Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

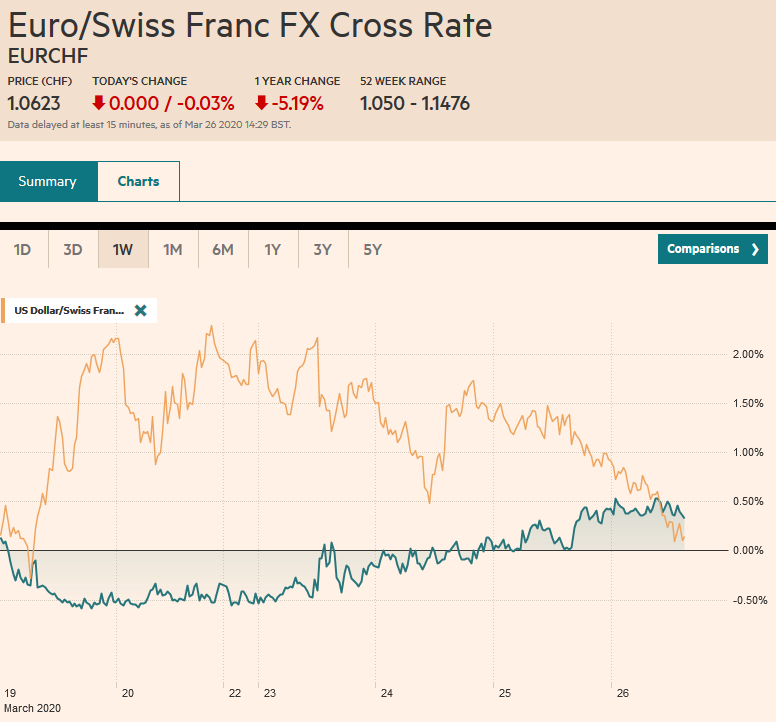

Swiss FrancThe Euro has fallen by 0.03% to 1.0623 |

EUR/CHF and USD/CHF, March 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

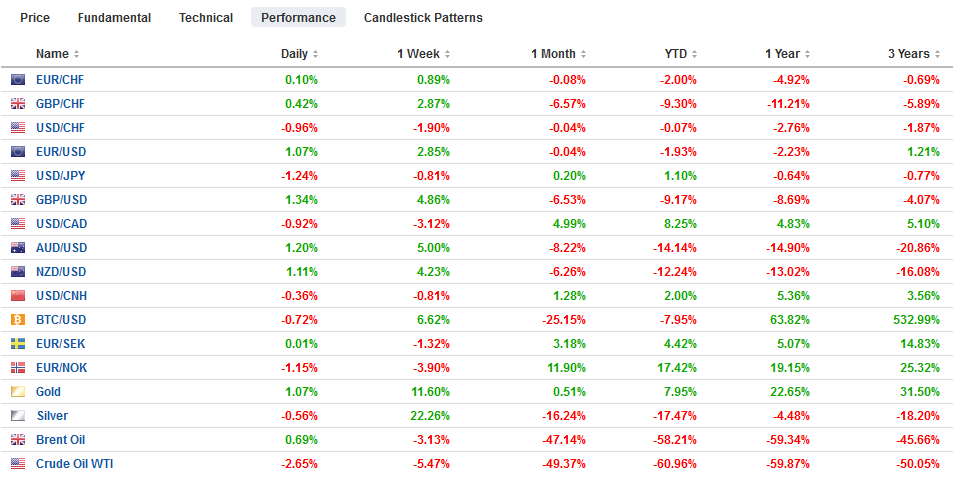

FX RatesOverview: Speculation that the US Senate would pass the large stimulus bill worth around 10% of US GDP is thought to have fueled a bounce in equities in recent days. The bill was approved and will now go to the House, where a vote is expected tomorrow. If the rumor was bought, the fact has been sold. The first to crack was the Asia Pacific region. Equities were mixed with the Nikkei shedding 4.5% and the Kospi off 1%. China and Hong Kong markets also slipped. Australia resisted and rose 2.3%. Indonesia, returning from yesterday’s holiday, played catch-up and jumped 10% (which also helped lift the rupiah). Led by energy, materials, and financials, Europe’s Dow Jones Stoxx 600 is almost 1.5% lower to snap a two-day 11.5% advance. The S&P 500 posted its first back-to-back gain since February 11-12 yesterday but is around 1.3% lower today. Benchmark yields are coming back softer with most major market yields are off 3-5 bp, while the European peripheral rates are off 9-11 bp, and Greece’s 10-year yield is off 28 bp. The US 10-year yield is around 6 bp lower at 0.80%. The greenback is softer against all the majors. The yen (~+0.9%) and euro (~+0.6%) are leading the way. Emerging markets currencies are mixed with several Asia Pacific currencies outperforming, while the more liquid and accessible ones are posting modest losses. Gold is lower for the second sessions while May WTI is giving back yesterday’s 2% gain in full. |

FX Performance, March 26 - Click to enlarge |

Asia Pacific

Although official figures show Japan, which had been one of the first countries outside of China to be infected, it has appeared relatively contained. However, Tokyo Governor Koike is urging residents to stay indoors and is warning that a lockdown may be imposed, as cases jumped. Separately, the BOJ continues to buy a record amount of ETFs. It bought JPY201 bln of ETFs today, matching the record of the previous two purchases.

Singapore is reported its biggest rise in infections so far after improvement had been seen. Singapore reported Q1 GDP contracted by 10.6% quarter-over-quarter. Economists in the Bloomberg survey had forecast an 8.2% decline. Industrial output imploded by 22.3% in February, skewed in any event by the Lunar New Year. Still, it was half again as high as the median forecast.

The People’s Bank of China appeared to protest the recent weakness of the yuan by setting the reference rate today considerably stronger (for the yuan) than the bank models suggested. The reference rate was set at CNY7.0692, about 100 bp lower (for the dollar) than the models implied. This is the most since China’s markets re-opened from the extended Lunar New Year holiday on February 3. The dollar is allowed to move 2% in either direction from the reference rate, while other currencies, such as the euro, are given wider berth. There is some thought that the PBOC is more concerned here with volatility than defending a specific level.

The three-month cross-currency basis swaps improved to around minus 50 bp from minus 80 bp late yesterday. It is the least in about two-weeks. The dollar had been bumping against a cap in the JPY111.50-JPY111.70 area but has pulled back today. It is approaching this week’s low, set Monday, near JPY109.65. A break of the JPY109.20 area could target the JPY108.30 area, where the 200-day moving average is found. There is a $740 mln option at JPY110 that will be cut today. The Australian dollar is fighting to extend its advance the fifth consecutive session. It reversed lower after reaching nearly $0.6075 yesterday and was sold to $0.5870 today before finding a solid bid. It is hovering around little changed late in the European morning. The intraday technicals suggest the risk is on the downside in North America today.

Europe

Germany’s Der Spiegel is reporting that the G7 was unable to reach an agreement on a statement. The report suggested that the US insistence on calling Covid-19 the “Wuhan Virus” scuttled the effort as other members refused. The World Health Organization is opposed to naming viruses after cities or countries, and the Spanish Flu did not originate in Spain.

Spain had its deadliest day so far, while the number of fatalities and new infections slowed in Italy, according to reports. The EU has approved Italy’s request to extend state guarantees for a debt moratorium from banks to small businesses. The ECB has clarified that its Pandemic Emergency Purchase Program (PEPP) announced last week (750 bln euros) will not be circumscribed by the capital key (roughly proportionate to GDP) as are its other sovereign bond purchase programs. This is important as it gives considerably more flexibility to the Eurosystem.

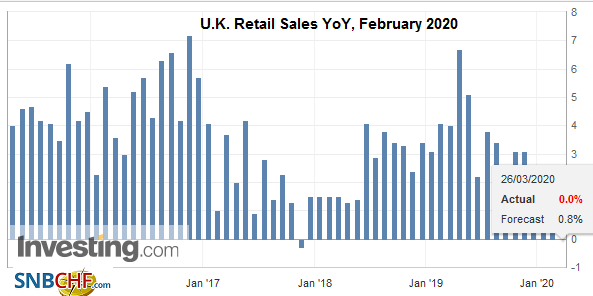

| The UK’s February retail sales fell by 0.5%, excluding auto fuel. Economists had been looking for a small decline, but the January series was revised up to a heady 1.8% (from 1.6%). The Bank of England meets today, and it is Governor Bailey’s first meeting at the helm. No change in policy is expected. The base rate was cut twice this month from 75 bp to 10 bp. |

U.K. Retail Sales YoY, February 2020(see more posts on U.K. Retail Sales, ) Source: investing.com - Click to enlarge |

The euro is advancing for the fourth consecutive session. It finished last week a little below $1.07 and is near $1.0950 in late European morning turnover. It is approaching the initial (38.2%) retracement of the slide March 9 high near $1.15 that is found by $1.0965. Above there is $1.10, where a roughly 840 mln option is struck that expires today. Sterling is firm but within yesterday’s range (~$1.1640-$1.1970). A move above $1.20 could spur a quick move toward $1.21, which is roughly the (38.2%) retracement objective.

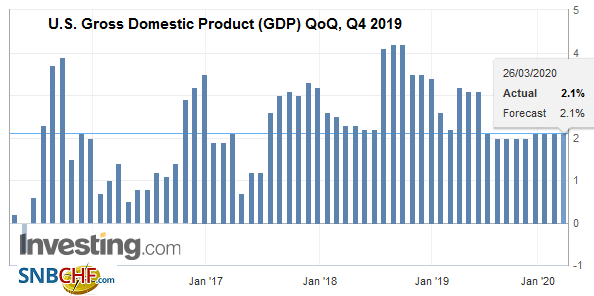

AmericaSt. Louis Fed President Bullard, who warned that Q2 GDP could contract 50% at an annualized pace and unemployment could surge to 20%, said yesterday what many economists also realize, weekly initial jobless claims are going to “skyrocket” for the week ending March 21. This report is the closest thing to a real-time read on the economy for businesses and investors. The median guesstimate in the Bloomberg survey has crept up to 1.65 mln (in recent days from 1.45 mln), which would be more than twice the previous record peak set during the Great Financial Crisis. There are some individual forecasts for more than twice the median. Outside of the weekly jobless claims, the US reports February goods trade figures and another look at Q4 GDP. The Kansas City Fed reports its March survey results. |

U.S. Gross Domestic Product (GDP) QoQ, Q4 2019(see more posts on U.S. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

Four-weeks through three-month US T-bills have slipped slightly into negative territory (an implied yield of around minus four-six basis points at an annualized rate). Bills are bought on a discounted basis (below the face value). They mature at face value, and the difference is the return. The implied negative yield means some are paying a little above face value. It is an expression of the incredible demand for liquidity and reveals systemic strain. It is an anomaly that is taking place in an emergency setting. Rates are negative in the EMU, Switzerland, and Japan, and they have been for several years. There is a reflection of policy, and given that, if rates were not negative, it would be evidence of dysfunction.

The bill that is likely to emerge from the US Congress does not have the $3 bln to fund the purchases of 77 mln barrels of oil to top up the Strategic Petroleum Reserves. The Trump Administration reportedly is looking to reallocate funds that have already been budgeted to the Department of Energy. Congressional approval is required, and it is often a rubber-stamp, but if part of the reason it was dropped from the bill on the grounds of aiding an unreformed carbon industry, it might not be traditional lay-up. Oil prices did not react much to US fiscal developments, and the May WTI contracted extended its recovery for a third session. US oil inventories are rising and now at the highest level since last July. Storage prices are already reportedly rising. While government purchases may not impact prices of crude, it could create more space in private storage. It seems that the rising cost of storage globally may discipline even low-cost producers. The projected global surplus, adjusted in light of the three-week lockdown in India, could be 2-3 times the ground storage space, according to some industry projections, in Q2. Lastly, another juxtaposition is taking place. After haranguing OPEC and Saudi Arabia to not keep artificially elevated oil prices, the Trump Administration has offered to mediate talks between the Saudis and Russians to stem the precipitous drop in prices.

The Canadian dollar has extended its recovery today. The US dollar reached almost CAD1.4670 on March 19 and is testing the lows since then near CAD1.4150. The greenback is heavier for the third consecutive session. A break of this area could signal a move toward CAD1.40, but the intraday technicals lean against this and appear more consistent with a push back toward CAD1.4300. The US dollar has fallen against the Mexican peso for the past two sessions (~5.7%). It has found support around MXN23.85-MXN23.90 after having set a record high near MXN25.46 two days ago (March 24). It is back above MXN24.00 as North American dealers set to return. Initial resistance is expected in the MXN24.40-MXN24.50 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Bank of England,EUR/CHF,negative rates,newsletter,U.K.,U.K. Retail Sales,U.S. Gross Domestic Product,USD/CHF