Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.21% at 1.1169 |

EUR/CHF and USD/CHF, June 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Risk-taking was bolstered by the dramatic shift in Draghi’s rhetoric less than two weeks after the ECB meeting and a Trump’s tweet announcing that there was going to be an “extended” meeting between him and Xi at the G20 meeting and that the respective staff would begin coordinating. It was later confirmed by the Chinese media. Today’s focus is on the FOMC. Barring a rate cut that would surprise, the focus is the extent to which the statement and Powell manage market expectations. The one-two punch of Draghi and Trump lit a fire to equities in Europe and the US. Asia followed suit, with the MSCI Asia Pacific Index up the most in five months. European equities are consolidating yesterday’s gains, and US shares also are little changed. The same meme is evident in the bond markets, where Asia Pacific played catch-up, while European and US bond yields edge higher after yesterday’s sharp decline. The dollar is little changed against the majors with the Antipodeans trading a little softer. Most emerging market currencies are firmer. The Turkish lira is the notable exception, as both the US and Europe are considering sanctions. The US is contemplating action to express its disapproval of Turkey, a NATO member, for buying a Russian missile system, while Europe disapproves its drilling activity in the Southeast part of the Mediterranean. South Korea and Taiwan currencies led the emerging market currencies with 0.8% and 0.6% gains respectively. |

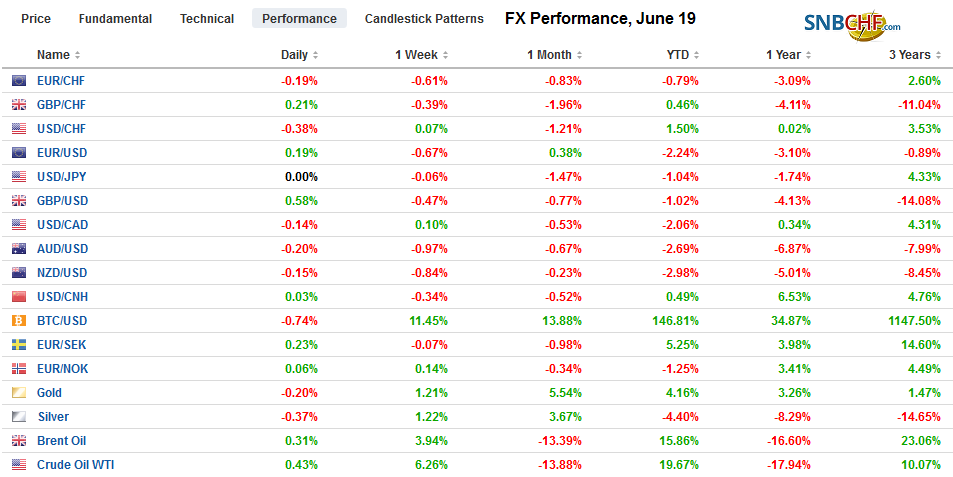

FX Performance, June 19 - Click to enlarge |

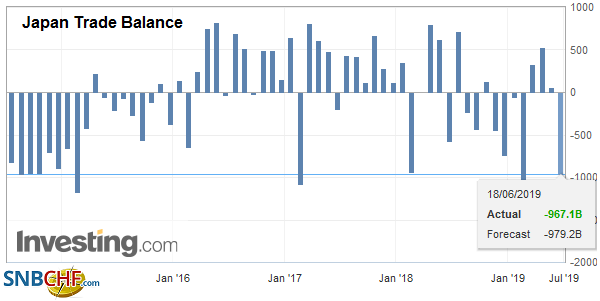

Asia PacificUS-Japanese trade talks are underway, and today’s data illustrates the challenge. Simply put, the days of Japan’s large trade surplus driving the current account surplus are history. Japan reported that after a three-month surplus, the trade balance returned to deficit. In the first five months of the year, Japan has recorded an average monthly shortfall of almost JPY300 mln. In the same period last year, the average deficit was near JPY30 mln. The current account, like Switzerland’s, for example, is driven by the investment income balance (profits, interest, dividends, licensing fees, royalties, etc.). Japan reported its sixth consecutive year-over-year decline in exports. The 7.8% decline is the largest since January. Last May, exports rose by 8.1% year-over-year. Chips and auto parts were important export drags (-30% and -12% respectively). In terms of destination, exports to China were off 9.7% year-over-year in May and down 6.3% in April. Exports to the rest of Asia fell 13.4% after a 1.6% decline in April. Exports to the EU were down by 7.1%, but exports to the US rose by 3.3%Imports unexpectedly fell by 1.5%. The median forecast in the Bloomberg survey was for a 1.0% gain. The weakness is seen as a reflection of the soft domestic economy. The BOJ meeting concludes tomorrow, and no change is expected, though pressure may be building for some technical adjustments given that it owns around 80% of the 7-10 year bonds and there is concern that it is disrupting activity. |

Japan Trade Balance, May 2019(see more posts on Japan Trade Balance, ) Source: investing.com - Click to enlarge |

For the eighth consecutive session, the US dollar sits on a JPY108-handle. Over this run, the dollar has finished the North American session roughly within 10 ticks of JPY108.45. There are nearly $1.2 bln in options struck between JPY108.30-JPY108.40 that expires today. There is a hefty $3 bln option struck at JPY108 that will also be cut. While volatility around the FOMC announcement may challenge the range, sizeable option expiries tomorrow may reinforce the range. Tomorrow sees $1.6 bln options at JPY108 and $1.2 bln at JPY109 roll-off. The Australian dollar initially made a marginal new high for the week before turning lower. The Aussie had approached $0.6900, where an A$512 mln option that expires today has been struck. Initial support is now pegged near $0.6860. The US dollar briefly traded below CNY6.90 for the first time in two weeks, but eventually edged slightly higher on the day.

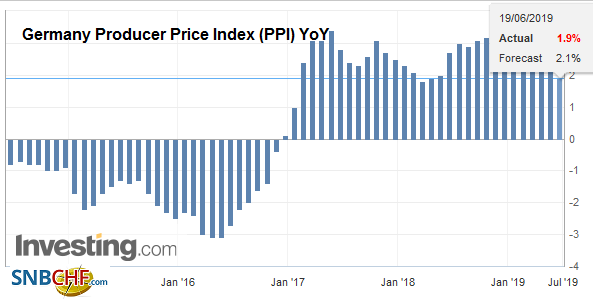

EuropeThere can be little doubt Draghi’s comments were impromptu. The ECB President knew exactly what he was doing, and he noted in a panel discussion that it was a deliberate recalibration of the message from the ECB meeting two weeks ago. There are three important takeaways. First, the bar to moving on policy is low. It does not require a deterioration of conditions; merely the lack of improvement. Anonymous sources told Bloomberg that a rate cut would be the likely first step even though Draghi indicated that there was also scope to re-start asset purchases if needed. Second, the ECB has made the judgment that uncertainty will linger and this uncertainty is itself the materialization of risk. Third, the US President’s claim that the ECB was manipulating the currency were rebuffed and more. Part of what is ailing the eurozone is the weakening of global growth for which tariffs and disruptive trade practice play an import role. The ECB may need to react further, and the market understood Draghi to signal a rate cut in H2 19 rather than in H2 20 as previously discounted. |

Germany Producer Price Index (PPI) YoY, May 2019(see more posts on Germany Producer Price Index, ) Source: investing.com - Click to enlarge |

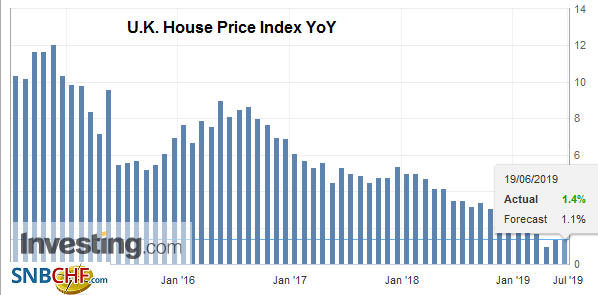

| Part of the uncertainty comes from Europe though too. Brexit uncertainty has increased. The risks of an exit without a deal have appeared to have risen. The Tory leadership battle continues. Johnson is seen as the hardest Brexit candidate left. Rory Stewart is perceived to have the mildest stance, and he practically doubled his votes round 2. A Johnson-Stewart choice for the 160k members of the Conservative Party would therefore arguably be the widest range. One consideration that has emerged that the commitment to leaving on October 31 is not ironclad. Johnson has appeared to soften his rhetoric by sounding more ambivalent. Meanwhile, Labour seems to be evolving to a more decisive “Remain” position and a referendum under all circumstances. |

U.K. House Price Index YoY, June 2019(see more posts on U.K. House Price Index, ) Source: investing.com - Click to enlarge |

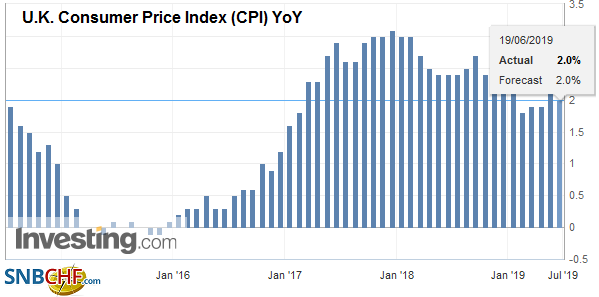

| Sterling was bid before the inflation data and spiked to session highs (~$1.2580) before pulling back. The May CPI was in line with expectations. CPIH rose 1.9% year-over-year (2.0% in April). The core rate slipped to 1.7% from 1.8%, which is the lowest since January 17. The BOE meets tomorrow and is expected to stand pay. Sterling needs to resurface above $1.26 to stabilize the technical tone. The euro is in a tight range. The bears want to see a better level to sell while the bulls were chastened by Draghi. Optionality may also deter the upside. Consider that there are around 5.7 bln euros in options struck between $1.1175 and $1.1210 that will expire today. Of those options, 3.3 bln are between $1.1200 and $1.1210. |

U.K. Consumer Price Index (CPI) YoY, May 2019(see more posts on U.K. Consumer Price Index, ) Source: investing.com - Click to enlarge |

America

We did not think that a Trump-Xi meeting would materialize, but there have been some noises in recent days that suggested some movement was afoot. China’s Vice Foreign Minister was in Washington, D.C. over the weekend. Because the staffs will meet first do some heavy lifting, it won’t be the impromptu, unscripted event in which we recognized would not suit Xi. The role of domestic American political considerations should almost be factored into the equation. While US election experts would caution against paying much attention to the polls at this stage in the cycle. The President does, and recently fired is polling team but not after polls showed Biden running well ahead in many states, including in the Midwest. Other Democrat candidates would also give Trump a run for his money, so to speak. Ultimately, even if ironically, enough people around Trump must recognize that the biggest threat to the economy, which is the main factor leading some Wall Street economists to forecast Trump’s re-election is the tariffs with China. An escalation would undermine the economy, which sucks the wind from his broader agenda. Perhaps a short-term trade deal may be politically more advantageous than standing on ceremony and demanding one deal that resolves all the multi-dimensional complexities. Mnuchin’s deal from last year might not look so bad. Trump’s language has changed. From wanting a “grand deal or no deal,” the US President now says a “fair deal” is desired.

With unemployment at a generation low, the Atlanta Fed’s GDPNow tracker anticipating another quarter of above-trend growth, the case of an immediate cut may not be compelling. However, Powell, we suspect, has learned from miscues, and likely wants to indicate that the Fed will act appropriately when needed. The Fed will probably acknowledge that crosscurrents remain powerful and that officials are taking it into account. Given the aggressiveness of the easing priced in–the January 2020 fed funds futures contract implies an effective average rate of 1.765% compared with the current rate of 1.38%. This means two cuts have been fully discounted and half of a third move. Fed officials will update their forecasts and some insight into how transitory they think the softness in price pressures last may be gleaned.

Canada reports May CPI today and a small increase is expected. It is unlikely to be much of a market factor. It is overshadowed by the FOMC meeting, and Friday’s retail sales report may be more important for investor sentiment. The Bank of Canada meets next on July 10 and is steadfastly on hold. The US dollar recorded a potential key downside reversal by making a new high for the move (a two-week high) before turning lower and finishing below the previous day’s low. The US dollar extended yesterday’s losses (to ~CAD1.3365) but is quiet in narrow ranges. Initial support is seen around CAD1.3350. A move above CAD1.34 may negate some of the favorable implications of yesterday’s action. The dollar is consolidating against the Mexican peso after falling to its lowest level since the tariff threat made, a little below MXN19.05. Initial resistance may be seen near MXN19.18.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: Brexit,China,ECB,EUR/CHF,FOMC,FX Daily,Germany Producer Price Index,Japan,Japan Trade Balance,newsletter,U.K. Consumer Price Index,U.K. Consumer Price Index,U.K. House Price Index,US,USD/CHF