Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

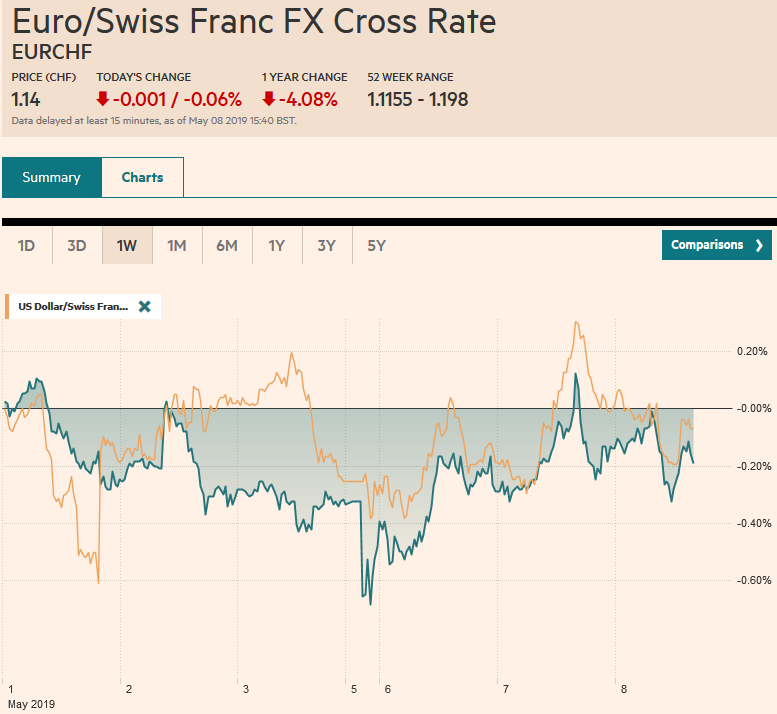

Swiss FrancThe Euro has fallen by 0.06% at 1.14 |

EUR/CHF and USD/CHF, May 08(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: It is taking investors a bit more than two sessions to find its footing after being the unexpected end of the tariff truce between the US and China struck last December. Asia Pacific equities tumbled after the S&P 500 shed nearly 1.7% yesterday, the third largest decline in 2019, but Europe’s Dow Jones Stoxx 600 is consolidating near yesterday’s lows. Germany reported an unexpected rise in industrial production, and it appears to be lending support to the DAX. US shares are little changed. European core bonds yields are steady to firmer, while peripheral bond yields are off two-three basis points. The 25 bp rate cut by the Reserve Bank of New Zealand (putting the cash rate at a record low (1.5%), was widely anticipated, and although it had little impact in the debt market, the New Zealand dollar was sold. The Kiwi joins sterling in being the underperformers today. The cross-party talks do not appear to be making much progress and pressure on May to step down is building. The other major currencies are straddling unchanged levels. The South African rand is the strongest among emerging market currencies as the country goes to the polls. The issue is ANC’s victory margin. If it garners 60% or more of the vote President Ramaphosa will be in a stronger position. |

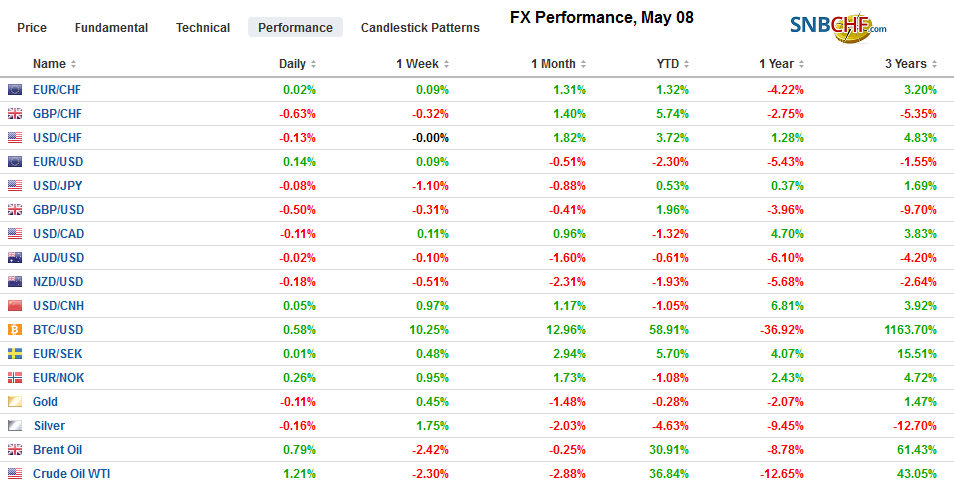

FX Performance, May 08 - Click to enlarge |

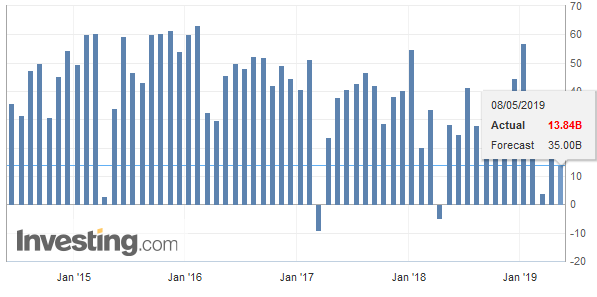

Asia PacificChina is proceeding with the trade talks with the US despite the fact it faces a US tariff increase in the middle of the two-day negotiations. Assuming that the US does indeed lift the tariff on $200 bln of Chinese goods to 25% from 10% before Friday’s negotiations, it ought not to be surprising if China also retaliates with its tariffs. Some see China pressing on with the talks as being conciliatory, but are unlikely to call the US being conciliatory if it continues to negotiate in the face of Chinese tariff increases. In a domestic dispute with American football players, the Trump Administration staged a couple of “impromptu” protests of their own. The speed at which a team with little experience in negotiating with China took offense and retaliated almost viscerally could itself be a tactic that the hardline camp was looking for an opportunity to deploy. Less than a week ago, press reports were playing up the likelihood of an agreement by the end of this week. Moreover, the US negotiators, who have been so critical of their predecessors, seem to have only belatedly come around to realize that a broad change in China’s industrial policy and other structural issues will not be forced on the PRC in these trade talks. Earlier today, China reports an unexpectedly large decline in its trade surplus. Like others in Asia, its exports are being hit, while the higher priced commodities boost imports. In dollar terms, exports fell 2.7% year-over-year, after a 13.8% rise in March. Imports rose 4% after a nearly 8% fall in March. This resulted in a $13.85 bln trade surplus in April after a $34.4 bln surplus in the previous month. In the current context, it is notable that China’s trade surplus has grown with the US by around 10.5% from the year-ago period. Some of this may reflect, US orders for Chinese goods that may have been front-loaded to beat some tariffs. Also, despite the smaller than expected April surplus, China’s trade surplus this year has averaged $22.3 bln a month. The average surplus in the first four months of 2018 was $17.7 bln. |

China Trade Balance (USD), April 2019(see more posts on China Trade Balance, ) Source: investing.com - Click to enlarge |

As widely anticipated, the Reserve Bank of New Zealand delivered a 25 bp rate cut that brought the cash rate to a record low of 1.5%. Weakness in the labor market and price pressures led the central bank to cut rates for the first time in three years. It is interesting to note that the RBNZ has a reformulated MPC that includes four internal members and three external, and a non-voting Treasury observer. Governor Orr acknowledged that the central bank sees a slightly lower path for the cash rate than implied with just one cut, but that there was a great deal of uncertainty surrounding that forecast. Some pundits had previously talked about a follow-up cut toward the end of Q3, but Orr seemed to suggest a longer wait-and-see stance.

The dollar slipped below JPY110 for the first time since March 26. The dollar stabilized in the European morning but is encountering some selling pressure near JPY110.20. There is a $666 mln option at JPY110 that expire today. It is the fourth day of dollar losses against the yen. The lows from last March were near JPY109.70. A break of the JPY109.50 could spur sharper losses. Recall that due to the cost of hedging, some Japanese institutions were buying US bonds on an unhedged basis. A break of JPY109.50 could prompt action either asset liquidation or new currency hedging.

The Australian dollar bottomed near $0.6965 at the start of the week and reached a high near $0.7050 yesterday before dipping below $0.7000 briefly today. Additional support is seen near $0.6980. The Chinese yuan also consolidated and remained in yesterday’s ranges. The New Zealand dollar was sold hard initially, falling to almost $0.6525 before short-covering kicked-in and fueled the Kiwi bounce to almost $0.6600 (yesterday’s close ~ $0.6605).

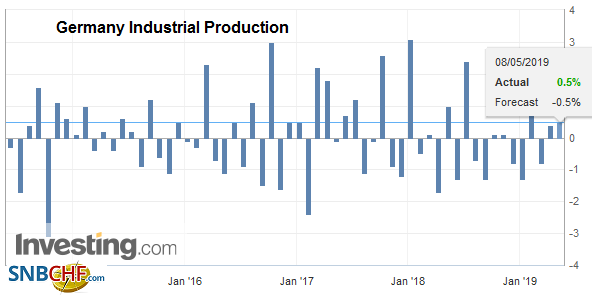

EuropeWe have noted that the survey data in Europe appears worse than the hard data, and German data underscored this observation. Economists surveyed by Bloomberg expected German industrial output to have fallen by 0.5% in March but instead, it rose by that magnitude. The April manufacturing PMI was below the 50 boom/bust level for the fourth consecutive month. After the February revisions, manufacturing boosted output for the second consecutive month in March. The February rise industrial output, which includes construction and energy, was revised to 0.4% from 0.7%. It also appears that the German auto sector is working through its issues and output rose by about 0.4% in Q1. Germany reports Q1 GDP next week and a 0.2%-0.3% quarterly gain is likely. |

Germany Industrial Production, March 2019(see more posts on Germany Industrial Production, ) Source: investing.com - Click to enlarge |

After a stunning loss of seats in last week’s local elections, there was a small window for the cross-party talks between the government and Labour. That window appears to be closing as the talks have reportedly not made much progress. If both parties had been sufficiently chastised by the electorate, a deal could have been struck in a few days, so the argument goes. The failure to reach an agreement this week is going to see the pressure on May to resign will increase. She has indicated she would resign once a deal is approved by Parliament. The Tory backbenchers are getting more impatient and are seeking her exit plan in light recent developments.

The euro is in a little more than a 10-tick range around $1.12. It reached a low yesterday near $1.1165. Yesterday’s high just shy of $1.1220 also corresponds to the 20-day moving average, which the euro has not closed above for nearly three weeks. There is also a 920 mln euro option struck at $1.1225 that expires today. Sterling is heavy. The problem with the risk of May’s departure is that her likely replacement would renew the risk of leaving the EU without an agreement. Sterling has largely traded in last Friday’s range (~$1.2990-$1.3180) this week. It is drifting toward the lower end now. The nearly GBP590 mln in an expiring option at $1.3085 held the early upticks. The question now is whether the option for almost GBP310 mln at $1.30 will be sufficient to prevent steeper losses. The intraday technicals suggest there is a reasonable chance that it will.

America

The S&P 500 gapped higher on April 1 and did not look back before reaching record highs on May 1. That gap is unfilled and may be important to the near-term outlook. That gap is found between 2836 and 2848.6. Yesterday’s low was 2862.6. On the upside, 2915-2920 area may be key. It houses the 20-day moving average and retracement targets of the recent setback.

The US economic calendar is light. The one Fed speaker today is Governor Brainard, who makes some opening remarks at a “Fed Listens” event before the US equity market opens. Canada reports April housing starts (a small increase is expected). Mexico’s calendar is empty today but the April CPI will be reported tomorrow and a small uptick is likely. Brazil reports April IGP inflation estimates today (a decline in the year-over-year rate to 8.15% from 8.27% in March is expected) ahead of the central bank decision, which is widely expected to keep the Selic rate at 6.5%, where it has been for nearly a year.

The US dollar is little changed against the Canadian dollar. It remains in a CAD1.34-CAD1.35 range. The US two-year premium over Canada is trending lower. Two weeks ago, it was near 80 bp and today it is slipping back below 70 bp. While under other circumstances that would support the Canadian dollar, the weakness in equities appears to be neutralizing it. The takeaway is that if equities do begin recovering, the Canadian dollar could outperform. The dollar continues to trade within last Friday’s range against the Mexican peso (~MXN18.91-MXN19.18). Year-to-date, the peso is up about 3% against the dollar. The Argentine peso is the worst performer in the region with its almost 17% depreciation this year, but the Brazilian real is a distant second with a 2.4% loss. The dollar has tested the BRL4.00-level a handful of times since late March but has been unable to close above it.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Brexit,China Trade Balance,EUR/CHF,FX Daily,Germany Industrial Production,newsletter,Trade,USD/CHF