Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

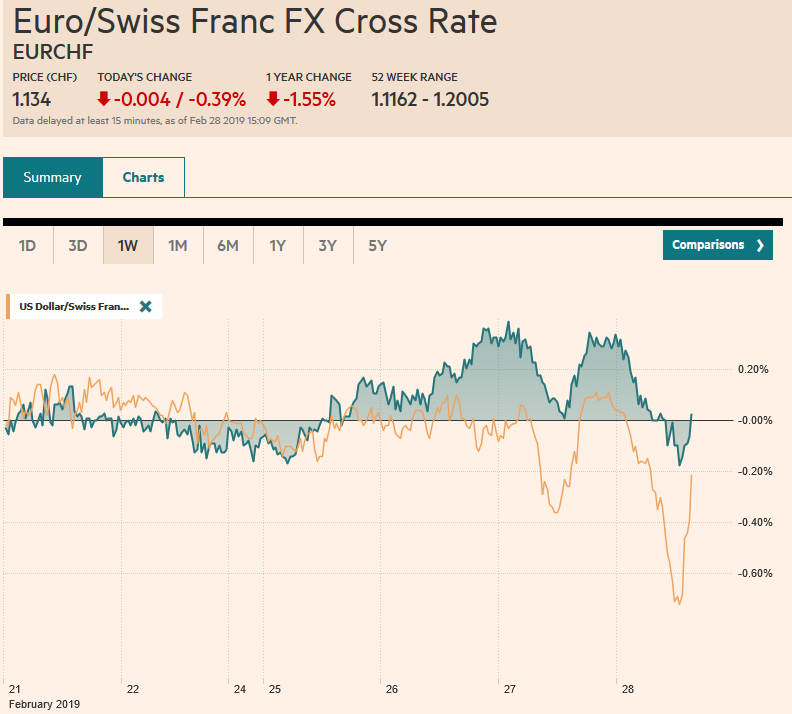

Swiss FrancThe Euro has fallen by 0.39% at 1.134 |

EUR/CHF and USD/CHF, February 28(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: News that the US-North Korean summit ended abruptly without an agreement spurred losses in equities and gains in the Swiss franc and Japanese yen. US President Trump willingness to walk away from the talks is important in and of itself, but it also sends a warning not to go all in on a US-China trade agreement that could also sour at the last minute. North Korea may express its displeasure by renewing missile tests. In addition, the tension between India and Pakistan remains in a heightened state. Equities in Asia Pacific (with the notable exception of India and Australia) and Europe are lower, and US shares are trading softer in Europe. Gold is firm, though below yesterday’s high ($1333). Oil is paring yesterday’s ~2.5% gain helped by the biggest drawdown of US inventories (8.65 mln barrels), which snaps a five-week build and offsets in full the past three weeks of stock building. The dollar is mixed, with the dollar-bloc currencies and sterling lag, while Sweden’s strong Q4 GDP (1.2% quarter-over-quarter rather than 0.6% median forecast in the Bloomberg survey) has lifted the krona to the top of the boards with around a 0.8% gain. |

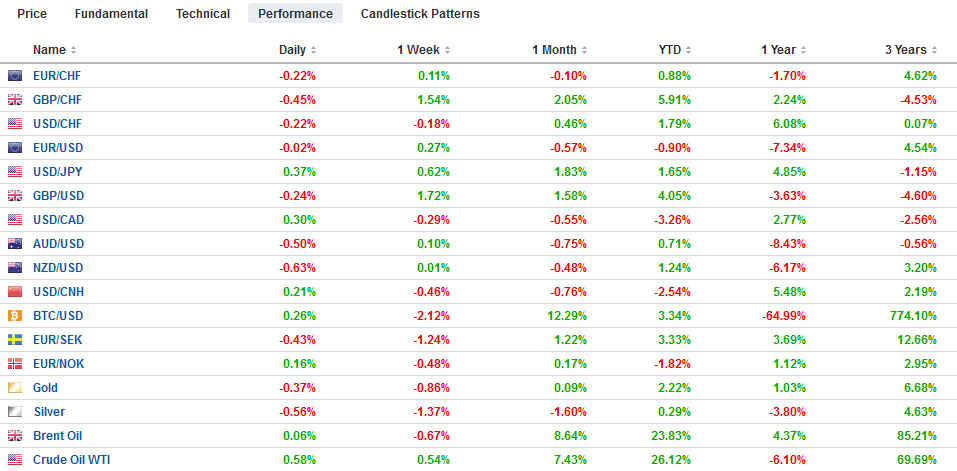

FX Performance, February 28 - Click to enlarge |

Asia Pacific

Japan reported disappointing data that cannot simply be dismissed due to the usual distortions at the start of the year. January industrial output tumbled 3.7%. Economists expected something closer to a 2.5% decline. The data may be exaggerated, but the direction is clear. It is the third consecutive month that industrial output fell. Moreover, the decline over the past three months is the largest in eight years. The same general pattern is seen in retail sales, which Japan reported fell 2.3% in January. It was three times larger a decline than economists expected. It is the second decline in three months, during which time retail sales have fallen most in two years.

China disappointed. If the official PMI is manipulated by the government as some suspect, they are not doing a good job. The official manufacturing PMI fell further into contraction territory at 49.2 (from 49.5). This is a three-year low. The output component fell below the 50 boom/bust level for the first time since 2009. The non-manufacturing PMI slipped to 54.3 (from 54.7). Construction was notably weak. Investors seemed to look past disappointment, perhaps persuaded as we, that Chinese officials are committed to doing whatever it takes strengthen the economy, which avoids the further estrangement of the people from the Party and illustrates its resolve in the face of a foreign threat.

The dollar is trading a little softer against the yen but remains in the upper end of yesterday’s trading range. Recall the high for the week was recorded on Monday near JPY111.25. Yesterday, the low for the week was recorded near JPY110.35, which coincided with the 20-day moving average, which the dollar has not closed below this month. There is a $500 mln option at JPY110.40 that expires today. The Australian dollar posted an outside down day yesterday by trading on both sides of Tuesday’s range and closing below its low. However, there has been no follow-through selling today, and the Aussie is consolidating mostly in a narrow range of $0.7130-$0.7150. There is an expiring option for A$935 mln struck at the upper end of that range that may be reinforcing the cap.

Europe

Here is where Brexit stands: The UK and EU are working on a codicil or annex to the Withdrawal Agreement to ease some MP concerns that it is some kind of a trap to keep the UK in the EU indefinitely. This is expected over the next week or so. This will allow a new vote by March 12. If the Withdrawal Bill is rejected, the following day will be a vote on leaving with no deal, which some MPs think is preferable to the Withdrawal Bill. If this is rejected, the following day will vote on seeking a formal extension. A formal extension or a Withdrawal Agreement will be finalized at the March 21-22 EU Summit. In some ways, Corbyn’s formal acceptance of the party’s plank calling for a second referendum played into May’s hands. May implied that a second referendum was a Trojan Horse with the Remain Camp hidden inside, ready to overturn the 2016 results. The risk that defeat could be snatched from the jaws of victory that was a month away now is forcing even some of the most virulent Leavers to pause. Perhaps one of the most successful tactics of the Prime Minister was to shift the brink from a no-deal exit to no exit.

A quiet week for data in Europe ended with a bang today. The large EMU countries reported preliminary February inflation figures ahead of the aggregate report tomorrow. Headline inflation likely rose from 1.4% to 1.5% and maybe even 1.6%, depending on the rounding. Core inflation is more difficult to project based on the preliminary data, but it does look like motor fuel helped lift the headline rate. The core rate was 1.1% in January. French consumers are have begun the year on a firm note with consumer spending jumping 1.2% in January nearly offsetting December’s 1.5% plunge. Year-over-year, consumer spending rose 1.0%. In December it was off 2.3%. Spain’s current account surplus surged as it typically does in December, rising to 4.7 bln euros from 1.8 bln euros in November. The December 2017 surplus stood at 5.06 bln euros. Spain’s current account surplus was roughly halved last year. As we noted, Sweden’s Q4 GDP rose 1.2%, twice as strong as expected and Q3 GDP was revised to show a 0.1% contraction rather than 0.2%. The New Year started on firm footing as retail sales rose 0.8% and the December series was revised to -0.9% from -1.4%.

The euro remains firm near $1.14. It has been capped in this area over the last couple of sessions as well. It “feels” like it wants to break it, though a 700 mln euro expiring option struck there may be helping put up a fight. Tomorrow there is a 1.8 bln euro option at $1.1425 and another one at $1.1450 for 1.5 bln euros that will be cut. Note that the 61.8% retracement of the euro’s decline this month is found just shy of $1.1410. Given the likelihood of a dovish hold by the ECB next week, we would be more inclined to sell into euro gains into those option strike areas. Sterling is consolidating after a four-day 2% rally. It is stalling today in front of $1.3325, where a GBP1.1 bln option expires today. Pullbacks remain shallow, and the $1.3230-$1.3270 area offers initial support. The euro is paring its recent losses against sterling and is testing the GBP0.8575 area, which holds a 590 mln euro expiring option. Resistance is seen in the GBP0.8600-GBP0.8625 area.

America

The US reports Q4 18 GDP today. It was delayed by the government shutdown, and although there is much anticipation for it, the risk is that it is anti-climactic. It is too historical to have much impact outside of the headline effect. The Fed has already responded to it-the tightening of financial conditions and the increased crosscurrent–but adopting its new patient and flexible stance. Estimates to Q4 GDP have slid as the delayed high-frequency data has been digested. The Atlanta Fed’s GDPNow tracker was updated after yesterday’s economic reports, and it now sees 1.8% Q4 18 GDP, which is where the median Fed forecast puts trend growth. While Q1 growth also looks soft, it could turn out to be a quarter of two halves with the government shutdown and cold snaps slowing economic activity in the first part and recovery in the second. That is what the Chicago PMI may show when it is reported today too.

Higher oil prices helped offset the benign inflation report on the Canadian dollar yesterday. It may not be so fortunate today. An influence-scandal may make it more difficult for Trudeau to be re-elected later this year and the geopolitical developments are not helpful for the currency. The CAD1.3200-CAD1.3210 area is interesting. It houses the 20-day day moving average, a retracement objective, and a roughly $615 mln option that expires today. The dollar is in tight ranges against the Mexican peso. The implied volatility is continuing to fall. Today, three-month implied volatility is at its lowest level (~11%) since October 2017.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$AUD,$CAD,$EUR,$JPY,EUR/CHF and USD/CHF,FX Daily,MXN,newsletter,SEK,SPX