Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

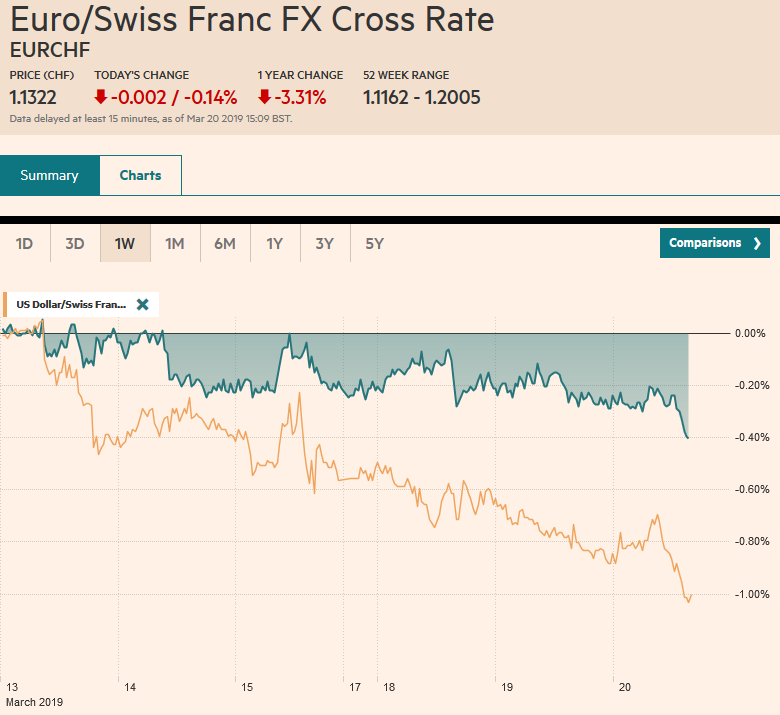

Swiss FrancThe Euro has fallen by 0.14% at 1.1322 |

EUR/CHF and USD/CHF, March 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: US stocks were not able to hold onto early gains yesterday, and this has helped set the stage for today’s heavier bias. Asia Pacific markets were narrowly mixed, with Japan and Korea eking out small gains while China and Taiwan slipped a little. Europe’s Dow Jones Stoxx 600 is threatening to snap a five-day advance as materials, healthcare, and energy leads the profit-taking while communication and real estate are proving a bit more resilient. Benchmark 10-year yields are little changed with peripheral European yields slightly firmer in this mild risk-off session. UK and US 10-year yields are 1-2 bp lower. The US 10-year yield struggles to hold above 2.60%. The US dollar is firmer against all the major currencies, with the apparent new threats of the UK leaving without an agreement weighing on sterling. |

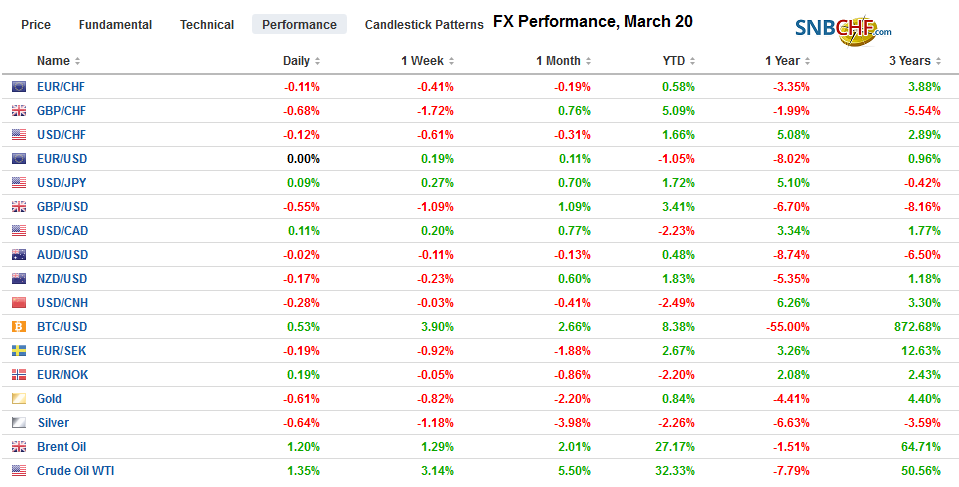

FX Performance, March 20 - Click to enlarge |

Asia-Pacific

Conflicting reports emerged yesterday about the progress of Sino-American trade talks. Some officials report that China is pushing back against US demands, especially apparently in intellectual property issues, which include pharmaceutical data, and patents. Other officials see it as part of the normal give-and-take of negotiations. US Trade Representative Lighthizer and US Treasury Secretary Mnuchin will go to Beijing next week and the following week Vice Premier Liu will return to Washington, D.C. for more talks.

As a consequence of the US decision to pull out of the Trans-Pacific Partnership and the signing of other local free trade agreements puts US agriculture at a disadvantage into Japan. Japan faces pressure from the US in the trade talks to put US agriculture on similar footing. Agriculture is also one of the hotly disputed areas between the US and Europe. Europe wants to exclude most agriculture issues for the trade talks.

The Japanese government echoed last week’s decision by the Bank of Japan in lowering its economic assessment. It is the first time the Abe government is doing so in three years. Exports and industrial output were specifically downgraded, though it said the economy was continuing to recover at a moderate pace. The poorer assessment of industrial output for a second straight month, saying it was nearly flat. The Japanese economy appears to be contracting in Q1, as it did in Q3. It is by virtue of the economic weakness that Abe may decide to again postpone the sales tax increase planned for October 1.

The dollar is firm against the yen, but it remains in the range seen in the final two sessions of last week: JPY111.15 to JPY111.90. The dollar is hovering around the middle of the range with a roughly $355 mln JPY111.50 option expiring today. There is a short-term downtrend line off the recent highs found near JPY111.80 today. There is a nearly $820 mln option at JPY112 that will be cut four hours before the Fed’s decision. An uptrend line from the end of February lows has caught the lows this month and is found near JPY111.20 today. After struggling to hold above $0.7100 yesterday, the Australian dollar was sold in early Asia when it briefly dipped below $0.7060. However, it has rebounded to $0.7085 in Europe. There is a large option for A$875 mln struck at $0.7100 that expire today. Hong Kong Monetary Authority intervened to support the Hong Kong dollar, which continues to threaten to break its band. The Chinese yuan resisted the strength of the US dollar. The greenback fell for the fourth consecutive session against the yuan and finished the onshore session below CNY6.70 for the first time this month. As expected Thailand’s central bank stood pat after hiking rates at the end of last year.

Europe

Reports suggest that the EU will offer the UK until mid-April to decide whether to extend Article 50 into 2020 or risk leaving without a deal. The small change in the date is thought to be sufficient to allow the Bercow, the UK Speaker, to allow a third vote on the Withdrawal Bill perhaps next week. It probably means that there will be an EU summit next week. Some countries are reluctant to grant a delay just for the sake of a delay without some new offering from the UK.

Separately, the UK’s headline February CPI ticked up to 1.9% from 1.8%. On the other hand, the core rate eased to 1.8% from 1.9%. CPIH, which includes owner-occupied housing costs, was unchanged at 1.8%. There is some talk that the BOE can raise rates in Q3, but we are not convinced, though we acknowledge the strong jobs growth and the firm price pressures. Interpolating from the OIS, the market has less than a 1 in 5 chance of a hike by the end of Q3. It increases to about 30% by the end of the year.

The euro is in less than a quarter cent range against the US dollar today, which is just inside yesterday’s range. Just below $1.1350 it is at the upper end of this week’s range, where the high has been a little above $1.1360. It reached its highest level since March 4. We had thought the technical potential was toward $1.14, but to get there in the next few hours, it needs to overcome roughly 1.9 bn euro options at $1.1390-$1.1400 that expire today. More like, the single currency may be trade between two other expiring options today: Around 645 mln euros at $1.1325 and nearly 510 mln euros at $1.1375. Sterling is almost a half a cent lower, but it is holding above Monday’s low (~$1.3185), which also corresponds to the 20-day moving average that has not closed below since March 12. Initial resistance is seen near $1.3260.

America

The FOMC meeting is here. The rhetoric since the December forecasts has changed dramatically. Today’s meeting is about realigning the two. This means that growth and inflation forecasts will be lowered. The hotly debated issue is the dot plots for the Fed funds rate. In December the median forecast was for two hikes this year. Six officials expected three hikes and five expected two. We get how the four than expected one hike could, fairly easily, shift to no hikes. We wonder if the six who thought three hikes can completely reverse themselves and if may be difficult to all who expected two hikes to fully retract. That said, economic activity in Q1 is particularly soft. In fact, the Atlanta Fed GDP tracker warns of near stagnation (0.4% annualized).

What could be Trudeau’s last budget for Canada was largely as expected. The stronger than expected revenues will be used to social programs and transfers, including skill training, support for seniors, and greater prescription coverage,

The US dollar spiked through the 20-day moving average against the Canadian dollar yesterday for the first time since March 1. It rebounded to close little changed on the session. Oil prices reversed. Equities could not hold on to their initial gains and the US premium over Canada on two-year money recovered from early softness. Initial resistance today is seen near CAD1.3370. The US dollar is flirting with MXN19.00, the lower end of its range since the end of January. The year’s low is a little below MXN18.90. Brazil’s central bank meets late today, and the overnight Selic rate is expected to remain steady at 6.5%. The dollar’s high for the year against the Brazil real was seen prior to the US employment data earlier this month near BRL3.90. Yesterday, it spiked down to nearly BRL3.7650, which is about the middle of this year’s range. A convincing move above BRL3.80 now would lift the greenback’s tone.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$EUR,$JPY,brl,EUR/CHF,MXN,newsletter,SPY,USD/CHF