Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

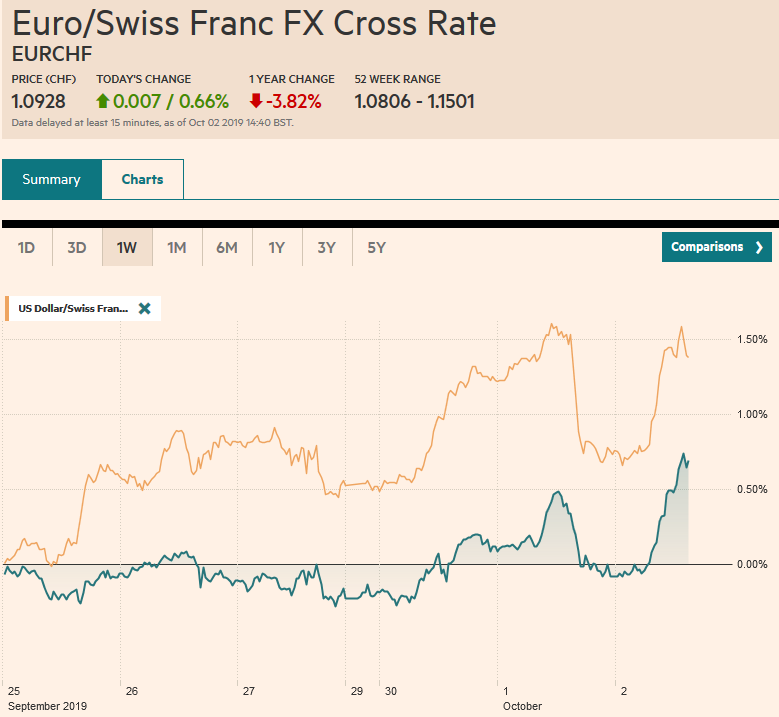

Swiss FrancThe Euro has risen by 0.66% to 1.0928 |

EUR/CHF and USD/CHF, October 2(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Shockingly poor ISM data sent shivers through the market on Tuesday and hand the S&P 500 its biggest loss in five weeks and took the shine off the greenback. The S&P 500 reached a five-day high before reversing course and cast a pall over today’s activity. All the markets were lower in Asia Pacific, with China and India closed for holidays. Europe’s Dow Jones Stoxx 600 reached a two-month high yesterday before selling off sharply, and it has seen follow-through selling today, with the benchmark off around 1.5%. US shares are trading softly, and the S&P 500 is off about 0.7% in electronic trading. The rally in US bonds yesterday lifted Asia Pacific bonds today, but the rally stalled in Europe, where yields are mostly 3-5 bp higher, with the periphery holding in a bit better. The US dollar is showing resiliency after yesterday’s drop and has edged higher against all major currencies, with the possible exception of the Japanese yen. Emerging market currencies are also under modest downside pressures. Gold is holding on to yesterday’s gains but remains below $1485, while WTI is trying to end a six-day slide following news of a larger than expected draw of US inventories, according to the API. |

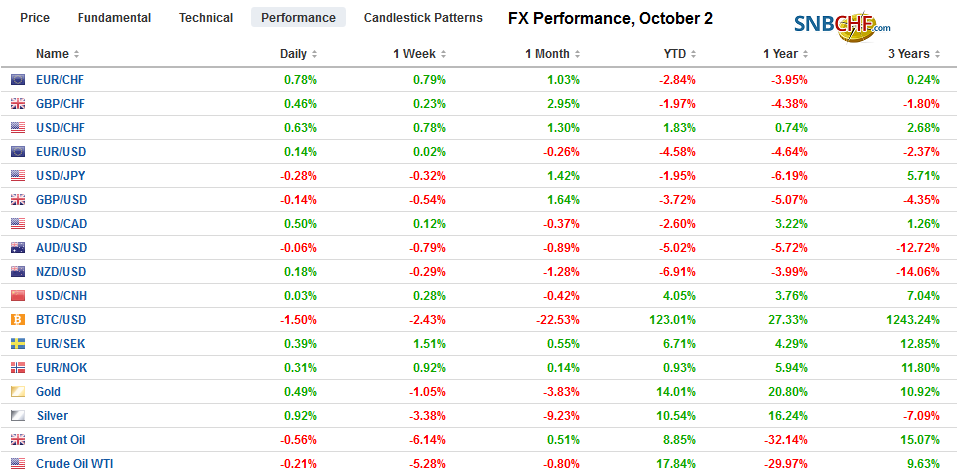

FX Performance, October 2 - Click to enlarge |

Asia Pacific

The conventional wisdom assumes what it must prove when it comes to China and Hong Kong. It holds that Bejing’s most pressing challenge is to quell the protest movement in Hong Kong. Is this true? Outside of some clumsy attempts to intimidate, Beijing appears to have done practically nothing as the demonstrations spill into the fourth month. China wins by letting Hong Kong deal with its own problems. It wins the way that one wins in paper-rock-scissors. One win by not losing. Hong Kong has the tools, including emergency powers that are like martial law. Direct intervention by China would risk HK’s special trade status with the US. It would further alienate Taiwan, which holds national elections early next year. It would create martyrs for further struggles. Separately, but related, HK reported its August retail sales collapsed by a quarter in volume terms and almost as much in value terms (-23%) from a year ago. This was a much deeper contraction than economists expected.

North Korea reportedly tested at least one submarine-launched ballistic missile today. The US State Department requested that North Korea refrain from provocations. Apparently, hours before the test, North Korea agreed to resume talks with the US. The South Korean won is the weakest of emerging market currencies today, losing about 0.55%. The dollar rose 1% last week against the won and is up about 0.85% this week. Poor economic data and prospects for another rate cut in the middle of the month also weigh on the won. The US dollar appears poised to the test the KRW1220 area, the 3.5-year high seen in August.

The dollar posted an outside down day against the Japanese yen (traded on both sides of Monday’s range and closed below Monday’s low). It appears to have made a double top near JPY108.50, but it needs to break JPY107.00 to confirm the pattern, whose measuring objective would be near JPY105.50. Ahead of that, the (61.8%) retracement objective of the rally from late August (~JPY104.45) is near JPY106.00. The follow-through selling today has seen the dollar test the trendline off the August and September lows that is found near JPY107.50 today. There are two sets of expiring options to note. The first set is for about $880 mln and struck between JPY107.50 and JPY107.70. The other set is for a little less (~$820 mln) and is found JPY107.90-JPY108.00. The Australian dollar has not seen follow-through buying after it managed to recover the $0.6800 level in North American dealings after falling to a new 10-year low yesterday (~$0.6670).

Europe

Brexit anxiety is being ratcheted up today. UK Prime Minister Johnson is expected to deliver an ultimatum to the EU today in what he says is the UK’s final offer. The UK Telegraph appears to have leaked it in broads strokes. It calls for scrapping the backstop and placing the hard border between Northern Ireland and the rest of the UK for four years. The Irish foreign minister said that this was unacceptable. The EC has been consistently opposed to a time limit on the backstop as it defeats the purpose. Moreover, Johnson’s proposal seems to undermine the Good Friday Agreement, which facilitated peace on the border. Since the referendum in 2016 and especially in the past several months, Johnson has made the same mistake repeatedly. He has broken the cardinal rule of politics by consistently under-estimating his adversaries, which is arguably why he did not replace Cameron initially. His strategy has been for Labour to capitulate, then Parliament, and now the EC. Assuming that this proposal goes the way of Johnson’s others, the issue may return to UK politics where Parliament has ordered the Prime Minister to request an extension if not deal is reached by mid-month. Johnson has refused.

Merkel tipped her hand. She signaled a formal shift in the fiscal stance by saying the monetary policy should not be overburdened. Bundesbank President Weidmann who has opposed almost every measure that has been implemented under Draghi, including testifying before the European Court of Justice against the ECB itself, has now taken to criticizing Draghi’s leadership style. Weidmann seeming wanted more and longer debates about asset purchases. The Bundesbank has also argued against fiscal stimulus. Merkel seems to be moving in the other direction. With the German economy apparently having contracted for the second consecutive quarter, the government is working on a number of fiscal initiatives, including the 54-bln euro climate change initiative announced recently. Other measures that are being considered include boosting subsidies for electric car purchases, expedite corporate write-offs, and reduce the employer and employee contribution to the unemployment fund. We would have preferred a more ambitious program but recognize the movement in the right direction.

The euro recovered from roughly $1.0880 yesterday to almost $1.0950. There has been no follow-through buying in Asia, and it retreated to nearly $1.09 in very early European activity. Although the intraday technicals are stretched, the euro continues to struggle to sustain even modest upside momentum. It has not risen in two consecutive sessions for nearly three weeks. A close above $1.0950 would begin stabilizing the technical tone. News that the UK’s construction PMI fell for the second consecutive month and has been below the 50 boom/bust level since April has not done sterling any favors, where Brexit concerns already weigh on it. The $1.22-area corresponds to a (61.8%) retracement of the recovery from the sub-$1.20 push seen in late August and a break points to a retest on the lows.

America

There is little positive one can say about yesterday’s ISM report. Perhaps the best that be said is that it was not confirmed by the PMI, which actually ticked up from the flash (51.1 vs. 51.0) and an improvement from the 50.3 reading in August. The details also diverged. The ISM reported a contraction in employment and new orders, while the PMI reckons both rose. US data surprise models were elevated, and the ISM was the anomaly. That does not mean that it is wrong, but it is picking up a sharp deterioration that is not evident in the other data. The ADP estimate of private-sector jobs is the main data point today. It is expected to show employment slowed by 50-55k to 140k. That would bring it more into line with the non-farm payrolls, which rose a disappointing 130k in August and was expected to rise to 140k-150k before this week’s reports.

The S&P 500 posted an outside down day yesterday. In doing so, it filled the gap created by the sharply higher opening on September 5. It also met the (50%) retracement objective of the rally that began in late August. The next retracement target is near 2917. There is another gap from the September 4 higher opening. It is found roughly between 2914.40 and 2921.85. A convincing break warns of a return to the August lows around 2820. Meanwhile, the index is poised to gap lower today, and that means resistance should be seen near yesterday’s lows (~2938.7).

The US dollar nearly transverse its three-week range yesterday of CAD1.32-CAD1.33. The upper end of the range also holds the 200-day moving average. The outside down day saw barely any follow-through selling and instead, the greenback has returned to the middle of the range. The intraday technicals are stretched after its recovery in the European morning. There are around $1.4 bln in options struck between CAD1.3275 and CAD1.3300 that expire today. Since the middle of July, the US dollar has fallen in only two weeks against the Mexican peso (of the past 11 weeks). It is approaching the (61.8%) retracement objective of the dollar’s drop from near MXN20.26 seen in late August. That retracement objective is seen near MXN19.90. Support may be seen near MXN19.75.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,China,Currency Movement,EUR/CHF,federal-reserve,FX Daily,Hong Kong,newsletter,USD/CHF