Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

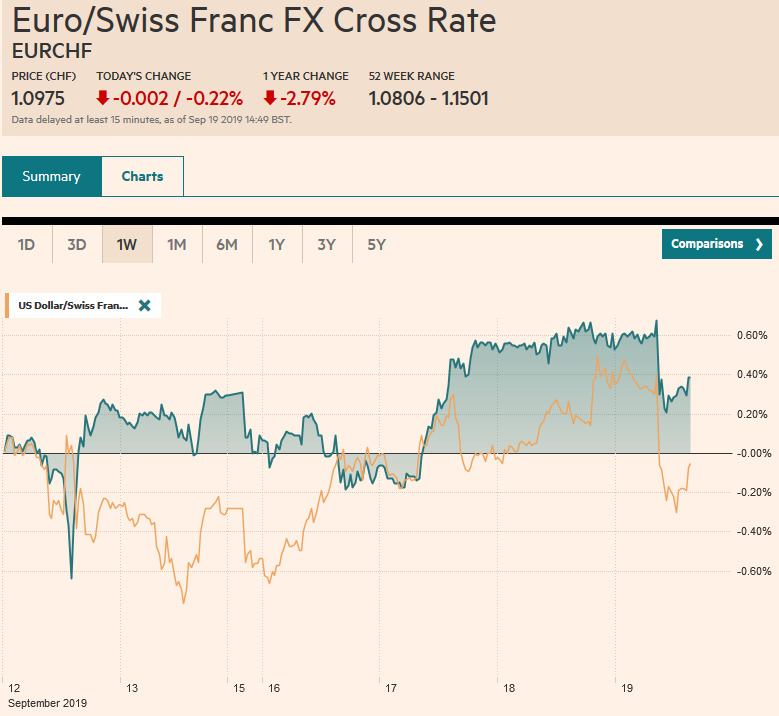

Swiss FrancThe Euro has fallen by 0.22% to 1.0975 |

EUR/CHF and USD/CHF, September 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

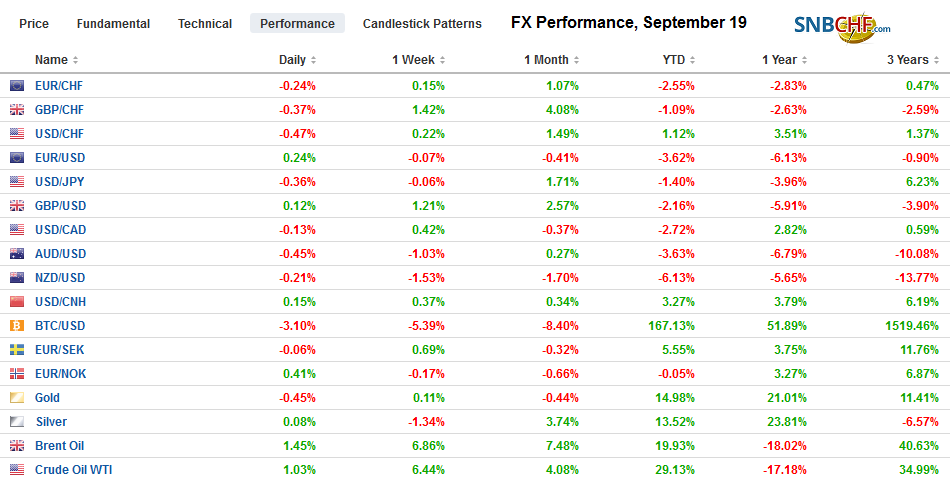

FX RatesOverview: Central bank activity is still very much the flavor of the day, but investors are looking for the next focus. The Bank of Japan and the Swiss National Bank stood pat, while Indonesia cut for the third consecutive time and the Hong Kong Monetary Authority and Saudi Arabia quickly followed the Fed. Brazil cut its Selic rate yesterday by 50 bp as widely expected. Norway’s Norges Bank hiked rates and signaled a near-term pause. Decisions by the Bank of England and the South African Reserve Bank are awaited. Several of the larger market in Asia Pacific, including Japan, China, South Korea, and Australian markets advanced, while Taiwan, India, and most of the small markets eased. Europe’s Dow Jones Stoxx 600 is edging higher after eking out a marginal gain yesterday. US stocks rallied to new session highs after the FOMC rate cut and Powell’s press conference but are trading heavier now. Benchmark bond yields eased in Asia Pacific, but are firmer 1-2 bp firmer in Europe. The rise in US 10-year yields to 1.90% last week continue to unwind and are now a couple of basis points lower on the day near 1.77%. The dollar has not seen much follow-through buying after yesterday’s post-Fed gains and is lower against all the majors but the Australian and New Zealand dollars. The Swiss franc and the Norwegian krone are the strongest, gaining about 0.4% against the dollar in late morning European turnover. Oil prices are firm within yesterday’s ranges. |

FX Performance, September 19 - Click to enlarge |

Asia Pacific

The Bank of Japan left policy on hold but unmistakably left the door ajar to lower rates. It indicated it was re-examining economic and price developments amid increasing downside risks emanating from abroad. It sees these foreign risks as the latest deterrent of stronger price pressures. The sales tax is to be hiked on October 1, and by the next BOJ meeting on October 31, the impact is likely clearer. A lower depo rate may be complemented with a wider range for the 10-year yield under Yield Curve Control.

Australia’s jobs data will keep investors looking for a rate cut. The headline growth of nearly 35k jobs, more than twice the increase forecast, is misleading. Full-time positions fell by 15.5k, meaning that part-time positions rose 50k. The participation rate ticked up to 66.2%, but the new entries did not find work and the unemployment rate rose to 5.3% from 5.2%. The Reserve Bank of Australia meets next on October 1. The market is discounting about an 80% chance of a cut, which would bring the cash rate to 75 bp. In New Zealand, Q2 GDP (0.5% for the quarter and 2.1% year-over-year) was a little better than expected, but still slower sequentially (0.6% and 2.5% respectively in Q1). The RBNZ meets next week few expect a rate cut. However, a move in November that would bring the cash rate to 75 bp is mostly discounted.

More reports are playing up the likelihood of an interim agreement between the US and China. As evident by the recent surge in food prices in China, the world’s second-largest economy is short grains and animal protein. The deal that is rumored is for China to buy more US agriculture products (pork and soy especially) and the US would postpone further tariffs and ease restrictions on Huawei. Recall that the US has delayed the increase of the 25% tariffs to 30% until mid-October from October 1. There is another round of tariffs are due mid-December. These next rounds or tariffs were expected to hit consumer goods, a delay would do more for the US than Chinese households. Such an interim agreement seems more like not harming oneself more rather than material steps that reflect some underling de-escalation. Separately, some market participants were disappointed that the PBOC did not cut its reverse repo rate earlier today, but this keeps the focus on the prime lending rate that will be announced tomorrow. If this rate does not ease, then the disappointment would be reasonable.

The dollar has been turned back from the JPY108.50 area, its best level since August 1. It fell to around JPY107.80 in the Asian session. It popped back above JPY108 in early Europe and met new sellers. There is an $810 mln option struck at JPY108 that expires today. The week’s low is near JPY107.50, where another expiring option is struck (~$550 mln). We suspect the dollar’s high may be in place and that it will work lower in the coming days. The Australian dollar has rolled over after being unable to push much above our $0.6880 target. Our initial downside object is near $0.6765, and a break would re-target $0.6700. There is a roughly A$540 mln option at $0.6800 expiring today that remains in play.

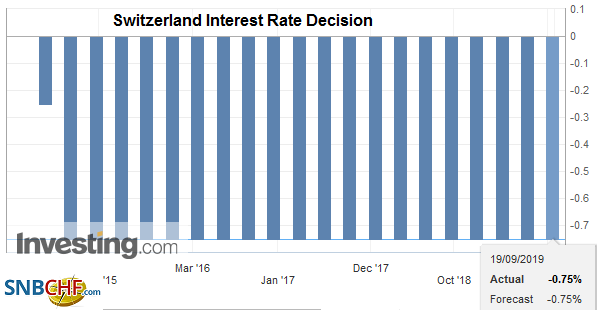

EuropeThe Swiss National Bank left its key rate unchanged at minus 75 bp. However, it cut growth and inflation forecasts and indicated it would change the way it was calculating negative rates on sight deposits. Norway’s Norges Bank continued to march to the beat of a different drummer. It hiked the deposit rate by 25 bp to 1.50% Most, including ourselves, thought that the Norges Bank would have held off. However, it did suggest that while there may be a need for an additional hike, it will likely standpat now into next year. |

Switzerland Interest Rate Decision, September 2019 Source: investing.com - Click to enlarge |

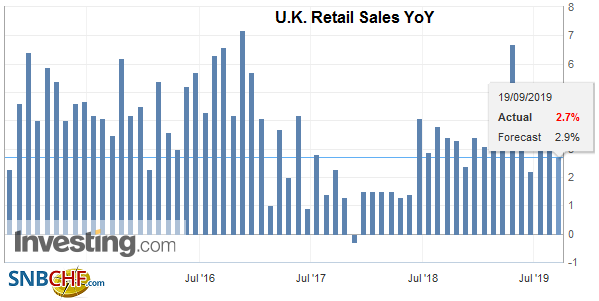

| The Bank of England is the last of the major banks to conclude this week’s policy meetings. There is little doubt that it is on hold. More speculation is on the possible extension of Carney’s term as governor (again) than on today’s rate decision. Separately, the UK reported August retail sales. The 0.3% decline, excluding petrol and -0.2% with it, were in line with expectations. The surprise was that the July series both rose 0.4%, double the initial estimate. |

U.K. Retail Sales YoY, August 2019(see more posts on U.K. Retail Sales, ) Source: investing.com - Click to enlarge |

| The other development in Europe was the take up of the ECB’s new round of Targeted Long-Term Refinancing Operations (TLTRO). Banks in the periphery tend to be the large users of this facility. These long-term loans also expand the ECB’s balance sheet and is a tool that it developed as part of its monetary policy tools. The ECB reported 3.4 bln euro in new loans were taken under the new facility. Reports suggest 28 banks participated, but the participation was considerably less than expected. That said, some suspect that when the new tiering (excluding some deposits at the ECB from negative rates) starts in several weeks, the demand for subsequent tranches will increase. |

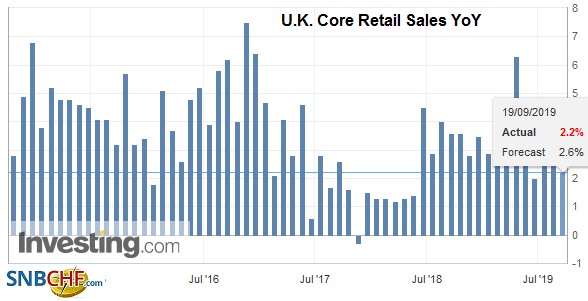

U.K. Core Retail Sales YoY, August 2019(see more posts on U.K. Core Retail Sales, ) Source: investing.com - Click to enlarge |

The euro has recouped a third of a cent that it lost after the FOMC announcement yesterday. However, as it approaches $1.1070-$1.1080 area, the buying enthusiasm is likely to diminish. The ~655 mln euro option at $1.1085 that expires today may be safe, but the 1.2 bln euro option at $1.1050 may be challenged in the North American morning. Sterling is consolidating within yesterday’s range, which was within Tuesday’s range. This pattern is often seen as a consolidation. That said, we continue to note that the $1.2500-$1.2 530 is important from a technical perspective.

America

The Federal Reserve cut the fed funds target range by 25 bp and tweaked the interest it pays on reserves and reverse repos by a little more. When everything is said and done, market expectations of the trajectory of policy did not change much. The January 2020 fed funds futures contract changed by half a basis point and continues to fully discount another 25 bp cut this year. That said, the dot plots are a bit like Goldilocks and the three bears. One camp (7) thinks the porridge is too cold and that another rate cut will be appropriate. Another camp (5) thinks the porridge is too hot and thinks a rate hike is appropriate. The third camp (5) thinks the porridge is just right and policy is fine where it is at. The logic of the Fed’s decision that the subdued price pressures provide for an opportunity to take some relatively cheap insures given the headwinds and risks. Based on the current information set, our bias is for a pause in October and a cut in December.

Separate from monetary policy, the issue of the funding squeeze was also a topic at Powell’s press conference. Many have speculated about the possibility of the US having negative interest rates. Former Fed Chairman Greenspan recently opined that based on demographic considerations, it is simply a matter of time. Powell played down the likelihood of it, preferring asset purchases as the first line of defense when the effective lower bound is reached.

Powell did not offer fresh insight into the cause of the funding squeeze and indicated the Fed was surprised as so many market participants were despite being well aware of the corporate tax date and coupon settlements. Powell indicated the Fed would continue to use overnight repos to ensure sufficient reserves (and the Fed preannounced an operation for today). He also spoke of the possible need to return to the organic growth of the Fed’s balance sheet. Powell was referring to the expansion of the Fed’s balance sheet gradually practically every year until 2007 and the crisis. The organic growth of the Fed’s balance sheet was dictated by the need for reserves as the economy and business expanded. Under quantitative easing, when the Fed buys assets, the expansion of the balance sheet drives the growth of reserves. The former is reactive. The latter proactive. Powell suggested some decisions could be announced at the October meeting. Yesterday’s repo operation as dealer demand for $80 bln for the $75 bln on offer. It should not be surprising if the repo operations continue into next week and possibly until the start of the new month and quarter.

The US reports weekly jobless claims (for the same week that the next non-farm payroll survey is conducted), the leading economic indicator, existing home sales, alongside the Philadelphia Fed survey for September. Mostly softer data is expected (which also means an increase in weekly jobless claims). A surprise could be with the existing home sales. Many observers saw the stronger than expected housing starts and permits reported yesterday as a sign that lower interest rates are helping the housing market. Canada and Mexico’s economic calendars are light today, though Canada reports July retail sales tomorrow.

The US dollar remains firm against the Canadian dollar is bumping against its recent highs and the 200-day moving average a little above CAD1.3300. Support is seen in the CAD1.3270-CAD1.3280. Meanwhile, the greenback continues to hover around MXN19.40. It has extended yesterday’s recovery off the MXN19.3260 low seen yesterday, its lowest level since August 5, to MXN19.45. We suspect the dollar is bottoming against the peso after falling from above MXN20.20 in late August. A move toward MXN19.60 would not be surprising ahead of the September 26 central bank meeting from which a rate cut is likely (~66% chance appears discounted). Brazil’s central bank delivered the widely expected 50 bp cut late yesterday and another cut of the same magnitude is expected before the end of the year. We look for the dollar to firm against the real and a move above BRL4.12 likely targets the recent high of almost BRL4.19.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of England,Brazil,Currency Movement,ECB,EUR/CHF,federal-reserve,FX Daily,newsletter,Norwegian Krone,U.K. Core Retail Sales,U.K. Retail Sales,USD/CHF