Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

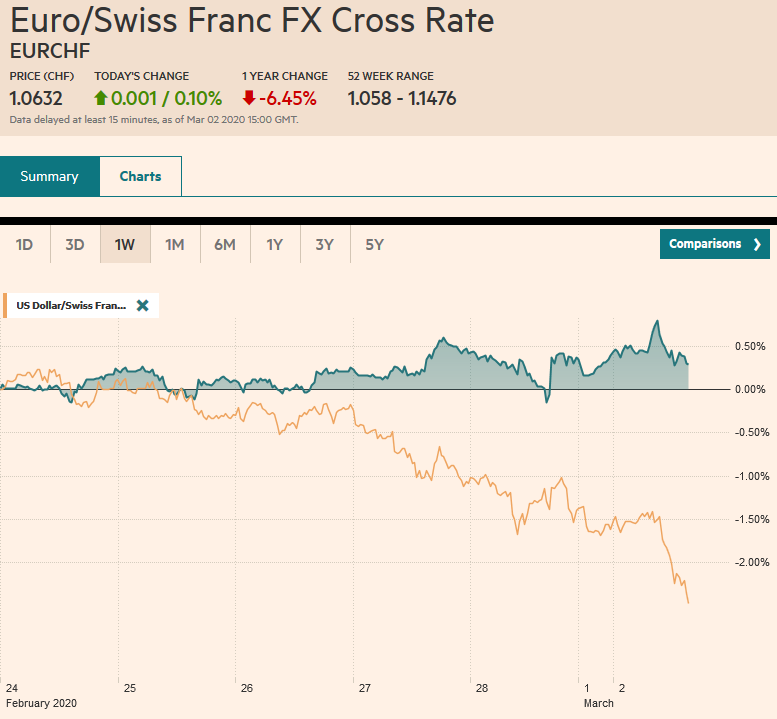

Swiss FrancThe Euro has risen by 0.10% to 1.0632 |

EUR/CHF and USD/CHF, March 2(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Comments beginning with Powell before the weekend, and BOJ and BOE earlier today promising support have saw equity markets briefly stabilize after last week’s dramatic moves. The G7 will hold a teleconference this week, but speculation of a coordinated rate move does not seem particularly likely. Most of the large stock markets in the Asia Pacific region rallied, led by a 3%+ advance in China. Japan’s indices gained nearly 1%, while Hong Kong and South Korea’s markets advanced too. Australia and Taiwan were exceptions and slipped lower. Europe’s Dow Jones Stoxx 600 rose about 1.5% in the morning, helped by a rebound in energy and health care, but reversed lower by midday. US shares were also trading firmer but surrendered the initial gains. Bond markets have continued to rally. Core European bond yields are off 4-5 bp, while the yield of the 10-year US Treasury is nearly eight basis points lower near 1.06%. The dollar is weaker against most of the world’s currencies today, with sterling the main exception among the majors, and the Indian rupee and Mexican peso the notable exception among emerging market currencies. Gold has rebounded with equities. Its 1.5% gain puts near $1610. Oil prices have also rebounded. Light sweet crude for April delivery is snapping a six-day drop with a 2.3% gain that lifts it toward $46 a barrel. |

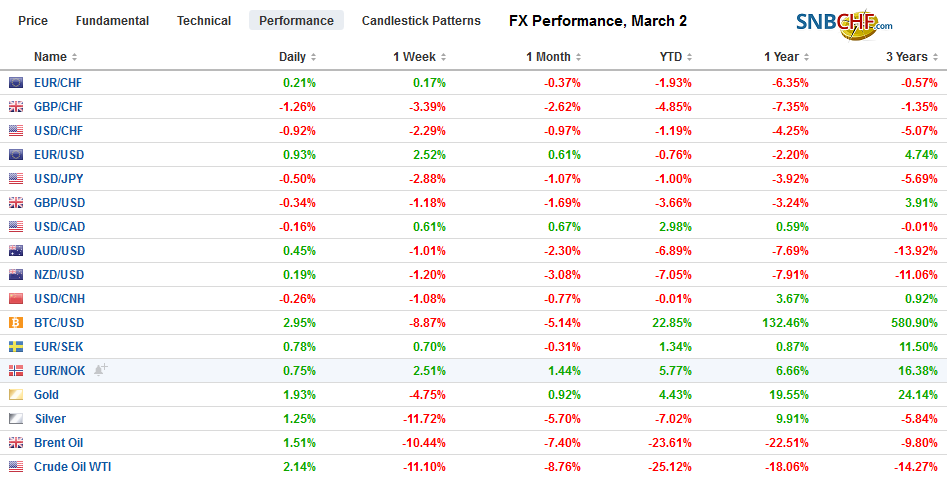

FX Performance, March 2 - Click to enlarge |

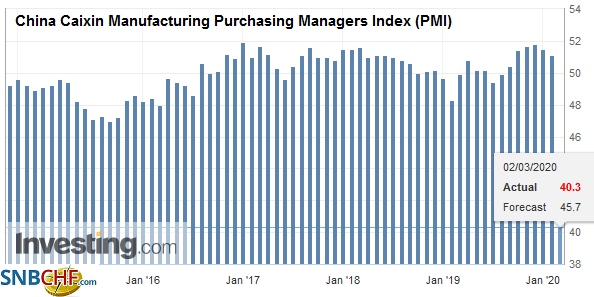

Asia PacificChina’s February PMI was dreadful. The composite PMI crashed to a record low of 28.9, almost 10-index points below the low from the Great Financial Crisis. The non-manufacturing sector slumped to a record low as well (29.6 vs. 54.1). The manufacturing PMI was already struggling, and in January was at exactly the 50 boom/bust level. It dropped to 35.7 in February. The details were horrific. Production, new orders, and new export orders fell below 30. The Caixin manufacturing PMI fell to 40.3 from 51.1. The data is not that surprising given that good parts of the economy were shutdown. However, there is evidence over the past two weeks that economic activity is taking place, and officials claimed over the weekend that 90% of the state-owned businesses have resumed operations. |

China Caixin Manufacturing Purchasing Managers Index (PMI), February 2020(see more posts on China Caixin Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The Bank of Japan indicated it will provide loans to support bank lending to businesses that have been hit by the coronavirus. It will offer JPY500 bln (~$6.6 bln) in new JGB repos. The Abe government will tap into the current budget’s reserves for JPY270 bln (~$2.5 bln) to help stabilize the markets. Separately, the final manufacturing PMI edged up to 47.8 from the flash reading of 47.6. It was at 48.8 in January and has not been above 50 since last April. |

Japan Manufacturing Purchasing Managers Index (PMI), February 2020(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

Australia’s manufacturing PMI rose to 50.2 from the flash reading of 49.8. It was at 49.6 in January and 49.2 at the end of last year. It is the second consecutive monthly advance, the first since last May and June. The Reserve Bank of Australia meets tomorrow, and the market has fully discounted a 25 bp rate cut.

Beware of news that South Korean exports rose 4.5% in February, the first year-over-year increase in more than a year. There were four more working days this year than in 2019 due to how the Lunar New Year fell. The daily average was off about $1.83 bln or nearly 12%. Exports account for around half of South Korea’s GDP. South Korea’s manufacturing PMI fell to a four-year low of 48.7 (from 49.8). New stimulus measures are being cobbled together. The extra budget will be unveiled Thursday, and it is expected to be larger than the KRW6.2 trillion (~$5.1 bln) spent on support during the MERS outbreak in 2015.

As one would expect, the manufacturing PMIs in emerging Asia were poor. Taiwan’s fell to 49.9 from 51.1. Thailand and Malaysia remained below 50, and the latter is expected to cut its overnight rate tomorrow by 25 bp to 2.50%. Vietnam’s PMI fell to a six-year low of 49. Indonesia’s manufacturing PMI fell to 49.3 from 51.9.

The dollar initially gapped lower against the Japanese yen and fell to nearly JPY107 before recovering to almost JPY108.60 in late Asian turnover. The greenback has come off to test the JPY107.50-JPY107.70 area. There are options for around $1.5 bln today in the JPY108.20-JPY108.30 area that expire today. The Australian dollar is firm within the pre-weekend range (~$0.6435-$0.6580). A move above $0.6600 would lift the technical tone, but participants may be reluctant ahead of the RBA decision. The PBOC set the dollar’s reference rate at CNY6.9811, a little weaker than the models anticipated. The dollar fell to the lower end of the range that has dominated since the Chinese markets re-opened after the Lunar New Year holiday (CNY6.95-CNY7.05).

Europe

Thus far, Italy has been the most seriously struck by the Covid-19 in Europe. It was already on the brink of a recession. The government has announced a 3.6 bln euro stimulus package, which includes tax credits for businesses that have lost 25% or more of their revenue, for example, and new health-care spending. It will formally request the EC approval for the plans that amount to about 0.2% of the GDP on top of the 900 mln euros unveiled before the weekend. Italy’s former Prime Minister (2016-2018) Gentilioni is the new EC Commissioner for Economic Affairs.

| The final EMU manufacturing PMI edged up to 49.2 from the 49.1 flash reading. It was the second consecutive increase. It stood at 46.3 in December and 47.9 in January. While still below 50, there were some small upward revisions in output and new orders. Germany’s manufacturing PMI rose to 48.0 from the 47.8 flash reading and 45.3 in January and 43.7 in December. The French reading was revised to 49.8 from 49.7 flash report, but down from the 51.1 in January, confirming the first sub-50 reading since last July. Italy’s manufacturing PMI slipped to 48.7 from 48.9, while Spain surprising on the upside with a 50.4 report, up from 48.5 in January and 47.4 in December. |

Eurozone Manufacturing Purchasing Managers Index (PMI), February 2020(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The UK’s manufacturing PMI slipped to 51.7 from the advanced reading of 51.9. However, it confirms the recovery since the election. Last December, it was at 47.5. In January, it rose to 51.0. Sterling, however, found little comfort in the PMI. Instead, market participants focused on a high-level resignation over the weekend that points to infighting in Johnson’s government. Negotiations with the EU begin today about the new trade relationship. The talks will start acrimoniously. Johnson has threatened to walk away as early as the end of Q2 if there is little progress toward the Canada-like free trade agreement.

Turkey is not getting the kind of support from Europe that seeks in its war against Russian-backed Syrian government forces. It is deploying its primary source of leverage against Europe. It re-opened its borders to allow some of the 3.7 mln Syrian refugees to flee into Europe. Greece is the frontline and claims to have stopped more than 10k refugees at its border. Greece has invoked an emergency clause of an EU treaty to ensure broader support.

The euro’s recovery was extended to almost $1.11. It has seen a low of about $1.0950 before the weekend. Recall it finished January a little below $1.11 as well before falling to a little below $1.0780 on February 20. The $1.1065 area corresponds to a (61.8%) retracement of this year’s decline. The 200-day moving average is also just below $1.11 today, and the euro has not closed above since mid-January. There are two option expirations of note. The first is for 1.8 bln euros at $1.1050, and the other is for about 570 mln euro at $1.1130. Sterling is largely confined to the lower half of its pre-weekend range and has been unable to rise above $1.2850. The pre-weekend low was near $1.2725, and the 200-day moving average is closer to $1.2700. The intraday charts suggest sterling is poised to recover in North America today.

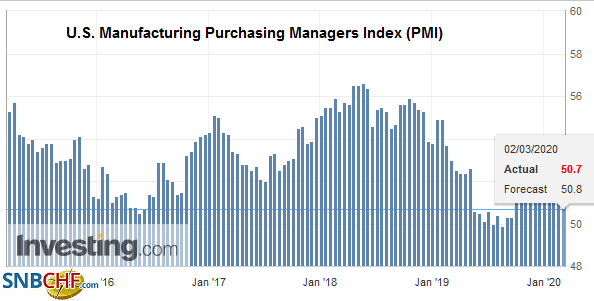

AmericaWhile the US sees the PMI and ISM reports, the focus is on the Federal Reserve, following Powell’s statement while the markets were open before the weekend. Speculation of a rate as early as today is elevated. Although we are skeptical, if such a move does take place, the recent history as limited as it is, suggests such a move would be delivered before the equity market opens. The March fed funds futures appear to have more than a 50 bp cut discounted, and if there is no cut today, the pricing will have to adjust. |

U.S. Manufacturing Purchasing Managers Index (PMI), February 2020(see more posts on U.S. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

There continues to be talk about negative rates in the United States. Our experience with negative rates is limited. However, there are a couple of characteristics that countries with negative rates have shared. First, no country has had negative yields bonds without the central bank pushing the policy rate below zero. This does not seem likely in the US, given Fed comments in recent years. Second, negative rates have been adopted by central banks that have current account surpluses (savings > investment). The US has a current account deficit (savings < investment).

Canada and Mexico also report February manufacturing PMI. The Bank of Canada meets Wednesday, and speculation of a rate cut has mounted in recent days. The market is pricing in about a 1-in-3 chance of a cut. It was closer to a 1-in-7 chance in the middle of February. Mexico’s central bank does not meet until March 26. The peso’s weakness could interrupt the central bank’s easing cycle. Mexico’s high real and nominal rates may help the peso recover quickly once the stability in the capital markets is assured.

The US dollar fell to about CAD1.3315 today after testing CAD1.3465 at the end of last week. With today’s losses, the greenback has retraced nearly 61.8% of its rally since February 21 low near CAD1.32. The intraday technicals suggest the range may be in place for the day. Look for consolidation in North America. The dollar briefly traded above MXN20.0 for the first time in six months. It pullback back to MXN19.50 before new dollar bids emerged. Near-term consolidation here also seems like the most likely scenario.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,central-banks,China Caixin Manufacturing PMI,COVID-19,Currency Movement,EUR/CHF,Eurozone Manufacturing PMI,federal-reserve,Japan Manufacturing PMI,newsletter,U.S. Manufacturing PMI,USD/CHF