Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.09% at 1.1333 |

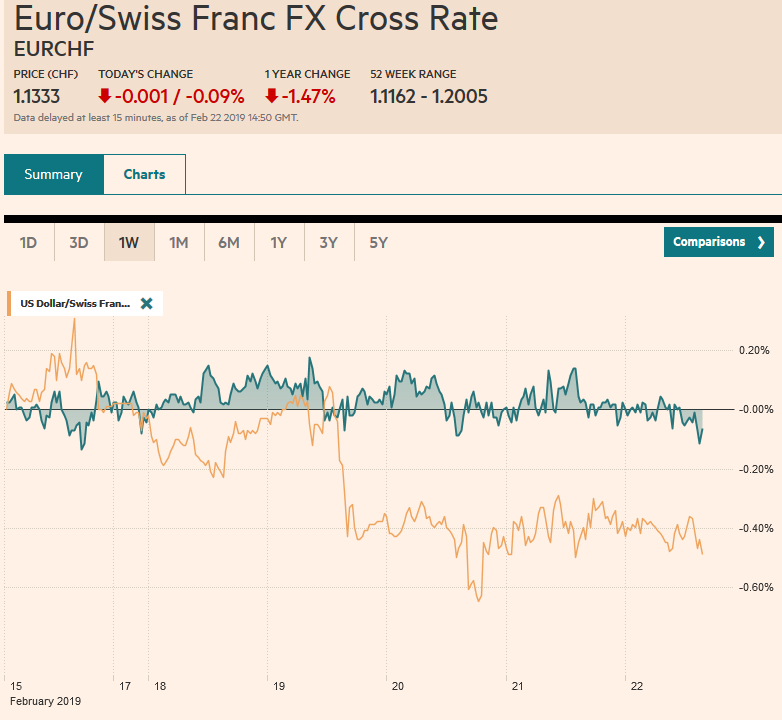

EUR/CHF and USD/CHF, February 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The global capital markets are winding down what appears to be an inconclusive week quietly and on a mixed note. The MSCI Asia Pacific Index is poised to snap a four-day advance but held on to a nearly 2% gain for the week. European bourses are mostly higher, and although the weekly advance of around 0.5% may not be that impressive, Dow Jones Stoxx 600 has only fallen in one of the first eight weeks of the year for a 9.5% year-to-date gain. Benchmark yields are mostly one-two basis points lower, with Australia and Italy the notable exceptions. The US dollar is confined to its well-worn ranges and is narrowly mixed. The Australian dollar has pared yesterday’s losses amid efforts by officials to play down the disruption of coal exports to China. Sterling is a little heavier on the day, but it is holding on to a 1% gain for the week. A delay in both Brexit and an escalation of US-China tariffs looks increasingly likely. |

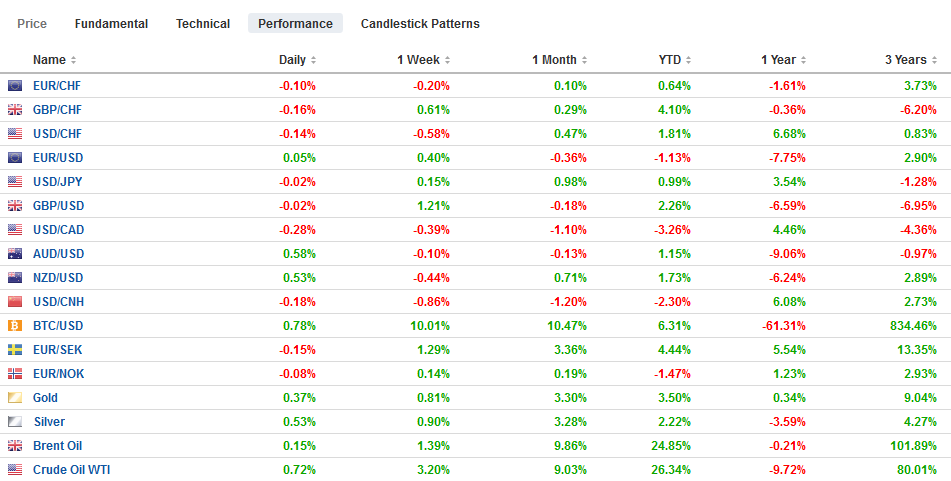

FX Performance, February 22 - Click to enlarge |

Asia Pacific

Australia’s Treasurer and the Governor of the Central Bank tried minimizing the significance of the disruption of coal exports to China. Reuters reported yesterday of the disruption, and the Australian dollar fell sharply. The slowdown of Australia’s coal exports may have begun last month, and RBA Governor Lowe tried linking it to environment and profitability issues and not to the controversy over Huawei. It is difficult to know. China uses its commercial power to express its displeasure, and there is a lack of transparency. This ambiguity keeps China’s adversary off-balance. Investors will be sensitive to data that shed light on these developments.

The Reserve Bank of New Zealand warned that raising capital requirements for banks could, all else being equal, tighten financial conditions. This, in turn, could pressure the RBNZ to cut rates to offset this “regulatory” tightening. The RBNZ is proposing lifting the Tier 1 capital requirement to 16%, or nearly double current levels. A formal decision is expected in Q3.

Japan’s underlying measures of inflation ticked up in January, though the headline was was unchanged at 0.2%. Excluding fresh food, which is how Japan measures its core rate, rose 0.8%, up from 0.7% at the end of last year. The target is 2%. Excluding fresh food and energy, inflation rose to 0.4% from 0.3%.

The Australian dollar had tumbled from $0.7200 yesterday to about $0.7070. Despite the bearishness of the price action (outside down day), there has been no follow-through selling. The Aussie is consolidating in roughly a 20 tick range on either side of $0.7100. At the middle of the range, the Australian dollar is off about 0.5% this week. We suspect the bears to sell into additional gains that could extend to $0.7140. The dollar has risen against the yen in four sessions this week and is poised to close higher for the third consecutive week. That said, the range has been exceptionally narrow–JPY110.40-JPY110.95. Three-month implied volatility has broken down, and at below 6.2%, it is at new five-year lows today.

Europe

Reports suggest that EU officials expect the UK to ask for a three-month extension. Any longer would complicate the EU Parliamentary elections at the end of May. EU officials are likely to grant the extension after pressing the UK. The risk of a disruptive no-deal exit is scaring some policymakers, and as many as 100 Tory MPs are threatening to vote against May’s bill next week to force a delay. Yesterday’s EU -UK talks ended without a fresh agreement, but the talks will continue next week. There is some talk that both the UK and EU could issue parallel statements that show a more benign interpretation or expression of will that some think may be sufficient to bolster May’s support.

Germany confirmed its practically flat Q4 GDP. The details were interesting. Consumption and investment rose (0.2% and 0.9%) respectively, but appeared to be offset by a decline in inventories, which, in turn, is tied to the auto sector. Many observers from debtor countries complain about Germany’s near-permanent austerity, but the breakdown of GDP data showed that government spending surged in Q4 by 1.6%, the strongest since Q1 16. Separately, and disappointingly, Germany’s IFO February survey showed no improvement in sentiment. The sense of the current climate eased to 98.5 from 99.3. Expects slipped to 93.8 from 94.3, the lowest since 2012. The overall assessment deteriorated to 103.4 from 104.5, a fresh two-year low.

The record from the recent ECB meeting boosted expectations that a new targeted long-term refinancing loan (TLTRO) will be announced next month, but the modalities or details might not be announced until later in Q2. The issue is not old loans are coming due this year, rather after the middle of the year, the previous four-year loans will have a year left. This puts them into a short-term financing bucket, and the banks are under regulatory pressure to minimize. In addition, if the loans are paid back, the ECB’s balance sheet would shrink.

Thus far the euro has been confined to a less than a quarter cent range against the dollar. It closed last week a little below $1.13 and has closed every session this week above $1.13. The three-month implied vol has softened this week but around 6.3%, it is a little above the month’s low (~6.2%), which itself was the lowest since late 2012. There is a large option (1.6 bln euros) struck at $1.13 that expires today. The euro looks trapped in a $1.1320-$1.1370 range. Sterling is trading at a three-day low near $1.30. The intraday technicals favor it holding. Three-month vol peaked early last December near 15%. It reached a low last month near 10% and is now near 11.4%. The prospects of a delay may be keeping the bears at bay, but this seems to be largely discount, making near-term outlook difficult.

America

President Trump will reportedly meet with China’s Vice Premier and point man in the trade talks Liu He. This is thought to help facilitate a meeting between Trump and Xi for next month. A Bloomberg survey found that nearly everyone polled did not expect tariffs to go up on March 1. However, 18 of the 29 do expect tariffs to go up eventually.

There is much press coverage of the report indicating that one of the US asks is for a stable yuan. We suspect this is being blown out of proportion. First, it is not new or even controversial. The US has expressed this concern before, and Chinese officials say they too want a stable yuan. Second, the G7 and G20 have endorsed letting market forces determine exchange rates. Many observers see a contradiction between market forces determining exchange rates and the US wants China to have a stable yuan. However, the contradiction is more apparent than real. One gets to a stable currency not be intervening, but by pursuing balanced policies. Third, the fact that the US housing market remains nationalized or that the US recapitalized banks during the crisis, does not deter US officials from pressing China to reduce the role of the state in its economy, suggesting officials are not hampered cognitive dissonance.

After a slew of data yesterday, the US economic calendar turns quiet today, but headline risk is presented by at around eight Fed officials speaking today. Investors learned this week that most officials favor ending the balance sheet operations this year, though a full rationale has not been delivered. On the other hand, there is still a subtle tightening bias as there was no apparent discussion of the conditions that would warrant a cut, but there was regarding a hike. Canada reports retail sales. They likely declined for the second month, and when autos are excluding, sales probably fell for the fourth month. Yesterday’s comments from Governor Poloz suggested that while the central bank’s normalization is not over, it is in no hurry to continue it by hiking rates. The Canadian dollar fell every week, but one in Q4 18 and is the strongest major currency this year with a 3% advance. It has only fallen one week this year, but this week’s gain of a less than 0.25% could be under risk if the retail sales are disappointing. Note that there is an option for a little more than $500 mln at CAD1.3215 that expires today and the greenback is hovering around it in the European morning.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,newsletter,NZD,USD/CHF