Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

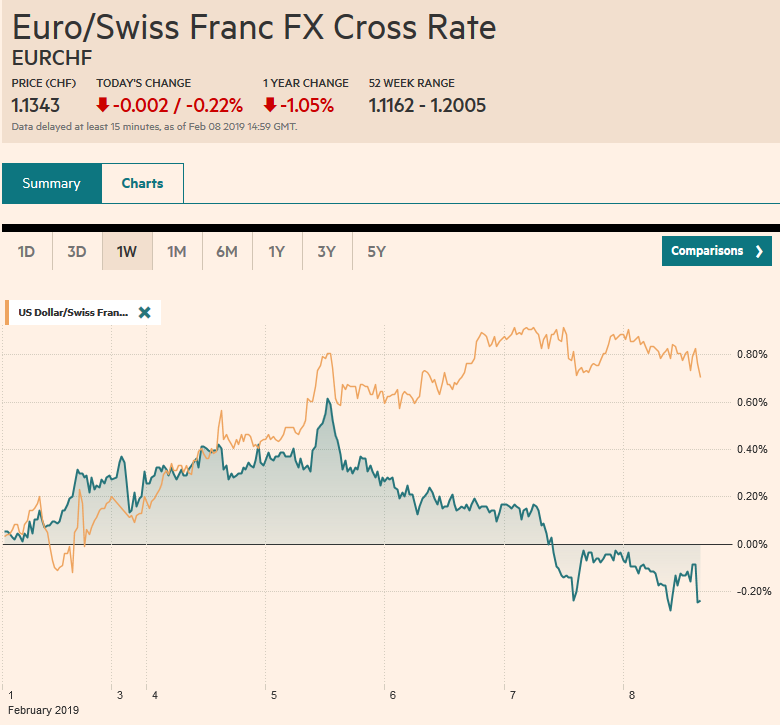

Swiss FrancThe Euro has fallen by 0.22% at 1.1343 |

EUR/CHF and USD/CHF, February 08(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: As North American traders return to their posts to put the finishing touches on the week’s activity, the Dollar Index is extending its advance for a seventh consecutive session. If sustained, it will be the longest advance since February 2017. The rally was sparked after the dovish FOMC statement had sent the greenback lower and the employment data raised the possibility that the Fed overreacted to the stock market volatility. The S&P 500 turned back from the 200-day moving average and gapped lower yesterday (~2719-2724) setting the tone for the still holiday-thinned Asian markets, where the MSCI Asia Pacific Index fell for a third session, to snap a four-week rally. European shares are faring better, and Dow Jones Stoxx 600 is poised to extend its streak for the sixth week. Benchmark 10-year bond yields are mostly a little lower. Oil is trading heavily, and with WTI for March delivery near $52.40, it is off more than 5% this week, the largest decline since late December. On the other hand, the shock from Vale is still behind iron ore’s surge. Today’s 5% rally bring it to a five year high. |

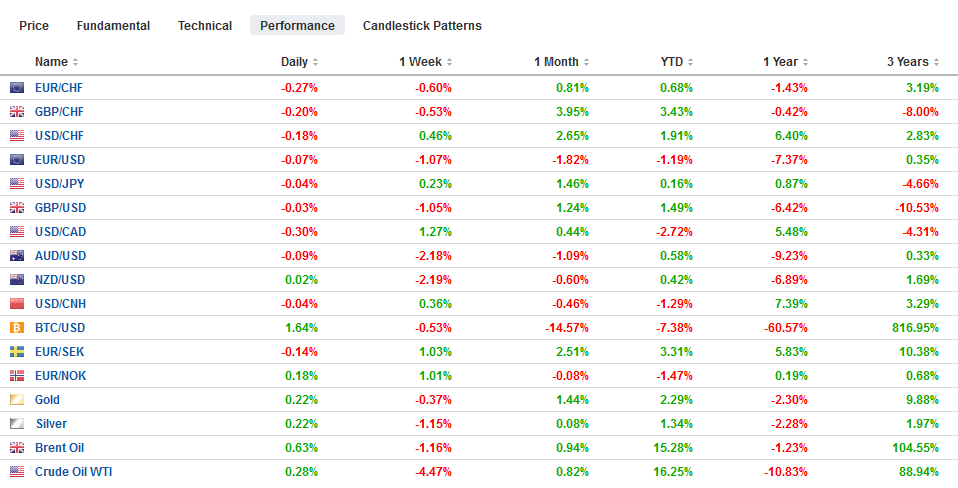

FX Performance, February 08 - Click to enlarge |

Asia Pacific

When the Reserve Bank of Australia left rates on hold and did not appear to change its stance much the Australian dollar traded firm, but subsequent “clarification” has seen the Aussie tumble. Governor Lowe’s neutral bias was quantified in today’s Monetary Policy Statement. Growth and inflation forecast were cut. The Australian economy is expected to grow 2.5% in the year through June, down from 3.25% previously. And growth in the following year was cut by half a percentage point to 2.75%. The softer inflation forecast was attributed to oil, with core inflation remaining near 2%. The forecasts would suggest an easing bias rather than a neutral stance that Lowe claims. Yet, the RBA still seems to be counting on the strength the job growth to boost wages and inflation. The underlying issue is whether the weakness in property prices will crimp consumption and growth. Australia’s 10-year bond yield fell 13 bp this week to 2.10%. The record low was set in August 2016 near 1.80%.

Japan’s December current account surplus, seasonally adjusted, was broadly in line with expectations. A key point to remember is that Japan’s current account surplus is not driven by the trade balance as much as the investment income balance. Consider the trade surplus on the balance of payments basis was about JPY216 bln, while the seasonally adjusted current account surplus was roughly JPY1.56 trillion. Separately, and arguably, more importantly, Japan reported the first increase in overall household spending since August. It eked out a 0.1% rise year-over-year in December. On the other hand, Japan’s leading economic indicator fell for a fourth month in December, and at 97.9 it is at the lowest level since October 2016.

The dollar’s range for the week against the Japanese yen was set on Monday (~JPY109.45-JPY110.15). Thus far today is the first day this week, the dollar has not traded above JPY110, where a $640 mln option expires today. The market does not appear to have given up on trying to establish a hand-hold above JPY110, though it would seem to require stronger equities and/or higher yields. The Australian dollar is off about 2.4% this week (~$0.7075). The next downside target is near $0.7020. The New Zealand dollar also has sold-off this week, and its 2.2% decline (~$0.6750) is the largest since August.

Europe

The euro made a marginal new low for the week, dipping below $1.1325 briefly. The pessimism toward EMU was not changed by today’s data, which, on balance, was a bit better than expected. Italy’s was not. December industrial output slumped 0.8%. The median forecast in the Bloomberg survey was for a 0.4% rise. However, news from France was better. French industrial production was expected to rise 0.6%. Instead, it rose 0.8% and manufacturing output itself was up 1.0%. This recoups most of the weakness since in November. For its part, Germany reported a considerably smaller trade surplus (13.9 bln euro in December vs. 20.4 bln euros in November, but more importantly, imports and exports recovered smartly. After falling 0.3% in November, exports rose 1.5%. Imports rose 1.2% after falling 1.3% in November.

UK Prime Minister May is still asking for some dilution in the plan for the Irish backstop, even though everyone has said not. Indeed, the backstop is in case no agreement is reached. There cannot be a time limit or it undermines the very purpose of the backstop. It would encourage delay tactics until the time limit passed. Meanwhile, a vote in Parliament that was expected next week looks likely to be delayed. Although everyone says they want to avoid a no-deal exit, it can still be stumbled into, and that continues to worry investors.

If the euro’s losses are sustained, it will be the first week since May 2018 that it has fallen in each session. Yet all that has happened is that the euro has gone from the upper end of its range (~$1.15) to the lower end of its range (~$1.13). Indeed, it should not be surprising for the euro to snap its losing streak and close higher ahead of the weekend. Large option expires today $1.1280 and $1.1380 do not seem particularly relevant, but there is a 2.0 bln euro option struck at $1.1365 on Monday that may be interesting. Sterling is trading higher for the second day in a row, but it won’t be enough to prevent the second consecutive weekly loss. Yesterday’s losses nearly fulfilled a retracement objective (50%) of the rally since the flash crash in early January that is found near $1.2830. Its recovery suggests that perhaps some move was completed. On the upside, a move through yesterday’s high near $1.30 would confirm a more constructive near-term technical outlook.

America

Trade talk optimism was hit yesterday. President Trump apparently indicated that there will be no meeting with China’s President Xi before the early March deadline. Economic adviser Kudlow’s assessment that there were still sizeable differences gave the sense that the lack of substantial progress was the reason the two presidents won’t meet rather than a schedule conflict. At the same time, the battle over Chinese telecom companies continues, and formal action in the US will be forthcoming. Meanwhile, Germany is balking and is opposed to banning Huawei, for example. This will likely server to exacerbate tensions as the US-Europe trade talks move into focus. The UNCTAD found that Europe is poised to benefit the most from US-China trade tensions, though as a percentage of trade, Mexico, Vietnam, Australia, and Brazil may be larger beneficiaries from China looking for alternative sources of inputs.

There are no important US economic releases and the only Fed officials to speak is Daly, the new San Fransico Fed President. Canada reports housing starts and employment figures. The US dollar is breaking a five-week slide against the Canadian dollar. This week’s 1.6% (~CAD1.3315) gain offsets in full losses from the past three weeks. We see three drivers for the US-Canada exchange rate (short-to-medium term), interest rate differential, equity markets, (risk appetite) and oil prices. All three moved against the Canadian dollar in recent days. The nearby target is CAD1.3330 and then CAD1.3370. Mexico may announce a capital injection into PEMEX today. The central bank, as widely expected left overnight rate at 8.25% yesterday. The peso looks to be going nowhere quickly as the greenback remains chopping in a MXN19.00-MXN19.20 range.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$JPY,EUR/CHF,FX Daily,MXN,newsletter,SPX,USD/CHF