an effort to focus on the EU’s budget (“Multiannual Finance Framework) as the main driver, as the ESM has been stigmatized. This is a fluid situation, though the lines of contention are clear, the resolution is less than obvious. |

Eurozone Producer Price Index (PPI) YoY, February 2020(see more posts on Eurozone Producer Price Index, ) Source: investing.com - Click to enlarge |

Today may be the first session since March 26 that the euro does not trade above $1.10, where there is an option for about 650 mln euros that expires today and another option for a billion euros that expires there tomorrow. The $1.09 area corresponds to a (50%) retracement of the last week’s bounce, and a break could signal a decline to the next retracement (61.8%) near $1.0835. Resistance is seen near $1.1040. Sterling has fared better It remains in a fairly narrow range below last week’s high near $1.25. There is an option for GBP580 at 1.2425 that may be of interest. A move above $1.2520 could spur a test on the 200-day moving average near $1.2665.

America

Investors were not persuaded by yesterday’s data. ADP estimate of private-sector employment fell by a mere 27k, and the manufacturing ISM slipped to 49.2 from 50.1. As we have seen in the PMIs, the longer supplier deliveries perversely lift the readings. New orders, on the other hand, fell to 42.2 from 49.8, and employment slumped to 43.8 from 46.9. Initial jobless claims soared to 3.28 mln in the week ending March 21. Economists expect today’s report to exceed it. There is good reason to expect it, rather than the monthly non-farm payrolls, for which the survey was conducted in the second week of March. Separately, the industry reported yesterday that US auto sales fell to 11.37 mln (seasonally adjusted annual rate) from 16.8 mln in February. It was the weakest since 2010 after bottoming in 2009 near 9 mln vehicles. Sales in March were about 35% lower than March 2019. Japan has also reported its March auto sales. They are off about 10% from a year ago. It gives a sense of the coming drop in retail sales and the accumulation of unwanted inventory.

The EIA reported a 13.8 mln barrel jump in US oil inventories. It appears to be the second largest in history (behind late October 2016). Not counting the US strategic reserves, there are about 469 mln barrels of oil in storages in the private sector. It is close to the five-year average for this time of year. Capacity is estimated at around 653 mln barrels, though this may overstate the case as above-ground tanks are never filled to the brim. Inventories rose every week in Q1 except for two in January. The average weekly increase in Q1 was 3 mln barrels, but as demand has fallen during the shutdown, the average over the last six weeks accelerated to nearly 4.4 mln barrels. In March alone, the average was closer to 6.3 mln barrels. Of course, the location of the storage is not equally distributed around the country. The industry focus is on Cushing, which s a major delivery point. Cushing saw an outsized jump of 3.5 mln barrels last week, which brings up the March average to 1.4 mln barrels a week. US government purchases for the strategic reserves would free up a bit more than 10% of the estimated private sector capacity.

Higher oil prices and firmer equity prices are helping lift the Canadian dollar. At the end of last week, the US dollar tested the CAD1.3920 area. Initial support today is seen near CAD1.4080, and a break could see CAD1.40 today. Separately, the Bank of Canada, which did not adopt QE policies in the Great Financial Crisis, has done so now, and yesterday was its first purchase. The US dollar climbed about 2.4% against the Mexican peso yesterday and is about 0.25% lower today. The greenback is in the upper half of yesterday’s range. More broadly, the US dollar is in a wide range of roughly MXN23-MXN25Mexico President AMLO remains reluctant to support fiscal stimulus to deal with the economic shock that is coming. He also does not want to use central bank reserves. Still, some health and economic measures are to be announced Sunday. Given the volatility and risk-appetites, or the lack thereof, Mexico’s high real and nominal rates are no longer a key attraction and now is seen as a detriment.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,capital flows,Currency Movement,EUR/CHF,Eurozone Producer Price Index,Japan,newsletter,OIL,USD/CHF