Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

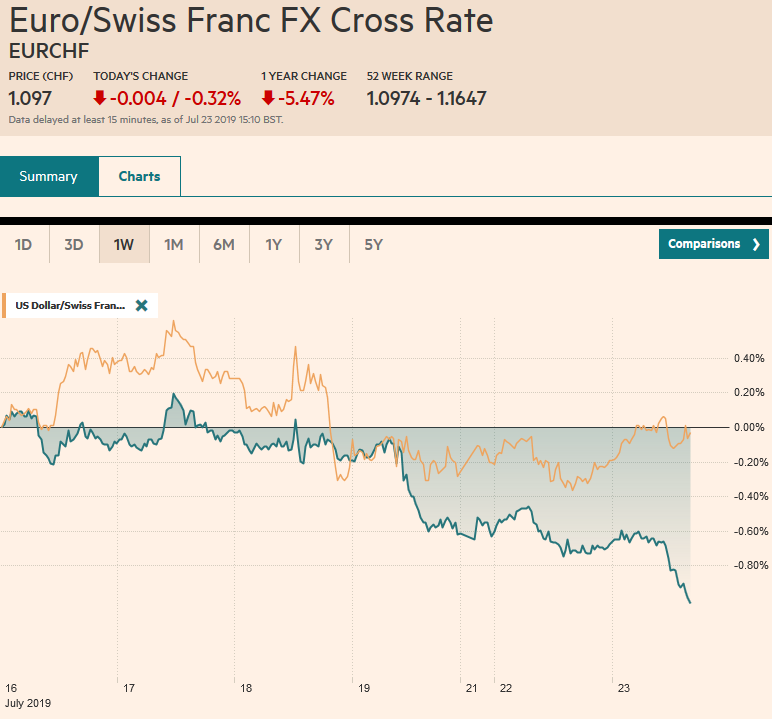

Swiss FrancThe Euro has fallen by 0.32% at 1.097 |

EUR/CHF and USD/CHF, July 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The gains in US equities and the apparent US budget agreement has underpinned equities today and the US dollar. Asia Pacific equities recouped yesterday’s losses, and Europe’s Dow Jones Stoxx is posting gains for the third consecutive session, helped by some earning beats, to probe two-week highs. US shares are firmer. Benchmark 10-year yields are mixed with the Asia Pacific softer and European firmer. Despite elevated political tensions in Italy, Italian bonds are bucking the regional trend with softer yields. The UK will have a new Prime Minister shortly, but the prospects of a no-deal Brexit and dovish comments by a hawk at the BOE has kept sterling on its back foot, while the US dollar enjoys broad gains among the major and emerging market currencies. The Chinese yuan, which has been trading as if it were pegged to the dollar and the Hong Kong dollar, which is formally pegged, are among the best performing emerging market currencies today. |

FX Performance, July 23 - Click to enlarge |

Asia Pacific

South Korea reportedly fired 360 rounds at Russian military planes violated its airspace. Reports suggest that three Russian planes and two Chinese bombers flew over part of South Korea earlier today. It is not clear if this was a coordinated move. Recall that yesterday Venezuela complained that the US violated its airspace. No one appears to be drawing a connection, but a tit-for-tat ploy cannot be ruled out.

The US has sanctioned a Chinese state-owned oil company for knowingly shipping Iranian oil in violation of the embargo. The PRC reportedly has stored Iranian oil in bonded storage on the Chinese mainland. The bonded storage is owned by Iran and does not appear in Chinese customs or import data.

Separately, China is imposing anti-dumping duties on stainless steel imports from Japan, Indonesia, South Korea, and the EU. South Korea, which is seeing new licensing requirements to purchase Japanese semiconductor and flatscreen materials, will be the hardest hit by the Chinese actions. All of its stainless steel manufacturers will face the steepest duties (~103%) except Posco (~23%). Indonesia will face around a 20% duty, and the EU producers penalty is near 43%. Most Japanese suppliers will have a 29% tariff, except Nippon Yankin Kogyo, which was slapped with about an 18% duty.

The US dollar is nearly a big figure higher from the lows in the second half of last week (~JPY107.20) against the yen today. It appears poised to re-establish a foothold above JPY108, where an $800 mln option is set to expire. There is an option that expires tomorrow at the same strike for $4 bln. The next immediate target is the JPY108.30-JPY1080.50 band, but the more significant cap is at JPY109. After approaching $0.7100 (peaked a little above $0.7080 last week), the Australian dollar is easing for the third consecutive session today. However, it found bids below $0.7020 but faces resistance now in the $0.7035-$0.7050 area. We see potential toward $0.6975. After sinking to four-month lows against the New Zealand dollar yesterday, the Aussie is coming back bid today. It has been helped by news that the Reserve Bank of New Zealand, which is expected to cut rates in early August, will reexamine its unconventional options as well.

Europe

The market has long been skeptical of Bank of England’s tough talk on rates, and today a hawk (Saunders) appeared to capitulate. The market favors a rate cut toward the end of the year. If Brexit does take place at the end of October, which Johnson and Hunt say they are committed, a rate cut can be brought forward. The market remains skeptical that Brexit will take place then. Meanwhile, as noted yesterday, the speculation is that under Johnson, Lyons will replace Carney as the Governor of the Bank of England. Jonhson is widely expected to have won the Tory leadership contest, the outcome of which will be announced shortly. Several more cabinet officials are expected to resign today. It seems a bit ironic that after the US announced that the UK has to look after its own ships in the Gulf, the UK sought the EU’s assistance.

The dovish signals from the ECB have helped lift Italian bonds over the past few months. Given the rally, Italian banks shares may have been expected to perform better as the vicious cycle became virtuous. However, the bank share index has recouped only around half of its spring sell-off. Meanwhile, rather than bad loans being the imminent risk, so many commentators have emphasized, it is Italian politics. League leader and Deputy Prime Minister Salvini is trying to exert greater influence in the government or else he seems to be threatening to topple the government and seek early elections. However, the ball is not entirely in his court. Reports suggest he wants the League to have more cabinet posts and may seek to replace Prime Minister Conte. The issues may come to a head in the coming days.

The ECB meets Thursday. Before the weekend, the market seemed nearly evenly divided over a rate cut this week or in September. The pendulum of market sentiment has swung against a formal move this week. The odds of a move now are around one-in-four. It is expected to tweak its forward guidance and formally signal its intent to ease policy. Draghi would likely prepare the market for a multi-step move that would include lower rates, a resumption of assets purchases (40-45 bln euros a month?), and perhaps more generous terms of the TLTRO that has already been announced.

The euro has pushed below $1.12 and through last month’s low near $1.1180. There is mild support around $1.1150, but nothing solid until $1.1100. It requires a move back above $1.1225 to stabilize the technical tone. There is a 2.5 bln euro option at $1.12 that expires tomorrow, which may act as a bit of a cap. Sterling had been testing the $1.2550 area in the second half of last week and is now approaching $1.2400. The two-year low set near $1.2380 last week is the next immediate target and then $1.2350. Implied volatility covering the run-up to the October 31 deadline is rising. The benchmark three-month implied vol is near 9.2% a three-month high today. One-month vol, in contrast, is firm near 6.6% but is well off the 100-day moving average of around 7.9%.

AmericaA two-year budget deal appears to have been struck by Democrat leadership in the House and Treasury Secretary Mnuchin. It will lift the debt ceiling, so it is not an issue until after the 2020 election. Spending caps will be raised, under the plan, by $320 bln, and the automatic cuts next year will be avoided. The spending will be equally divided between defense and the domestic economy. There are around $75 bln in offsets, half as much as the Trump Administration proposed. Reports suggest that Trump is committed to unwinding as much of Obama’s legacy as possible, and ironically, the Budget Control Act of 2011, which Republicans, some of whom are in the administration, foisted upon Obama, is now euthanized after being waived for the past five years. With a couple months left in the fiscal year, the combination of spending increases and lower revenues due to the tax cuts the budget deficit is near $750 bln, a 23% increase from a year ago. |

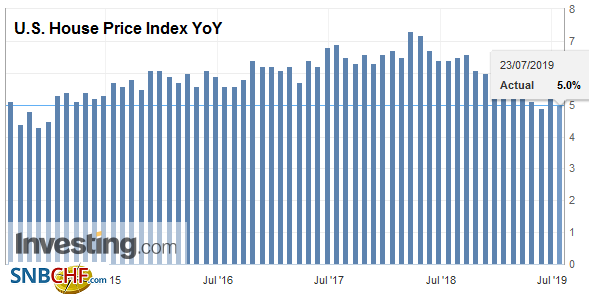

U.S. House Price Index YoY, May 2019(see more posts on U.S. House Price Index, ) Source: investing.com - Click to enlarge |

Canada had its second consecutive disappointing economic report. At the end of last week, Canada unexpectedly reported a decline in May retail sales. Yesterday, it reported an unexpected drop in May’s wholesale trade. The 1.8% decline was the largest in three years and helped lift the US dollar to its best level in two weeks. It closed above CAD1.31, which it has not done since July 9. The five-day moving average is crossing above the 20-day (a proxy of the short term trend) for the first time since early June. We have suggested the US dollar was carving out a low and noted the bullish divergence in some of the technical indicators. Bullish speculators were large buyers of the Canadian dollar in the futures market recently, and this leaves the late longs in weak hands. During the corrective phase, the first important target may be in the CAD1.3175-CAD1.3220 band.

The US dollar is edging higher against the Mexican peso for the third consecutive session. Last week’s highs near MXN19.12 may be tested today, but the MXN19.20 area offs a more solid near-term cap. Mexico’s high real and nominal yields make it a favorite carry play–against the yen, euro and Swiss franc, for example. Tomorrow Mexico reports its biweekly inflation reading. The central bank targets a 2%-4% range and recently price pressures have fallen back into the target range, but just barely. Between the recent surprise resignation of the finance minister and the government’s latest attempt to help PEMEX, investor confidence has been shaken.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CAD,Brexit,Currency Movements,ECB,EUR/CHF,newsletter,U.S. House Price Index,USD/CHF