Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

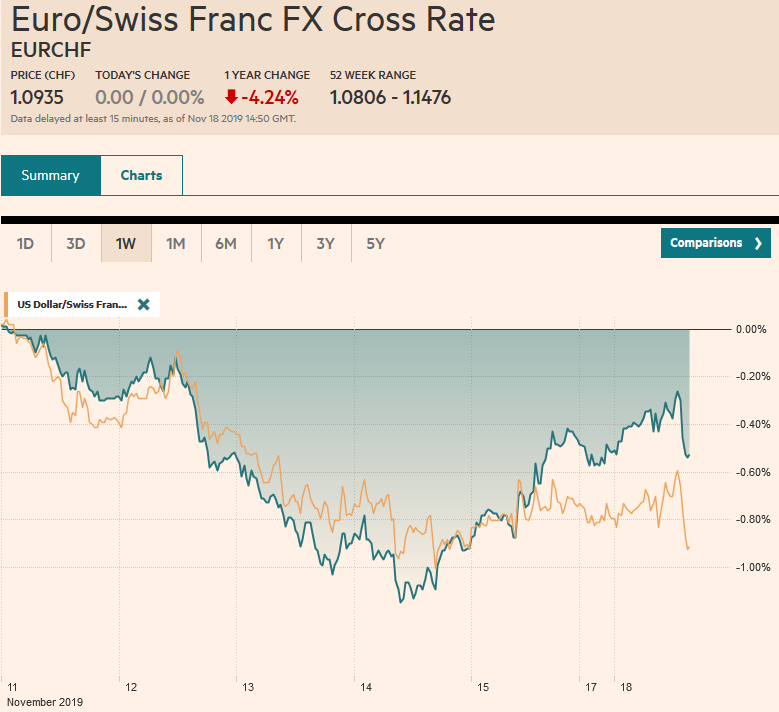

Swiss FrancThe Euro has unchanged by 0.00% to 1.0935 |

EUR/CHF and USD/CHF, November 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Equities in Europe and the US look to extend their six-week rally, while the MSCI Asia Pacific Index gets back on the winning way after stumbling last week. Despite the escalation of the conflict in Hong Kong, the Hang Seng rose 1.35% to lead the region and recoup a chunk of last week’s 4.8% slump. The Dow Jones Stoxx 600 puts the European benchmark within spitting distance of the four-year high set recently. The S&P 500 gapped higher at the start of last week to new record highs. It is poised to gap higher again today. Equities are where the movement is today as bond yields and the currencies markets are quiet. Core bond yields, including US Treasuries, around a basis point firmer, while peripheral bond yields in Europe are a little softer. Against the majors, the dollar is little changed, with two exceptions. Sterling is the strongest, up around 0.5% (~$1.2960) aided by optimism that the Tories will win next month’s election. On the other hand, the yen is softer as the dollar retests the JPY109 area. Emerging market currencies are mixed. he South African rand and Mexican peso lead the laggards, off 0.25%-0.33%, while the Turkish lira (+0.25%) and the South Korean won (+0.20%) lead the advancers. Gold giving back most of last week’s 0.65% gain and oil prices are little changed. |

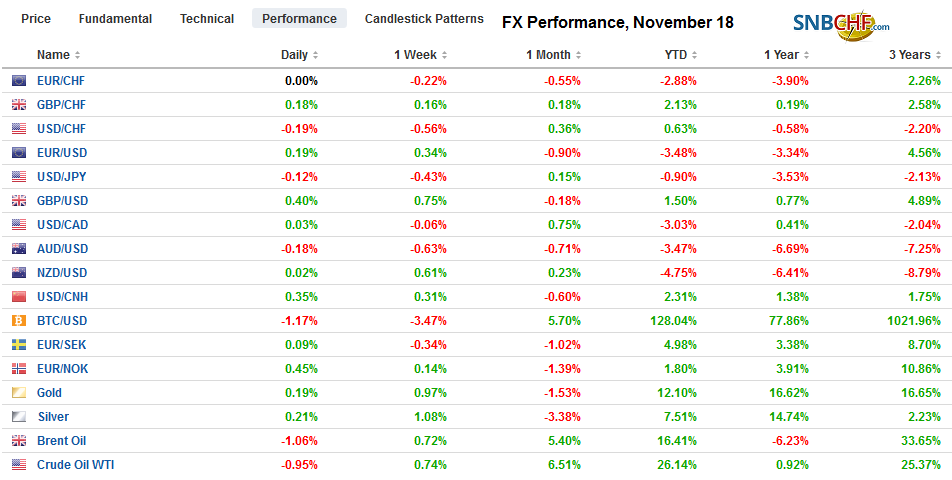

FX Performance, November 18 - Click to enlarge |

Asia Pacific

China shaved the seven-day reverse repo rate by five basis points to 2.50%. It follows a similar reduction in the medium-term loan facility two weeks ago. The strength lies in the signaling. The PBOC also injected CNY180 bln ($26 bln) via an open market operation. The 10-year yield eased four basis points and at 3.2% is the lowest in a month.

The escalation of force in Hong Kong and the pitch battles between the demonstrators and police are putting this coming weekend’s local election (November 23) at risk. Meanwhile, the US Senate is expected to take up the House bill that requires an annual affirmation of Hong Kong’s autonomy to continue its special trade privileges.

Singapore, as an entrepot (commercial and financial center), is closely watched for insight into larger trends. The October trade data were released and showed a little serially improvement, but not as much as economists expected. Non-oil exports fell 2.9% from September after a 3.3% decline. Economists had hoped for less than a 1% fall. Year-over-year, non-oil were off 12.3% compared with 8.1% in September and is the worst showing since June. Electronic exports fell 16.4% from a year ago after a 24.8% decline in September.

Japan will report October trade figures tomorrow. Exports and imports are expected to have deteriorated. However, the balance is expected to return to surplus after deficits were recorded in the past three months. In the first nine months of the year, Japan has recorded a trade deficit of JPY1.42 trillion. In the same period a year ago, a surplus of JPY26.6 bln was recorded.

The dollar has bounced smartly off last week’s low near JPY108.25 to retest air above JPY109 today. A $485 mln option is struck there and expires in the US session today. It also corresponds to the 200-day moving average and the (61.8%) retracement objective of the decline since the JPY109.50 high on November 7. The intraday technicals are over-extended in the European morning. The Australian dollar is consolidating in a narrow range above $0.6800. The gain before the weekend snapped a five-day slide, but the technical damage remains. A move above the $0.6840 area is needed to begin repairing the damage. After drifting lower in the last two sessions, the US dollar firmed against the Chinese yuan, where it is consolidating between CNY7.01 and CNY7.02.

Europe

UK Prime Minister is set to reach out to business today promises of some tax relief and new spending. The first televised debate will be held tomorrow. The weekend polls all show the Tories ahead of Labour. Meanwhile, at least eight previous Brexit Party candidates, who were told they could not run in Tory-held districts, may mount independent candidacies, according to press reports. The issue is not so much whether the Tories win the most votes, it is whether it can secure a majority in the House of Commons.

It is a relatively quiet week for EMU data. The highlight is the flash PMI at the end of the week. It is expected to show a nascent recovery in the region. Many fear that the weakness in the manufacturing sector will hamper services. Still, instead, the resilience of services, which speaks to the domestic economy, is likely putting a floor under the manufacturing industry, depressed by external developments and specific challenges to the auto sector (e.g., new emission standards).

The $1.1060 area the euro is testing corresponds to a (38.2%) retracement of the decline from near $1.1180 seen near the start of the month. The next retracement objective is closer to $1.1080, where the 20-day moving average is also found. There is a 1.3 bln euro option struck at $1.1055 that expires in a few hours. Support now is pegged near $1.1030. Sterling reached $1.2985, its highest level since October 22. It appears to be breaking out of the consolidative triangle pattern, which, if confirmed, projects toward $1.3200. However, the intraday technical indicators are stretched, and there may be little incentive to punch above $1.30 today, where a GBP255 mln option is struck that is also set to expire.

America

A quiet calendar starts the new week. The US reports the Treasury’s International Capital report (TIC) after the markets close today, and the Fed’s Mester is the only speaker today. The minutes from last month’s FOMC meeting will be released at mid-week. Mexican markets are closed for a national holiday. Canada reports CPI (Wednesday) and retail sales (Friday). The US is expected to grant another reprieve for domestic buyers of Huawei for the third time, but the product-specific licenses that would allow US companies to sell non-sensitive products/services to Huawei have yet to be granted. Separately, the APEC summit that was supposed to see Trump and Xi sign-off on the handshake agreement supposedly struck a month ago was canceled due to unrest in Chile, but the deal has not been struck yet.

One would hardly know it by looking at the US equity market (record highs) or yields (the 10-year yield ~1.84%, the upper end of a three-month range) that the Atlanta and New York Fed’s GDP trackers are warning the US economy is nearly stagnating. Household spending, capital expenditures, residential investment, and inventories were downgraded. The Atlanta Fed model sees Q4 GDP at 0.3%, and the NY Fed estimate is 0.4%.

The US dollar was turned back in the second half of last week after approaching the 200-day moving average against the Canadian dollar (~CAD1.3275). It fell to almost CAD1.3215 before the weekend and has drifted closer to CAD1.3200. A today’s lows, it has retraced (38.2%) of the rally from the November 5 low near CAD1.3115. The next retracement (50%) is found near CAD1.3195, but it will likely take a move below CAD1.3175 to convince others that a top is in place. Resistance is seen in the CAD1.3230-CAD1.3240 area today. The dollar is drifting higher against the Mexican peso after being setback at the end of last week, following Banxico’s as expected 25 bp rate cut and a relief rally in Chile. The intraday technicals are a bit stretched as the North American session is about to begin. Initial resistance is seen near MXN19.26-MXN19.27. The pre-weekend high was around MXN19.33. The Dollar Index is extending last week’s loss below 98.00. It has approached the 20-day moving average near 97.85. It has met the initial retracement (38.2%) of the bounce from November 1, around 97.95. The next retracement (50%) is closer to 97.75.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Brexit,Currency Movement,EUR/CHF,FX Daily,Hong Kong,newsletter,Singapore,USD/CHF