Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

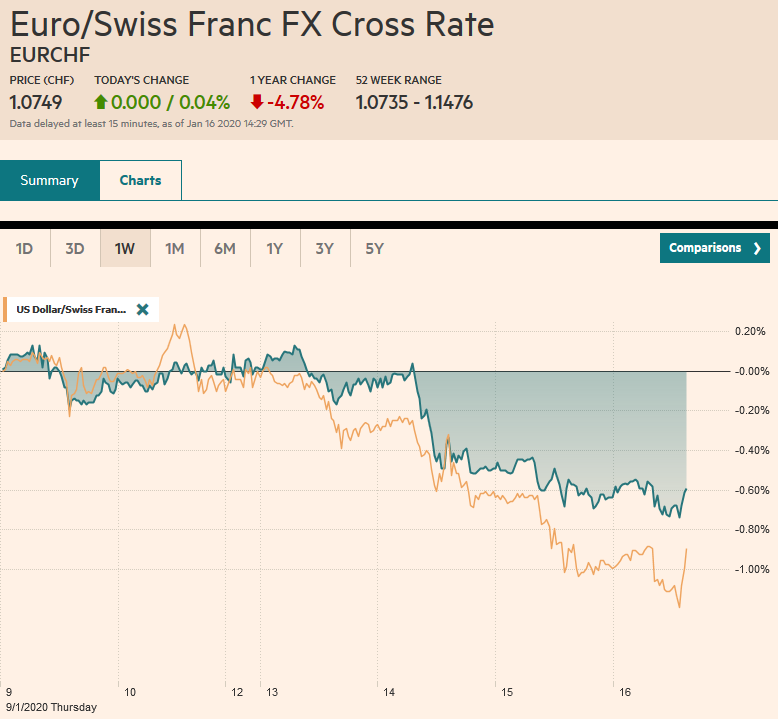

Swiss FrancThe Euro has risen by 0.04% to 1.0749 |

EUR/CHF and USD/CHF, January 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The global capital markets are calm today as investors await fresh trading incentives. New record highs in the US equity indices gave Asia Pacific stocks a lift, though China and Taiwan were notable exceptions. Europe’s Dow Jones Stoxx 600 is firm new record highs set last week. US equities are edging higher in Europe. Benchmark bond yields are little changed. European yields are a little lower, while the US 10-year is steady around 1.78%. UK short-term rates are steadying after their recent drop as the market discounts a greater chance of a cut later this month. The dollar is trading lower against the major currencies, but the Japanese yen in quiet turnover. Emerging market currencies are mostly lower ahead, though the yuan recouped yesterday’s decline. The market awaits the South African (expect steady policy), and Turkey’s 75 bp rate cut was anticipated. Gold is paring yesterday’s gains, and the decline in US oil inventories may be lending crude some support. |

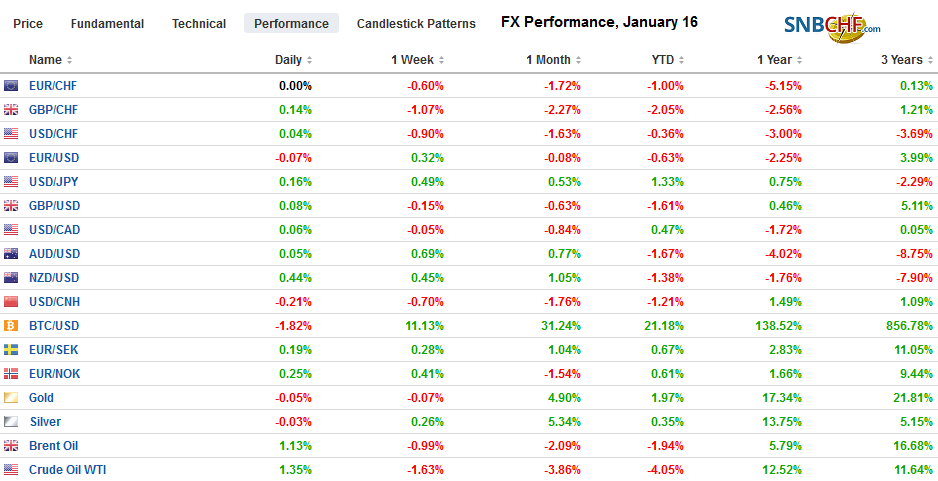

FX Performance, January 16 - Click to enlarge |

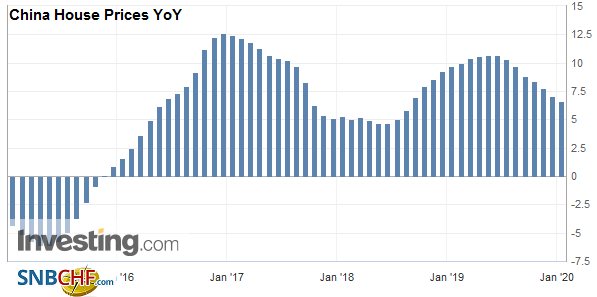

Asia PacificJapan’s sales tax increase distorts some high-frequency data. It impacts economic activity as it was brought forward. The tax increase also affects prices. Both of these were seen in today’s data. Core machine tool orders jumped 18% in November, around six-times greater than expected after a 6% drop in October. This is seen as a good indicator that capex will bounce back quickly. Separately, producer prices rose 0.1% in December, but 0.9% year-over-year. Recall there were negative year-over-year readings from June through October 2019. The BOJ meets next week. Although policy is unlikely to change, the central bank will offer new forecasts. China’s lending figures showed bank lending slowed in December, while the shadow banking lending rose. Bank loan growth eased to CNY1.14 trillion from CNY1.39 trillion. Aggregate financing quicken to CNY2.1 trillion from CNY1.75 trillion. The difference between the two is a useful proxy for shadow banking activity. The average aggregate financing in 2019 rose to CNY2.13 trillion from CNY1.87 trillion in 2018. Given the debt-led growth reliance in China, better lending figures seem consistent with the stabilization of the economy. |

China House Prices YoY, December 2019(see more posts on China House Prices, ) Source: investing.com - Click to enlarge |

The dollar has been confined to about a 10-tick range on either side of JPY109.95. Recall Tuesday’s high was near JPY110.20. There is an option for $1.8 bln at JPY110 that expires today. Near-term direction cues may come from other capital markets. The side of the risk-on mode that weighs on the yen is helping support the Australian dollar, which is testing the upper end of its recent range near $0.6920. Above there, resistance is seen in the $0.6940-$0.6960 area. The Chinese yuan remains firm though it is below the high set earlier this week that saw the dollar trade near CNY6.8670. The continued firmness of the yuan seems to go against the impulses from the monetary stimulus. The PBOC cut reserve requirement to start the year, and the new benchmark, the loan prime rate, is expected to slip lower when it is set in a few days.

Europe

The ECB meets next week, and the new strategic review (how to measure and implement price stability target appears to be the key focus) will be fleshed out. The record from Lagarde’s first meeting will be reported shortly. Going forward, we expect the record to change more in line with the practices of other central banks. Room for dissents will remove the perceived need for those that lose debates to take the case to the press.

The strategic retreat by French President Macron on boosting the age to draw on full retirement benefits does not appear to be enough to appease the critics. Labor unions are organizing for widespread demonstrations at the end of next week.

The short-end of the UK curve is stabilizing after investors upgraded the chances of a rate following recent official comments. The June short-sterling futures implied no change (at 75 bp) as recently as a week ago. It reached 54 bp earlier today, a marginal new low, before steadying. Some caution may indeed be in order ahead of tomorrow’s December retail sales report, which is expected to show UK consumers returned to the shops after declining by 0.6% in November (with and without petrol).

Although Turkey’s inflation rose to 11.84% in December from 10.56% in November, the central bank appears to be under political pressure to cut rates today from 12% (one-week repo rate). It delivered a 75 bp rate cut (to 11.25%) Leaving aside the loss of central bank independence, a cut will bring the real rate (inflation-adjusted) below zero. The risk is a vicious cycle, where rates do not fully compensate for the inflation (and other risks), weakening the currency over time and fanning price pressures. In contrast, South Africa’s inflation was 3.6% in November, and the December reading, out next week, is expected to see an uptick through 4%. The average repo rate stands at 6.5%, and the central bank is expected to stand pat today.

The euro is in about a 10-tick range on both sides of $1.1155 and in the middle of the range seen in the first half of January. There are a little more than two billion euros in options struck between $1.1100 and $1.1110 that expire today and more tomorrow. If the downside looks protected, the upside seems capped in the $1.1180-$1.1200 area. Sterling is firm near the week’s highs (~$1.3065). The euro has met offers in the GBP0.8600 area, which, coupled with the softer dollar tone, maybe offering sterling some support. Nearby resistance against the dollar is seen in the $1.3080-$1.3100. The political changes in Russia do not seem to change the underlying status quo and Putin’s ability to dominate. Russian yields are a couple basis point lower, and the rouble has been under a bit of pressure since recording roughly 18-month highs at the start of the week.

AmericaIt is striking that most of the initial assessments of the new US-China trade agreement seemed to be critical for not going far enough. Some argued it is not as ironclad as the administration suggests. Others were disappointed that the currency section was not more robust. It does not seem to go beyond the G20 and IMF commitments and mostly have been met: reserves, trade, and the financial account are reported in a timely fashion. Many economists and observers, including the IMF, do not think that China has been manipulating the yuan to gain a competitive edge. Direct intervention in the foreign exchange market has been virtually non-existent. Also, China has made recent moves to strengthen intellectual property rights and is opening more of its financial sector to foreign investors. There is some concern that with Boeing’s woes, long-term contracts in natural gas, export controls, may be used as a loophole. It is possible, and maybe even likely, that while the US bilateral deficit with China narrows, it grows with the rest of the world. |

U.S. Retail Sales YoY, December 2019(see more posts on U.S. Retail Sales, ) Source: investing.com - Click to enlarge |

At the same time, there is an innovation or a departure from the US traditional approach. Previously, the US focused on establishing rules. Pax Americana was rules-based. Trump negotiated an outcome-based treaty. This follows from economic nationalism and the abandonment of the Open Door (multilateral trading system eschewing tariffs and barriers to trade). Previously, the US advocated a rules-based system become it fit into the US political culture, and it was confident that it could win under those rules. Confidence has been sapped. The kind of globalization that the US used to advocate is out of fashion on both the right and the left. Many think it is losing under those rules. They argue that the rules were not designed for current problems and, in particular, the rise of China. The rules can always be gamed, so the alternative is to seek specific outcomes and can be monitored, and violation allows for retaliation.

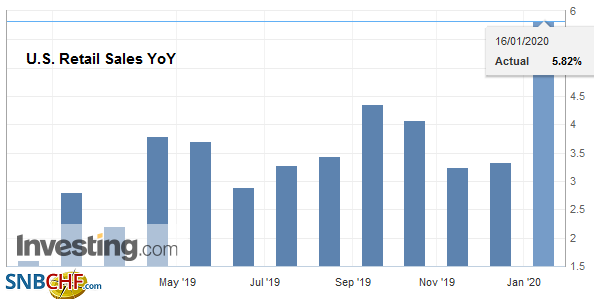

The highlight of today’s US economic data includes the Philadelphia Fed survey, which is among the first reading of economic activity in the new year, and retail sales that will likely show that American consumers were shopping at the end of last year. The Philadelphia Fed survey has softened for four of the last five months and is expected to have edged higher in January. Retail sales likely accelerated from the below-par November levels. The median forecast in the Bloomberg survey expects a 0.3% rise at the headline level and 0.5% excluding autos (from 0.1% in November). The components used for GDP calculation is likely to accelerate to 0.4% from 0.1%. This “core” measure rose by an average of 0.6% in the first 11 months of 2019. With a 0.4% rise in December, the average in Q4 would be a little less than half the long-term average. The US also reports weekly jobless claims, import/export prices, and the Treasury’s International Capital report (TIC). Canada and Mexico’s economic calendars are light. The US Senate could vote to approve the USMCA today.

The US dollar stalled near CAD1.3080 on Tuesday and Wednesday and has slipped back toward CAD1.3030 today. Chart support is seen near CAD1.30 today. The daily technical readings are still supportive of the greenback, but a break of CAD1.30 would likely weaken the outlook. The Bank of Canada meets next week. No change in rates is expected, but the rhetoric/forward guidance may soften a bit more within the neutral framework. The US dollar remains in tight ranges against the Mexican peso, hovering around MXN18.80. The dollar has not finished above MXN18.82 since January 7 or below MXN18.7820. The Dollar Index is trading at new six-day lows (~97.15). The next support area is seen between 96.80 and 96.95.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,China House Prices,Currency Movement,ECB,EUR/CHF,newsletter,Trade,U.S. Retail Sales,USD/CHF