Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

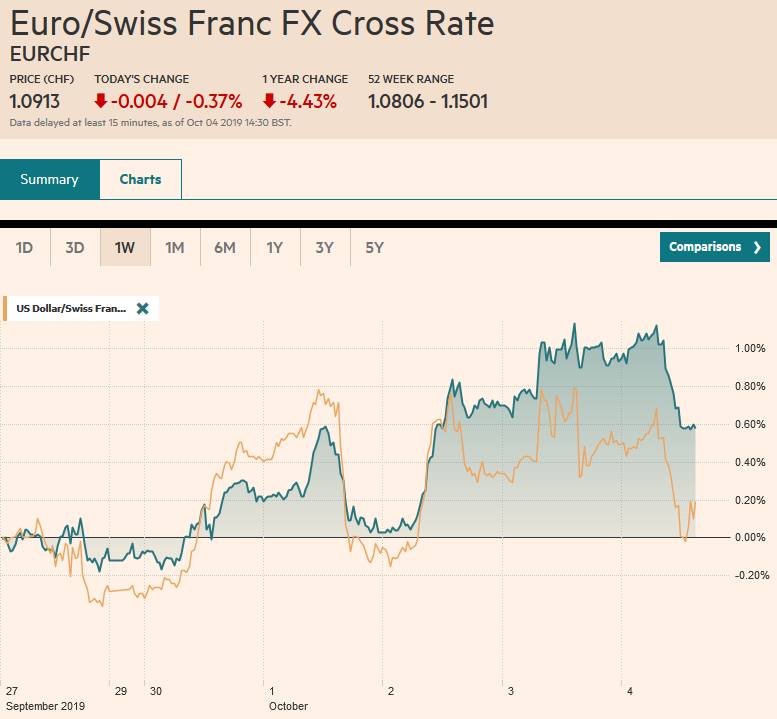

Swiss FrancThe Euro has fallen by 0.37% to 1.0913 |

EUR/CHF and USD/CHF, October 4(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

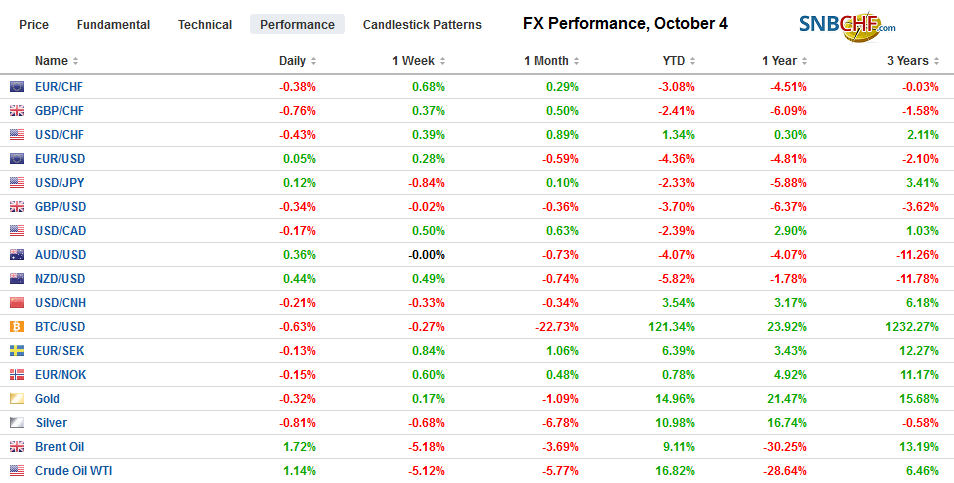

FX RatesOverview: The recovery of US shares yesterday signaled today’s fragile stability. Gains in Japan, Australia, and Taiwan blunted the losses elsewhere in the region, including a 1% slide in Hong Kong. The MSCI Asia Pacific Index fell for the third week. China’s markets have been closed since Monday and will re-open Monday and may play some catch-up. Europe’s Dow Jones Stoxx 600 is extending yesterday’s recovery. Although the week’s losses have been pared, the 3.3% drop would still be among the largest of the year. US shares are trading softer in Europe, unable to extend yesterday’s 2% recovery of the S&P 500 from intrasession lows ahead of the jobs report, where much of the recent data (PMI/ISM and ADP) point to downside risks. Benchmark 10-year bond yields are mostly a little lower. The US benchmark yield is off 14 bp this week while European yields are a couple basis points lower. Swedish yields are off seven basis points on the back of large data misses. The 10-year JGB is practically flat. The US dollar is heavy against the major currencies with the Antipodeans faring best (~0.2%-0.4%). For the week, the yen’s 1% gain leads the way, followed by a 0.5% gain for the New Zealand dollar. The euro and sterling are set to snap a two-week slide. Most emerging market currencies are higher today, led by the South Korean won. On the other hand, the Turkish lira, South African rand, and the Indian rupee are nursing small losses. Meanwhile, gold is trading higher for the fourth consecutive session, but the week’s gain is modest 0.8% (~$1508.5). November WTI is looking to snap an eight-day slide, but it is still off nearly 5.6% for the week (~$52.80), which is the biggest loss since mid-July. |

FX Performance, October 4 - Click to enlarge |

Asia Pacific

As tipped yesterday, Hong Kong cited claimed its emergency powers to ban masks for protesters, though stopped short of declaring an emergency. Chief Executive Lam indicated officials are willing not to extend their response unless the violence escalates. Officials also denied intentions to impose capital controls. This weekend will test the resolve of both sides. Hong Kong’s actions seem designed, at least in part, to appeal to the moderate and business community, which, for example, was not particularly supportive of the Umbrella Movement a few years ago. It also reinforces for us that Beijing recognizes that it is best if local authorities address the local situation.

The Reserve Bank of India delivered the widely expected 25 bp rate cut to bring the repo rate to 5.15%. It is the fifth consecutive rate cut this year, and the series of moves that chopped 135 bp off the repo rate since February. The poor PMI data offered a context but not cause for the cuts. The services PMI fell to 48.7 from 52.4, and the composite reading dropped to 49.8 from 52.6. It is the first overall contraction since February 2018. The central bank cut growth and inflation forecasts and appears to anticipate around 125 bp in rate cuts over the next year.

In the past three sessions, the US dollar has fallen from about JPY108.50 to JPY106.50, the lowest level in a month. The main driver is the drop in global yields and equities this week. So far, today is the first session since September 4 that the greenback has not traded above JPY107.00. There is a nearly $500 mln option struck there that expires today and another for about $535 mln at JPY106.50 that also rolls off. A weekly close below JPY107.00 would add to the bearish technical condition. The Australian dollar is extending its recovery off the 10-year low set in the middle of the week, around $0.6670. It has risen above previous support near $0.6740. The week’s high was close to $0.6775, and that is the next target. However, re-establishing a foothold above $0.6800 would help solidify the base. Chinese markets re-open Monday. The offshore yuan (CNH) has risen by about 0.25% since the mainland markets closed on September 30.

Europe

Outside of the US-Ukraine story, Brexit is the main talking point. The general pattern seen in the past three years remains intact. The closer that the UK Parliament might get to agreeing how to proceed, the further away the UK moves from the EU. Johnson’s plan seems to have won support from the Tory backbenchers, including some who do not share the hardline, the Democrat Unionist Party from Northern Ireland, and some Brexit-leaning Labour MPs. It is not clear if this amounts to a majority. However, what is clear is that from top EU officials is that it is too little too late. The Chair of the foreign affairs committee of the German parliament said Johnson’s proposals cannot be negotiated by the end of the month. EU President Tusk said he was “unconvinced” by the UK proposals and EC. President Juncker said it was “problematic.” The European Parliament expressed “grave concerns.”

Johnson’s proposal seems to violate the basis of the Good Friday Agreement, and the EU cannot accept that Northern Ireland can veto the plan every four years. Although the Prime Minister called his offer his last, he does appear to have a fallback position, which apparently is a time limit on the backstop. Europe has consistently argued that a time limit on the backstop defeats the purpose and removes incentives to reach an agreement. Even though officials on both sides of the Channel have given themselves a week to work things out, the negotiations are bound to continue into the EU summit October 17-18. We continue to believe that a three-month extension is still the most likely scenario while recognizing that a no-deal exit is the default unless positive action is taken.

The euro is posting modest gains for the fourth consecutive session today. During this run, it has risen from a 2.5 year low near $1.0880 to $1.10. It is consolidating inside yesterday’s ranges today and appears to be building a near-term base around $1.0960-$1.0965. The $1.10 level was tested yesterday and held fast. There is an option for about 645 mln euros that is struck there and expires today. The 20-day moving average is also found near there. The response to the US jobs report will determine how the single currency finishes the week, in which the poor US data overshadowed the disappointing EMU PMI. Sterling is trading roughly in a third of a cent range today and remains little changed. It has moved higher in the past three sessions as many see the prospects of an extension or delay as having risen. It seems to have found a base near $1.2325.

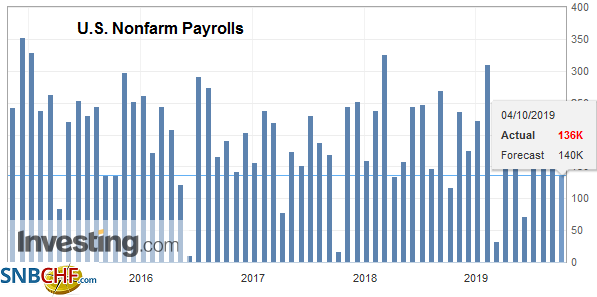

AmericaUS job growth has slowed. Through August, the US created a net of about 158k jobs a month. In the first eight months of 2018, the US grew 234k jobs a month. In Q2, non-farm payrolls rose by an average of 152k. |

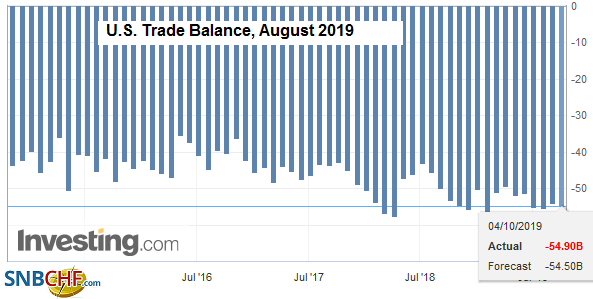

U.S. Trade Balance, August 2019(see more posts on U.S. Trade Balance, ) Source: investing.com - Click to enlarge |

| If the US economy grew less than 167k jobs in September, the three-month average would decline in Q3. |

U.S. Nonfarm Payrolls, September 2019(see more posts on U.S. Nonfarm Payrolls, ) Source: investing.com - Click to enlarge |

| After ISM/PMI and ADP reports, expectations for today’s report softened further, and it might take less than a 125k to disappoint the market.

Given some recent disappointing data, after the US data surprise models reached among the best levels of the year, the focus may be on job creation more than wage growth. |

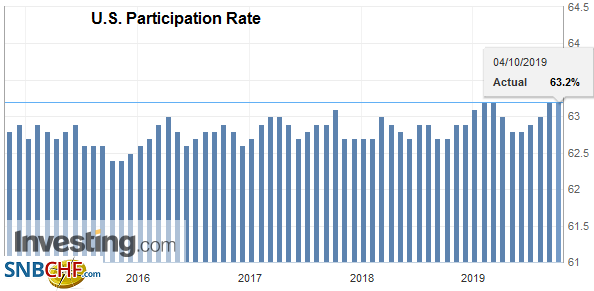

U.S. Participation Rate, September 2019(see more posts on U.S. Participation Rate, ) Source: investing.com - Click to enlarge |

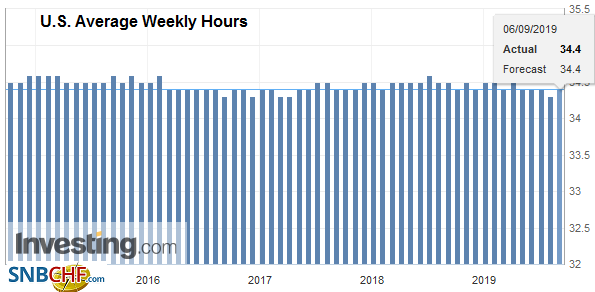

| A 0.3% rise in average hourly earnings would keep the year-over-year pace at 3.2%, which is what it has averaged so far this year. |

U.S. Average Weekly Hours, September 2019(see more posts on U.S. Average Weekly Hours, ) Source: investing.com - Click to enlarge |

| The average was 2.9% in the first eight months of 2018. If the increase in average hourly earnings is supposed to be the faint heartbeat of the Phillips curve, the patient still appears comatose. |

. |

| There has been an important development this week and one that has gone largely unobserved. Looking at two-year interest rates, the US is not the highest yields anymore. |

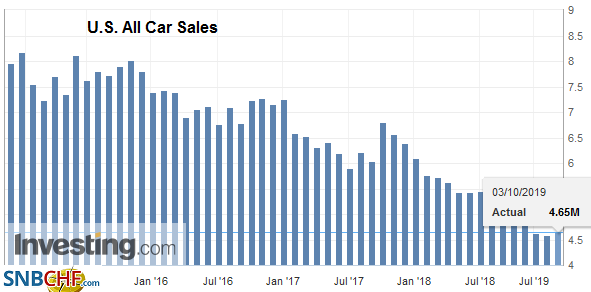

U.S. All Car Sales, September 2019 Source: investing.com - Click to enlarge |

| That role has been assumed by Canada. Its two-year rate pushed fractionally above its US counterpart and extended the move yesterday. The US two-year yield has tumbled about 24 bp this week, while the Canadian two-year yield is off about 16 bp. |

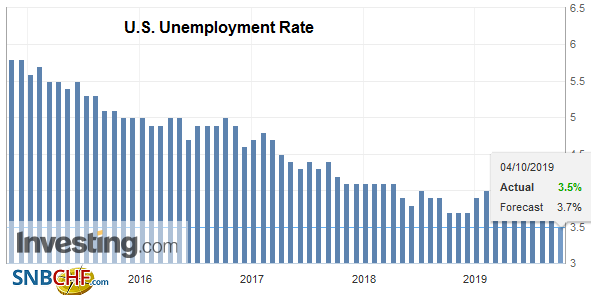

U.S. Unemployment Rate, September 2019 Source: investing.com - Click to enlarge |

On the surface, it looks this has not benefited the Canadian dollar, which in the foreign exchange market, lost about 0.5% against the US dollar this week, making it poorest performing major currency. However, it highlights the fact that the major currencies are not simply a reflection of rate differentials. There are other influences on the Canadian dollar. We typically emphasize two others: the general risk appetite and oil prices. We note that oil prices fell nearly 6.5% last week, its biggest decline in a couple of months, and brought the two-week drop to 10%. The S&P 500, a proxy for risk, fell for the third consecutive week and is lower in seven of the past ten weeks.

The US dollar broke above CAD1.33 and the 200-day moving average in the middle of the week and has not looked back. It reached almost CAD1.3350 yesterday and is consolidating its gains ahead of the US jobs report. Canada reports August trade and September IVEY survey. The data are overshadowed by the US jobs report. Note that Fed Chair Powell delivers opening remarks at a “Fed listens” event around 2PM ET. The US dollar’s five-day advance against the Mexican peso ended in the middle of the week, and now it is off for the third consecutive session. It finished last week near MXN19.69 and is trading close to MXN19.55 currently, near the 20-day moving average (~MXN19.5450). Initial support is seen in the MXM19.50-MXN19.52 area. The Dollar Index reversed lower on Turnaround Tuesday after setting reaching its best level since Q2 17. The 20-day moving average (~98.65) was frayed on an intraday basis yesterday, but that area may offer initial support. A close below 98.35 would be a particularly bearish technical development

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,Canada,Currency Movement,EUR/CHF,FX Daily,jobs,newsletter,U.S. Average Hourly Earnings,U.S. Average Weekly Hours,U.S. Nonfarm Payrolls,U.S. Participation Rate,U.S. Trade Balance,U.S. Unemployment Rate,USD/CHF