Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

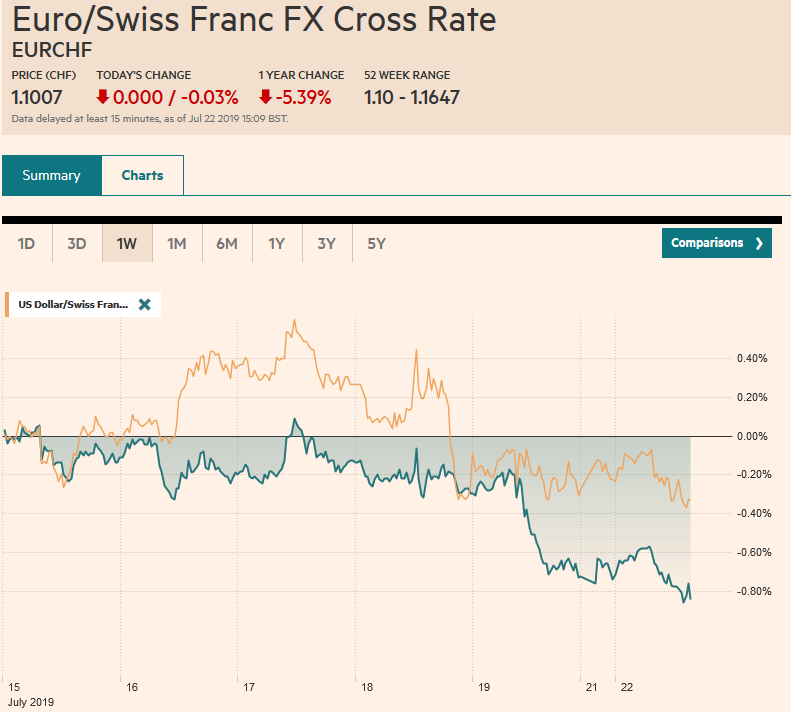

Swiss FrancThe Euro has fallen by 0.03% at 1.1007 |

EUR/CHF and USD/CHF, July 22(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: What promises to be an eventful two weeks has begun quietly. The ECB, Fed, BOJ, and BOE will meet over the next fortnight. The central banks of Turkey and Russia meet this week and are expected to cut rates. The UK will have a new Prime Minister. The UK-Iranian seized each other ships, and the UK seeks a resolution. Japan may remove South Korea from its preferred trading partners. The US House of Representatives is set to go on the summer recess with the debt ceiling looming. Asia Pacific equities trade heavily after the losses in the US before the weekend. Although China’s initial launch of its tech-startup market ended on an up note, the Shanghai and Shenzhen Composites led the regional bourses lower. European stocks are little changed in the early turnover. US shares are also little changed. Benchmark 10-year yields are mostly softer. The dollar is in narrow ranges (+/- 0.15%) against the major currencies. Sterling and the yen are on the weaker side, while the New Zealand and Canadian dollars are a touch firmer. Tensions in the Gulf is unpinning oil prices, while gold has steadied after the pre-weekend retreat. |

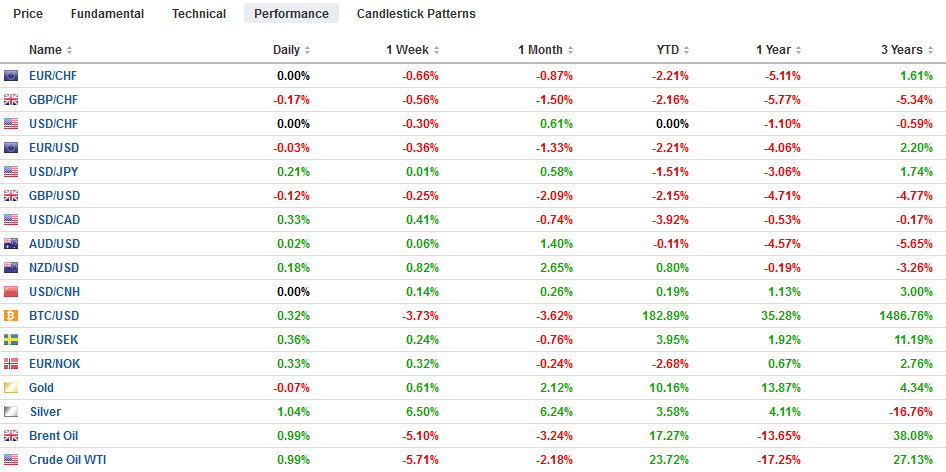

FX Performance, July 22 - Click to enlarge |

Asia Pacific

A low-voter turnout gave the LDP and its allies a solid majority but took away the super-majority (2/3) it enjoyed. This is important because it makes constitutional changes more difficult. Although Abe did not campaign on the issue, he has long sought modifications to Article 9 of Japan’s constitution that limits its military capability. It is not a particularly galvanizing issue. Pensions, taxes, and the economy more broadly, were more salient to voters.

South Korea trade figures for the first 20 days in July warned of continued headwinds. Exports fell by 13.6% year-over-year, after a 10% decline in June. Three different shocks are hitting South Korea. The first is the disruption of trade and the slowing of the Chinese economy, which difficult to separate fully. South Korean exports to China are off 19% and 5.1% to the US. The second is industry-specific challenges in the semiconductor space, which is partly related to the first shock. South Korean semiconductor exports are off 30% year-over-year. The third shock is the dispute with Japan. Exports to Japan were off 6.6%, which related to the first force discussed above, but the 15% decline in imports from Japan may be more about the tensions between the two countries. Japan’s public hearings on removing South Korea from its preferred trade partners list conclude later this week. If removed, a wider range of South Korean industry, including autos, may be disrupted. The won’s 0.33% loss today is among the largest of the emerging markets.

Demonstrations in Hong Kong continued for the sixth week. After being mostly peaceful, they have turned violent recently as it appears an organized group of men have taken to attacking the demonstrators. The resulting mayhem leads to an escalation of police force. The market impact has been minimal. The Hang Seng has rallied in six of the past seven weeks, though the nearly 1.4% loss today was among the largest in the region. After flirting with its lower band in late May, the Hong Kong dollar (HKD7.85), it is now on the firm side (~HKD7.8080).

The US dollar was bid to a three-day high in early Asia (almost JPY108.10) before slipping back to JPY107.80 in the European morning. There is a $400 mln option struck at JPY107.70 that will be cut today and larger options (~$2.9 bln) stacked between JPY107.25 and JPY107.50. While the intraday technicals seem supportive of another push higher, the dollar might not be able to distance itself much from the JPY108 area where an option for $3.4 bln will expire on Wednesday. The Australian dollar reversed ahead of the weekend after pushing briefly through $0.7080. It extended the retreat briefly today toward $0.7030, which is a (61.8%) retracement of the bounce from the middle of last week. A break initially targets $0.7000. The Australian dollar is up about 0.3% against the greenback this month, putting it just behind the Canadian dollar and lagging the New Zealand dollar by about 0.5%. The dollar-bloc currencies are the outperforming so far in July. The Chinese yuan continues to trade in extremely narrow ranges and small net change. Officials seem to be seeking greater stability in the foreign exchange market despite (or because of) tensions in the money markets. The tensions seem to be stemming from the failure of Baoshang Bank in late May, which appears to have reintroduced counterparty risks in the interbank market.

Europe

The ECB meeting is the main economic event in Europe this week. The main issue is whether it merely prepares the market for easier policy in September or whether it acts now. ECB officials have made a case to act sooner rather than later and with a range of tools at their disposal (including rates, asset purchases, and forward guidance. Due, it appears, mainly to procedural issues, and the new staff forecasts that will be available in September, market sentiment leans against action this week. However, the forward guidance of a commitment to keep rates low through the middle of next year could be extended to the end of 2020 and include a phrase that would allow for lower rates.

The prospect of a no-deal Brexit despite the UK Parliament’s attempt to frustrate such a course has encouraged the EC to develop a substantial aid package for Ireland. Meanwhile, Johnson is poised to officially win the Tory leadership challenge and will become the next Prime Minister. Media reports are suggesting he is considering his former adviser Lyons to head the Bank of England when Carney steps down later this year. Several senior ministers, including the Chancellor of the Exchequer Hammond, are expected to resign over the next 48 hours. Separately, the UK is seeking UN assistance to resolve the tensions with Iran.

Spain’s Socialist Party appears to have struck a deal with Podemos, leaving Sanchez in the position of being the first Spanish Prime Minister to lead a coalition government. There has been little in any market impact. Italy’s coalition government was strained, but the scandal over Russian funding for the League paradoxically may strengthen the coalition may restraining League leader and Deputy Prime Minister Salvini.

The euro is stuck in its trough just above $1.1200. It has been capped near $1.1225 today. There is a 2 bln euro option at $1.12 that expires Wednesday. The euro finished last month a little above $1.1370. It has not been above $1.13 since July 3. The low has been a touch below $1.1195. We suspect the risk is for new lows this week. Sterling has been unable to sustain even the most mild of upticks. It was little changed to slightly firmer in Asia before being sold as European markets opened. While there is scope for losses toward $1.2430, the intraday technicals warn that the market is getting stretched. The euro eased for the past three sessions against sterling but is coming back bid today and is back at GBP0.9000.

America

The Boston Fed ‘s Rosengren’s rejection of the arguments for a rate cut is the last Fed comment until after the July 30-31 FOMC meeting. The unusual step the NY Fed took to rein in market expectations of a 50 bp move is also important. Also, St.Loius Fed’s Bullard, the lone dissent last month in favor of an immediate cut, endorsed a 25 bp cut. He talked of it in terms of a “recalibration” rather the beginning of an easing cycle like the market has discounted.

The House of Representatives’ summer recess begins at the end of the week. There is much unfinished business. The new free-trade agreement with Mexico and Canada needs to be approved. PredictIt.org shows wagers see only a 30% chance it will be passed this year. More pressing is the debt ceiling. Trying to impress upon Congress the urgency, Treasury Secretary Mnuchin warned that conservative estimates warn that the debt ceiling could be hit before the House of Representatives returns on September 9. The uncertainty already seems to be impacting the T-bill market. In addition to bills, the US Treasury will raise $130 bln this week in coupon sales (2, 5, and 7-year securities).

The economic calendar for North America is light today. It features the Chicago Fed’s National Activities Index. In the first five months, it has declined consistently, except for March. The June reading today is expected to snap a two-month decline and lend credence to the idea that the US economy found some traction at the end of the quarter, while the NY and Philadelphia Fed surveys suggest the momentum carried into July. The economic highlight of the week is the first look at Q2 US GDP, where the market expects something close to what the Fed sees as the sustainable long-run pace (1.9%) and around a quarter of the S&P 500 report.

The US dollar is in the middle of the CAD1.30-CAD1.31 range that has confined it for nearly two weeks. The technical indicators have not confirmed to greenback’s lows, and this is being expressed as a sideways trend rather than a recovery. The weakness in Canada’s retail sales before the weekend points to the fact that much of the good news for Canada (that the economy recovered from its soft patch and that the Bank of Canada is on hold) is already in the exchange rate. Concerns about the AMLO government and pessimism over its plans for PEMEX have seen the peso lose its previous momentum, while the high yields still protect it. The dollar’s new range appears around MXN18.93 to MXN19.12.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,Currency Movements,ECB,EUR/CHF and USD/CHF,Japan,newsletter,South Korea