Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

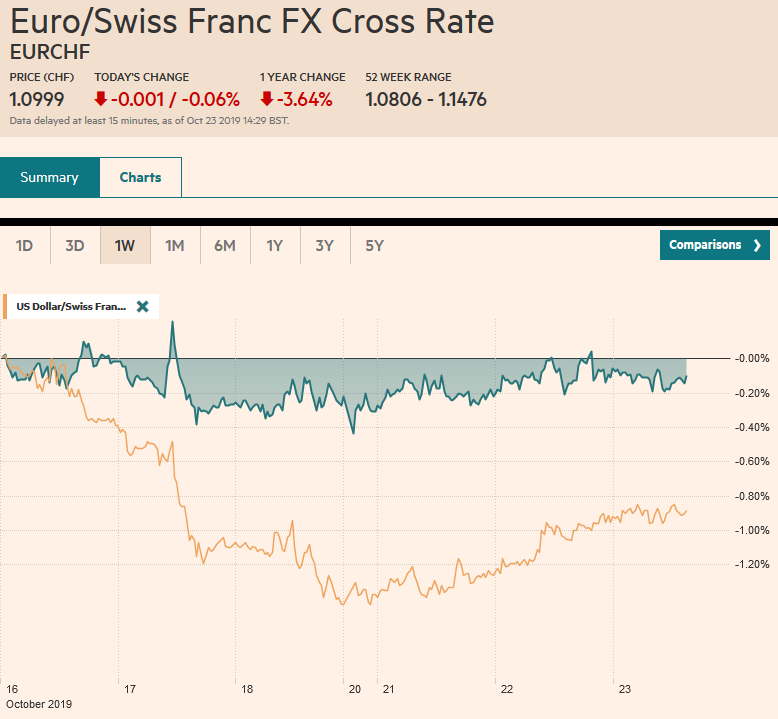

Swiss FrancThe Euro has fallen by 0.06% to 1.0999 |

EUR/CHF and USD/CHF, October 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

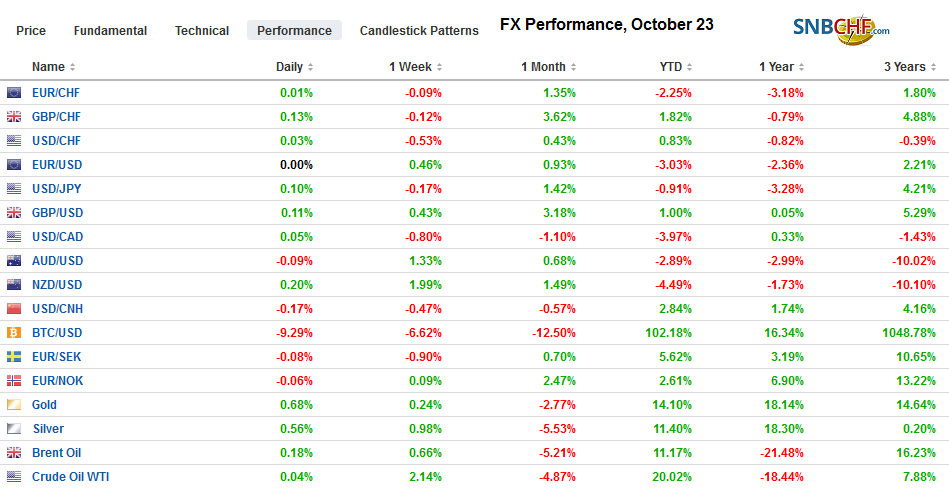

FX RatesOverview: UK Prime Minister Johnson is neither dead in a ditch as he said he would prefer to be than request an extension of Brexit, nor will the UK leave the EU at the end of the month. Yesterday’s vote rejected the attempt to fast-track the legislation needed to support the divorce agreement. It all but ensures that such a delay will be forthcoming. The question now is whether a new timetable will be agreed up or whether efforts will be made to hold an election. Meanwhile, the capital markets are mostly little changed as investors lack near-term conviction. Asia Pacific equities were narrowly mixed, and the MSCI benchmark was weighed down by losses in China, Hong Kong, Taiwan, and South Korea. Note that Taiwan’s benchmark hit a nearly 20-year high yesterday, before pulling back today. Japanese, Indian, and Australian markets edged higher. Bourses in Europe were slightly lower, and US shares were also trading a bit heavier. Benchmark 10-year bond yields are 2-4 bp lower, though the Antipodean bond yields shed 5-6 bp. The foreign exchange market is calm, with most of the major currencies not much more than +/- 0.15% and emerging market currencies in a slightly wider range. Gold remains in a narrow range below $1500, and December WTI is inside yesterday’s range, straddling $54 a barrel. |

FX Performance, October 23 - Click to enlarge |

Asia Pacific

The Financial Times reports that plans are emerging whereby Lam, Hong Kong’s Chief Executive, steps down, which apparently she has wanted to do for some time. The report suggests that if she is allowed to resign, it might not take place until March. Her term extends to 2022. It is unclear what a resignation then would achieve. The demonstrators have sought her resignation, but waiting four-five months will likely have little bearing on the protests. It is not even clear that if the transition were to happen sooner, it would provide closure and end the demonstrations. The press report (citing “people said”) identified two potential candidates, a former head of the Hong Kong Monetary Authority, and a former finance and chief secretary.

The US-China trade conflict has been eclipsed by other developments, but the challenge remains. Both sides are claiming progress, though we continue to note that no date has been set for the resumption of face-to-face talks that are supposed to lead to a signed deal on the sidelines of next month’s APEC meeting. China announced it granted its third round of waivers of the retaliatory tariffs to buy as much as 10 mln tons of US soy, which is double the earlier rounds. While many observers see such steps as cooperative, we suspect it shows what could happen without an agreement–opportunistic buying of American soy not to do US farmers any favors but to meet the domestic shortage. That said, US soybeans are at trading near four-month highs, and Chinese importers may wait for prices to soften before placing new orders.

The dollar slipped to a six-day low against the Japanese yen near JPY108.25. The session low has so far been recorded in the Tokyo session, and this may discourage foreign participants from taking the dollar higher if Japanese accounts are sellers. A break of JPY108, which houses the 20-day moving average and the (38.2%) retracement of this month’s rally, is necessary to confirm our suspicions that the market is giving up on the JPY109 area. The Australian dollar is trading at a three-day low as the upside momentum has faded, and corrective pressures have come to the fore. Initial support is pegged near $0;6820 and then $0.6800. A close above $0.6865 would lift the tone. The dollar remains in narrow ranges against the Chinese yuan, and the implied one-month volatility has fallen to levels (~4%) not seen since Beijing allowed the greenback to rise above CNY7.0.

EuropeThe elation that Prime Minister Johnson felt when the House of Commons supported the broad principles of his agreement (322-299) lasted less than 30 minutes. Parliament quickly rebuffed his attempt to push the necessary legislation through without much debate (322-308). This seems to ensure that the October 31 deadline cannot be met. The EU will not consider the request for a three-month extension. EU President Tusk said that the EU would never force a no-deal exit on the UK. However, Johnson has threatened to force snap elections if there was such a delay and withdraw the bill from consideration. It is possible that, given the first vote, that theoretically, the UK would be ready to leave in November, but an election gambit would force a longer extension. That said, some of the Labour MPs that voted in favor of Johnson’s plan in principle (first vote) cautioned that its vote was tactical so that Johnson’s plan can be amended and their support cannot be taken for granted going forward. |

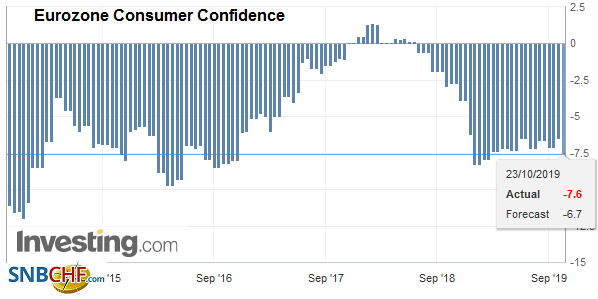

Eurozone Consumer Confidence, October 2019Eurozone Consumer Confidence, October 2019(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

The ECB meets tomorrow. It will be Draghi’s last meeting. Given the package of measures announced last month, it is unreasonable to expect new initiatives. One key issue that remains unresolved, though, is about the self-imposed caps on holdings. Don’t expect Draghi to address the issue, but our understanding is that it is not very pressing now and will not be well into next year. The press conference will likely focus on retrospection and the challenges that Lagarde faces. A few hours before the ECB announcement, the October flash PMI will be reported. A small increase is expected.

As the cessation of Turkish hostilities in Syria was coming to an end, an agreement with Russia was announced to create a buffer zone in northern Syria that includes joint patrols and coordinated action with Syria’s regular forces to push out the remaining Kurdish fighters. Meanwhile, Turkey’s central bank meets tomorrow, and many look for another 100 bp rate cut that will bring the one-week repo rate to 15.5%. Separately, reports suggest that the government may be looking to get another large transfer from the central bank based on unrealized gains in its revaluation account (accrual changes in gold and fx holdings). Currently, tapping the revaluation account is prohibited and requires legislative action to change it. Many observers focus on Turkey’s hard currency debt, but in Q1 20, an estimated TRY75 bln of local debt is coming due.

The euro is near a four-day low around $1.1115 after peaking just shy of $1.1180 on Monday, a two-month high. While the nearly 635 mln euro option struck at $1.1150 that expires today does not seem relevant, the roughly 960 mln option at $1.11 that also expires today may be challenged. We see a band of support extending to $1.1085. Intraday resistance is seen near $1.1130. Sterling has also eased to a four-day low near $1.2840. The low was set in Asia. Nearby support is seen around $1.2820, and a break opens the door to as much as another cent pullback. Cable should be capped in front of $1.29 pending new developments.

America

With the quiet period ahead of next week’s FOMC meeting and a light economic schedule today, before tomorrow’s durable goods orders, flash PMI, and new home sales tomorrow, the market is in need of trading incentives today. The focus may be on corporate earnings. Around 20% of the S&P 500 report this week. Companies that disappoint are being punished, but what is concerning is that even many companies that meet or exceed the guided expectations are lowering the outlook for next year.

| The violent demonstrations have put Chile back on many investors’ radar screens. The government has announced some reforms to help blunt the impact of the higher administered prices and taxes, like a 20% increase in the guaranteed pensions and a boost to the minimum guaranteed income. Late today, the central bank is expected to cut the overnight target rate to 1.75% from 2.0%. The rate has been reduced twice since May, and both moves were 50 bp. Recall that the central bank had hiked rates by 25 bp in January before the easing cycle began. Brail’s Senate is expected to pass the pension reform today after the bill was pulled yesterday to consider the impact of an amendment. The dollar fell 1.1% yesterday against the Brazilian real to reach its lowest level (almost BRL4.06) in three weeks. |

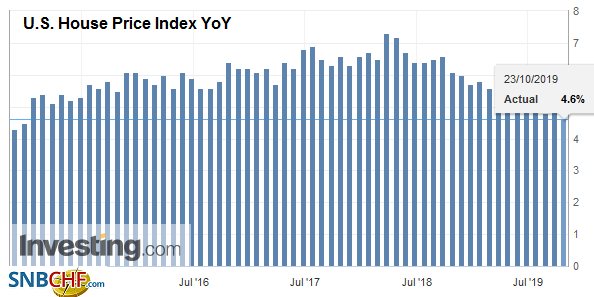

U.S. House Price Index YoY, August 2019(see more posts on U.S. House Price Index, ) Source: investing.com - Click to enlarge |

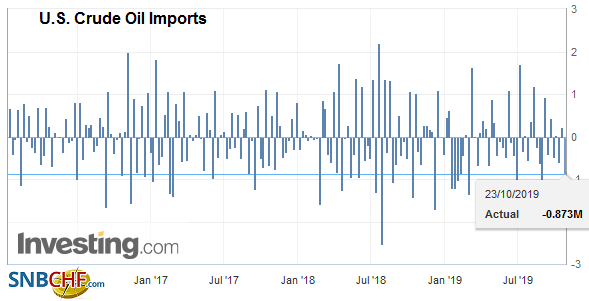

| Reports indicate that API estimated US oil reserves rose 4.45 mln barrels last week. If a build is confirmed by the EIA today, it would be the sixth weekly accumulation and the longest streak since last September-November, when the oil build stretched for 10 weeks. Separately, OPEC is reportedly considering deeper output cuts amid projections of weaker demand. Bloomberg reports that more supertankers are headed for China than seen in the past couple of years. Looking downstream, this may signal that Chinese refiners are set to ramp up output. |

U.S. Crude Oil Imports October 23, 2019(see more posts on U.S. Crude Oil Imports, ) Source: investing.com - Click to enlarge |

The US dollar fell to three-month lows yesterday as the market took in stride the loss of the Liberal majority in Canada’s parliament in Monday’s election. Macro policy is unlikely to be impacted very much. The US dollar is straddling the CAD1.3100 area. We anticipate that near-term greenback low has been approached. Scope for corrective upticks extends into the CAD1.3175-CAD1.3200. The dollar may have formed a bullish hammer candlestick against the Mexican peso yesterday. Recall that greenback had fallen for eight consecutive sessions coming into this week’s activity. It has traded higher Monday and Tuesday and is seeing some mild follow-through gains today. Initial resistance is seen near MXN19.20, but we see near-term potential toward MXN19.26.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,Chile,Currency Movement,EUR/CHF,Eurozone Consumer Confidence,Hong Kong,newsletter,OIL,U.S. Crude Oil Imports,U.S. House Price Index,USD/CHF