Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Many high-income countries experienced little growth but strong price pressures in the 1970s. Since the mainstream economics said the two were mutually exclusive, a new term had to be created, hence stagflation. Fast forward almost half a century later, and mainstream economists are still having a problem deciphering the linkages between prices and economic activity, such as inflation and employment. Theory needs to accommodate the new facts.

Theory is being challenged in another profound way now. Germany, the world’s fourth-largest economy appears to be contracting and experiencing disinflation pressures despite its entire yield curve being below zero. Negative rates have not spurred inflation. It has not bolstered investment. The lower price of money (interest rates) has not spurred demand for it. This is true throughout Europe. Negative rates do not preclude recessions. Nor are they necessarily inflationary as theory might suggest. US and UK inflation is running higher than in the eurozone and Japan, even though the latter have negative interest rates.

Germany, unlike Japan, abhors debt and has, until recently, not been keen to jettison the “black zero” of austerity. Given the debt servicing costs, many officials still seem to think that they can have their cake and eat it too. Spending can be boosted, and taxes cut without taking on greater debt costs. For its part, Japan, which barely grows in the best of times and barely managed to get core CPI (excludes fresh food) to 1% in recent years to say nothing of the 2% target, just raised the tax on consumption.

At last month’s initial tranche of targeted long-term refinancing operations, the ECB practically could not give money away. There may have been some technical considerations deterring interest, and stronger demand is expected at the next tranche in December. Still, the point remains unmarred that the experiment with negative nominal rates has not generated the kind of economic outcomes that were expected.

While nominal rates are not negative in the US, depending on how it is calculated, real interest rates are near or below zero. The 10-year yield is near 1.53%, and the 2-year yield is about 1.4%. The US reports September CPI figures on October 10. The headline rate is expected to rise to almost 2%, and the core rate stable around 2.4%. There are a couple market-based measures of inflation expectations. The 10 through 30-year breakevens (the difference between the conventional and inflation-linked yields) are 1.50%-1.60%, and the five-year five-year forward (the expected rate of inflation for five years beginning five years from now) is at 1.90%.

Low and negative interest rates are spurring neither growth nor inflation. With little real or nominal growth, distributional issues come back to the fore. There are national variations on this theme, but it seems to be a common source of the current political populism. Low real and nominal rates are a function of large economic forces, including weaker population growth, slower productivity growth, past technological advances, and a competitive environment for goods production.

Social organization is important. Capital launched an offensive in the face of falling profits and stagflation in the 1970s. The governments of the UK and the US purposely weakened unions, the one institution whose raison d’etre was to boost labor’s share of the social product. Capital increased its dominance and took an increasingly bigger share. It was too successful. It has so much money, it does not know what to do, so it gives it back to shareholders in the form of buybacks and/or dividends. One CEO of a large internet company claimed to have so much money that he would need to go into space to spend it. Really? And seriously boosting the compensation of the median employee and/or accepting smaller margins is ideologically unthinkable?

There is a great disparity among companies, but business as a whole in the US is sitting with large savings. This does not mean corporations do not borrow money. Of course, they do, but they do this on the whole, as part of “tax minimization” strategies and other financial considerations. Corporate America is a net creditor. They are a source of capital, not net borrowers. Lenin had it wrong when he said that “the capitalists will sell us the rope with which we hang them.” They apparently are hanging themselves. The biggest threat to capitalism and the ability of the social classes to reproduce those relations is the success of capitalists themselves. They have garnered such a surplus that it drives below zero the return on coupon-clipping (passive “risk-free” investment). What Keynes called the “euthanasia of the rentier class,” which we seem to be experiencing now, was not at the hands of communists but results of the dynamic of capitalism itself.

The Federal Reserve’s minutes from the September meeting that saw three regional presidents dissent from the decision to cut rates 25 bp will be released. Two did not think a cut was warranted, and one thought a quarter-point move was too small. The record from the ECB’s recent meeting that saw several officials speak out against the decision and many link the resignation of Germany’s Lautenschlaeger to the disagreement, though no reason has been given, will be reported. The objections to the ECB’s actions spurred several former officials from Germany, the Netherlands, Austria, and France to write a “memorandum” outlining their criticism.

The Federal Reserve may not be as divided as the three dissents, and the dot plot suggests. First, there have not been dissents from any of the Governors, and Vice-Chairman Clarida’s emphasis on reaching the 2% inflation target implies that the Board favors a cut. That is five votes, but the NY Fed President (Williams) has a permanent vote at the FOMC and will vote with the Governors. Bullard, who is the leading dove, might be persuaded to support a 25 bp cut and close ranks. That leaves the standpat Rosengren and George, who objected to both the July and September cuts.

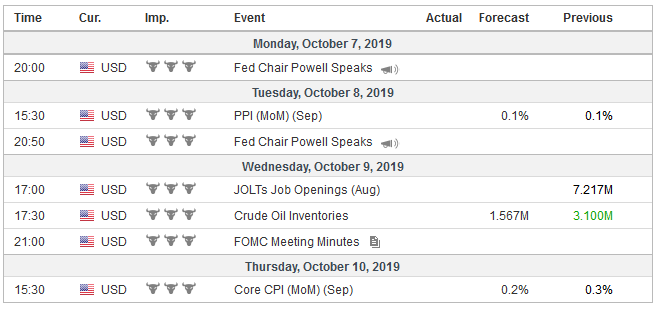

United StatesThe weakness in the PMI/ISM reports and the fall in US equities spurred speculation of not one but possibly two Fed rate cuts this year; one at the end of this month and one at the last meeting in mid-December. The two-year note yield fell more than 20 bp last week. The yield of the January 2020 fed funds futures contract fell by 12 bp last week to 1.455%. The current average effective rate is around 1.83%-1.85%. The US employment data, however, does not show an economy falling off the cliff as some of the survey data seemed to imply. Job growth slowed, but it was still sufficient to see the unemployment rate fall to 3.5%, its lowest level since the end of 1969, and that was with a steady participation rate (63.2%). The underemployment rate also fell to a new cyclical low (6.9% vs. 7.2%). Back-month revisions are understood by some economists as an indication of the underlying trend, and the 45k upward revisions help offset the somewhat lower than expected non-farm payroll gain in September. The main disappointment, however, was with the flat average hourly earnings, which saw the year-over-year increase slip to 2.9% from 3.2%. It is the lowest since last July. The UAW strike at GM might have impacted earnings even if the jobs survey was conducted before the strike began in a statistical quirk. Next month’s non-farm payroll report will pick-up the strike at GM provided if it lasts through the end of next week, which at this juncture looks likely. Based on this week’s developments, we see no reason to alter our base case that the Fed stands pat at the FOMC meeting at the end of this month. We expect the Fed to focus on the plumbing and favor a permanent repo facility as the most likely way to boost repo liquidity rather than increasing reserves (organically or through QE) and hoping that the banks will repo the excess reserves. The Federal Reserve is likely to reserve QE for the conduct of monetary policy. It needs to help investors keep separate the plumbing issues (maturity transformations) from the decision about the price and quantity of money. After standing pat in October, we look for a cut at the December 11 meeting for largely the same reasons as the first two cuts in H2 19: below target inflation presents a low-cost opportunity to help extend the expansion. |

Economic Events: United States, Week October 7 - Click to enlarge |

Eurozone

The ECB is not nearly as fragmented as it sounds either, but the fissure there may be more profound. Many of the differences between the Fed and ECB seem superficial, but one important distinction is in the structure. When fully staff, the Board of Governors at the Fed have a majority of votes at the FOMC. There are two vacant seats presently. There are more regional presidents, but four rotate and the NY Fed president, as we noted before has a permanent vote. The Federal Reserve was designed to give the Governors control. The ECB has a relatively small board, and a larger number of the regional presidents vote even though a rotating system has been introduced.

Of the seven former officials that signed or endorsed the memo cited above, only two came from the ECB’s executive board, the other five were from national central banks. The two former Board members and one former president of a central bank, which means three of the seven, came from Germany. Lautsenshlaeger, who recently resigned, was not one of the endorsers.

The main divide is between creditors and debtors. Germany, the Netherlands, Austria objected to asset purchases from the get-go. Estonia also objected though none of its officials were included in the memo. France’s official objection last month seemed to stem from the timing, unlike the others who opposed on principle. Like the distribution problem discussed above, the tension between creditor and debtor interests can be ameliorated by stronger growth, and some would argue, more federalism (e.g., Draghi endorsing a fiscal union). The new ECB president may seek procedural solutions to the division, such as developing the ECB record to allow individual arguments to be expressed and identified, which Draghi resisted. However, the underlying challenge is that the creditors are a minority in Europe.

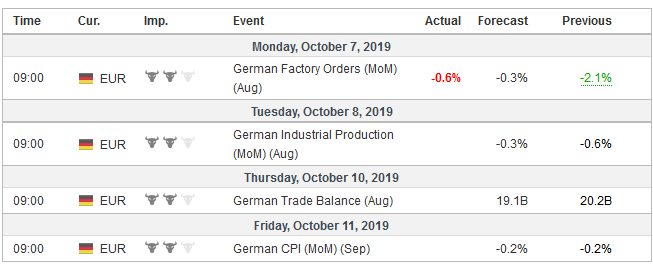

GermanyOn substantive grounds, the survey and real sector data continue to weaken while the lending data and money supply growth are firm. Germany’s August factory orders and industrial production reports are the highlights in the week ahead. Factory orders plunged 2.7% in July, which offset in full the rise in June. Orders are expected to have fallen around 0.4% in August. The average monthly decline through July has been 1.0% compared with a 0.9% average decline in the same 2018 period. The year-over-year contraction is expected to deepen from the -5.6% in July to closer -6.7% in August. The worst so far was recorded in May with an 8.5% year-over-year decline. Industrial output is weakening. It has fallen in three of the four months through July. The average monthly decline this year has been 0.5% compared with a 0.2% decline in the first seven months of 2018. The year-over-year contraction reached a 10-year extreme of -4.7% in June. It stood at -4.2% in July and is expected to have remained there in August. There seems little doubt that the German economy more broadly is contracting and that deflationary winds are strengthening, and that was before the escalation of trade tensions with the US. The US tariffs in response to the WTO ruling will be implemented in a couple of weeks. President Trump must make a decision about tariffs on autos by the middle of next month. These risks, coupled with Brexit, remain potent. UK Prime Minister Johnson continues to publicly reject Parliament’s instructions to seek a delay if an agreement is not struck soon. In court, the government has indicated it intends to adhere to its legal orders. A three-month delay seems the most likely scenario, during which time the UK will hold a national election. Survey results warn of what the British like to call a hung parliament, which in most other countries is understood as a coalition government. |

Economic Events: Germany, Week October 7 - Click to enlarge |

China

China returns from its national holiday that began on October 1. Since it left, the dollar has fallen by about 0.4% against the offshore yuan (CNH). The JP Morgan Emerging Markets Currency Index has risen a little more than 1% over the last three sessions. The dollar also eased against many of the major currencies, including the euro, yen, and sterling. The risk of a non-linear move by the yuan seems minimal. Nor are Chinese shares particularly vulnerable even though the MSCI Asia Pacific Index lost almost 1% last week. Global equities traded better at the end of last week, and the MSCI Emerging Markets equity index rose in the previous two sessions to trim the weekly loss to less than 0.5%. The S&P 500 snapped back from early weakness and gained 2.2% combined on Thursday and Friday.

China will report some financial data, including reserves and lending figures. Caixin’s services and composite PMI will be reported. The data won’t change the general impression that the world’s second-largest economy continues to slow. Most of this seems to reflect China’s own internal dynamics, but part of it is likely traceable to the disruption of US tariffs, the adjustments being made, and the uncertainty of the situation. China’s trade delegation comes to the US next week to hold face-to-face talks with the administration. One metric for the negotiations is whether the US refrains from implementing the duties that were already delayed from October 1 to October 15.

We reject assertions that paint China’s purchases of US soy and wheat and pork and beef ahead of the talks as goodwill gestures. There is a shortage of goodwill and a surplus of national interest. These actions are driven by China’s needs. The fact that they may placate the mercurial American president is an added benefit. The market has responded to heightened trade tensions as a deflationary force and weighs on equities and yields, and often the dollar appears to trade heavier. President Trump’s public request that China investigate the Bidens is likely to reinforce Beijing’s cautiousness in dealing with Washington and, like when Trump recently claimed Chinese officials called and wanted to resume trade talks, it seems provocative at this level of politics. Imagine what we would think about a foreign leader who did that to us. The US also revealed that a trade agreement, if even struck, would not prevent it from confronting China elsewhere, like on portfolio flows, arming Taiwan, and the South China Sea. We suspect that the Trump Administration wants a trade deal now more than China.

Full story here Are you the author?

Tags: China,ECB,federal-reserve,Germany,negative rates,newsletter,Surplus Capital