Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

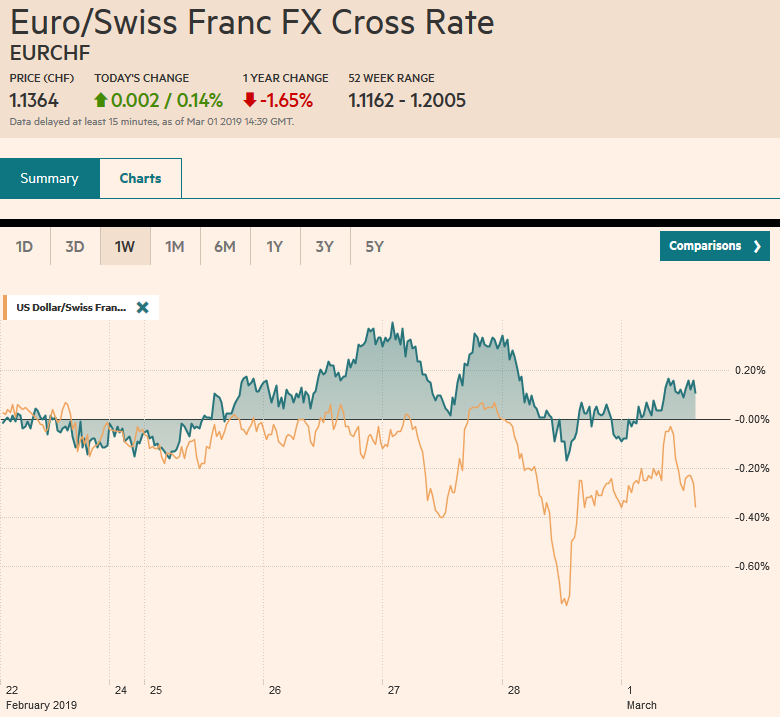

Swiss FrancThe Euro has risen by 0.14% at 1.1364 |

EUR/CHF and USD/CHF, March 01(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: News that MSCI plans to substantially boost China’s equity weighting in its indices and a better than expected Caixin manufacturing PMI and some easing of India-Pakistan tensions helped bolster the risk-taking appetite going into the weekend. This lifting equity and weighing on bonds. China’s CSI 300 rose 2.2% for a 6.5% weekly gain. The Shanghai Composite has risen every week this year. Europe’s Dow Jones Stoxx 600 is up 0.6% through the European morning and is up a little more than 1% for the week. It has been down only one week this year. The S&P 500 is carrying a three-day decline in tow, but the participants have not given up on the 2800 level and will make another attempt. Bond yields are mostly higher. The US 10-year yield closed above 2.70% for the first time since early February and is edging higher still today. It is up about six-seven basis point this week. The 10-year German bund yield has doubled in the past four sessions to 18 bp. The 10-year JGB yield remains slightly in negative territory. The dollar-bloc currencies are faring the best today, with the yen and Swiss franc doing the worst, which is consistent with the risk on mood. Although it is off about 0.2% today, sterling is the strongest currency this week on the back of ideas that the risks of no-deal have eased. |

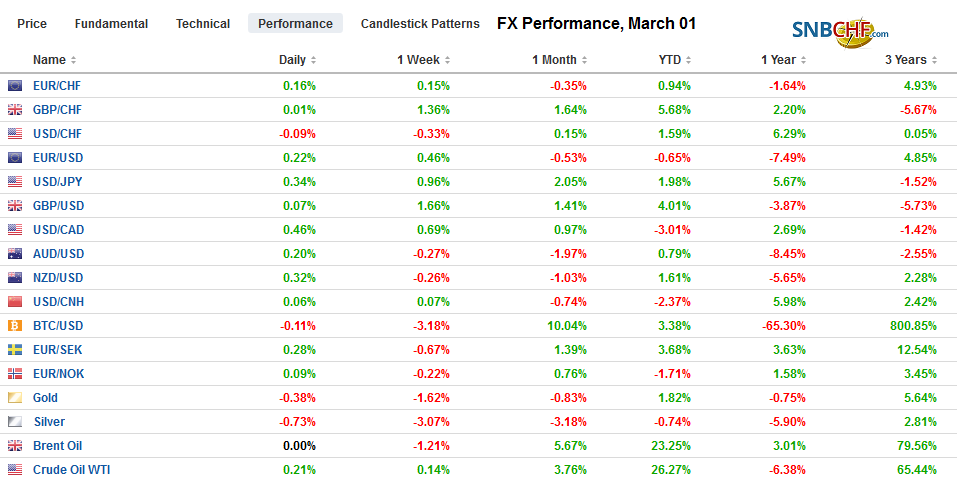

FX Performance, March 01 - Click to enlarge |

Asia Pacific

Last September MSCI indicated it was considering boosting the weighting of the mainland A shares in its indices. It confirmed its intentions yesterday to the surprise of no one and will boost China’s inclusion factor from the current 5% inclusion factor to 20%. This is not the same as weighting, though it confuses many observers. The inclusion factor reflects the percentage of the local shares that are included. The actual weighting in the MSCI flagship emerging markets equity index will rise from 0.71% to about 3.3% over the next nine months. However, rather than do it two steps, it will take three. This is part of the larger integration of China into the world capital markets. Many fund managers track or shadow the MSCI benchmark, and this will encourage more purchases of Chinese shares. The same thing is taking place in the fixed income world. Different index providers are adding Chinese bonds. Bloomberg, for example, will include Chinese bonds in its indices at the beginning of Q2. This is a source of demand for yuan and Chinese stocks and bonds. The MSCI decision is expected to boost inflows by $60-$70 bln.

China’s Caixin manufacturing PMI was better than expected at 49.9. It was at 48.3 in January and economists had expected a small rise. Although the reading is still (just) below the 50 boom/bust level for the third month, the report is part of the accumulating data that suggest the worst may be passed. New orders rose to 50.2 from 47.3. It is a three-month high and back into expansion territory. China;’s National People’s Congress meets for the next two weeks, and Trump and Xi’s meeting will likely take place shortly after the session ends.

Japan’s data were mixed. The 48.5 flash manufacturing PMI was revised to 48.9, though still well below the January 50.3 reading. Like the US reported yesterday with the GDP data, there was a strong jump in Japan’s Capex in Q4. In Japan, it surged by 5.7% from 4.5% in Q3. The four-quarter average of 6.6% in the highest since H1 16. Japan’s unemployment rate unexpectedly ticked up to 2.5% from 2.4%, though the job-to-applicant ratio remained steady at 1.63. Corporate profits disappointed, falling 7.0% (year-over-year) in Q4, the worst in two and a half years.

The dollar is testing the JPY112 level for the first time since December 20. Optimism on US-China trade and the lack of escalation in the India/Pakistan confrontation, and ideas that the Japanese economy is lagging behind others weighed is weighing on the yen. Note that the 100- and 200-day moving averages converge near JPY111.40 today. Nearby resistance above JPY112.00 is seen near JPY112.30, while the 2018 high was set in October around JPY114.55. This is the fourth consecutive week the dollar has appreciated against the yen and is the longest streak since last September-October. The Australian dollar tested $0.7200 in the middle of the week and is now trading in a narrow range on both sides of $0.7100. The central bank meets next week and although no one expects a change in the cash rate (1.5%), confirmation of a sub-50 composite PMI shortly before the meeting may see a dovish interpretation market participants of the RBA’s neutral stance. We would peg initial resistance in the $0.7130 area today, and there are nearly A$4 bln in expiring options struck between $0.7150 and $0.7175 today.

Europe

We suggested above that the Chinese economy may have turned a corner. It also looks like the eurozone might have as well, but it will not deter the ECB from moving toward a new long-term loan facility (TLTRO), and a commitment could come as early as next week’s meeting. Germany’s manufacturing PMI was confirmed at 47.6, but the other reports today were better than expected. Retail sales rose 3.3% rather than the 2% economists forecast in January offsetting the December decline in full (which was revised to -3.1% rather than the -4.3% initially reported). The unemployment rolls fell 21k in February, around four-times larger of a decline than expected, while the unemployment rate was steady the cyclical low of 5%, where it has been since last November.

The French manufacturing PMI edged up to 51.5 from the 51.4 flash reading and 51.2 in January. It is the second consecutive monthly increase. The fact that French exports are a smaller part of world exports than Germany and its manufacturing sector has fared better is consistent with a Chinese shock hitting Germany (on top of the idiosyncratic auto sector development). Italy remains in contraction mode at 47.7 from 47.8 in January. So far, the weakening economy has had little impact on the popularity of the government. The Five Star Movement, ostensibly the senior partner in the coalition has not done well in the local elections that have been held while the League seems to act as if it were the senior partner, has seen its support increase. However, the disappointment in PMI is in Spain, which has enjoyed a robust expansion. The manufacturing PMI fell to 49.9 from 52.4. Spain holds national elections next month.

For the euro area as a whole, the manufacturing PMI stands at 49.3, a little better than the 49.2 flash, but off the below 50.5 in January. Indeed, it has fallen without fail since last July. Separately, the Eurostat reported that unemployment rate for EMU is at a new cyclical low of 7.8%, but that it was reached in January rather than February for the first time. Eurostat also confirmed February’s headline inflation ticks up to 1.5% from 1.4%, but that the core rate was slipped to 1.0% rather than remain unchanged at 1.1%.

The euro steadied in the European morning after reaching a low a little above $1.1350 in late Asian turnover. There is a 2.0 bln euro option struck there that expires today. On the upside, there is a nearly 650 mln euro option at $1.1385 that also will be cut today. Yesterday the euro did turn around in front of $1.1425 where a 2.1 bln euro option expires today. Ahead of the ECB meeting next week, which is likely to be a dovish hold, the market may be cautious about taking the euro to close to the top of its recent range. After rallying to $1.3350 in the middle of the week, sterling is lower for the second day amid light profit-taking and the soft manufacturing PMI (52.0 from a revised 52.6, initially 52.8) did not help. Still sterling is up nearly two cents on the week and, barring a large sell-off, will be back-to-back weeks of over 1% gains. Initial support is seen near $1.3220-$1.3230.

America

Although Q4 18 US GDP was a little stronger than most expected, the rise in inventories coupled with slower consumption suggests that they were unwanted, and may weigh on Q1 18 output. The December PCE data is already incorporated into the GDP figures, but the market will be interested in the deflators, and the headline may ease to 1.7% from 1.8%, while the core is expected to be steady at 1.9%. The February PMI and ISM offer headline risks and the University of Michigan’s consumer confidence and especially the inflation expectation components draw attention. The February auto sales data will also be reported. It typically does not impact trading, but it offers important insight into consumption and health of the economy.

Canada reports Q4 18 GDP. It is expected to have slowed to 1% from 2% in Q3. December monthly GDP is likely to be flat after contracting (0.1%) in two of the past three months. Prime Minister Trudeau has come under more pressure from trying to influence a judicial matter. The already was vulnerable ahead of the national elections later this year. A cabinet reshuffle is expected as soon as today.

The US dollar is flat against the Canadian dollar this week at the start of the last North American session. There is a large $1.1 bln option expiring today at CAD1.3150. The US dollar is up about 0.6% against the Mexican peso this week. It will be interesting to see if the February manufacturing PMI recovers above 50 from 49.8 in January. The dollar is in the upper end of its two-week range against the peso, call it MXN19.33. The low for the week was set on Monday near MXN19.00. Meanwhile, the Dollar Index is up for the third consecutive session after previously falling for three straight sessions. Yet at 96.25 it is still off about 0.25% on the week. The 96.60-96.80 area may be key next week, that features not only the ECB (and RBA and BoC) meetings but also US jobs data, where the early call is for about 185k increase in non-farm payrolls and an acceleration of earnings.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,MXN,newsletter,USD/CHF