Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

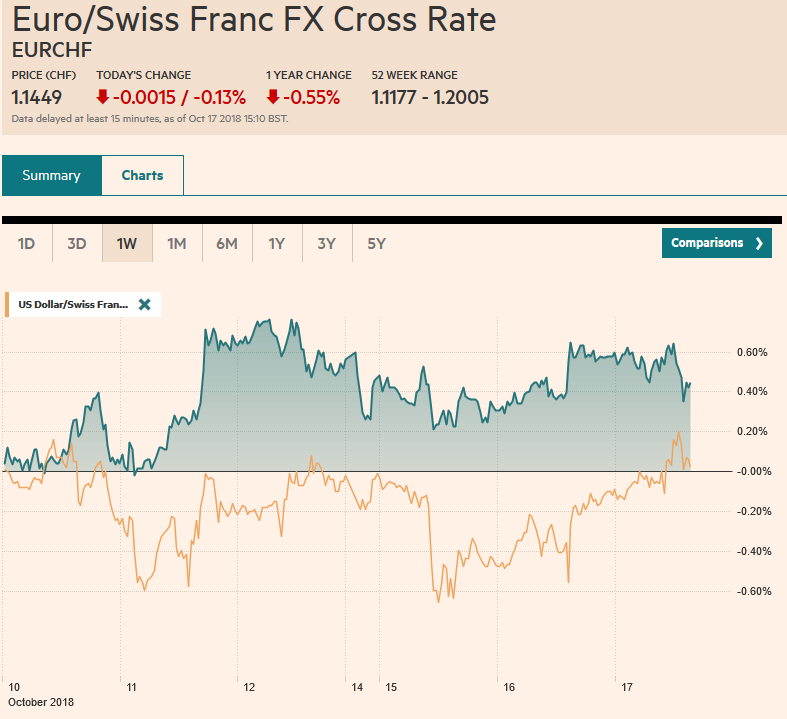

Swiss FrancThe Euro has fallen by 0.13% at 1.1449 |

EUR/CHF and USD/CHF, October 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Led by a dramatic recovery in US stocks, global equities are moving higher today. Before last week, decline, the US stock market lacked breadth, but not only did the S&P 500 and NASDAQ post their biggest advance in several months, but the small-cap stocks in the Russell 2000 had their best day in a couple of years. Asian equities followed suit, with the main equity market in Japan, Australia, Korea, and Singapore rising more than one percent. The MSCI Asia Pacific Index rose in back-to-back sessions for the first time in nearly three weeks. Although the Shanghai Composite gains were not particularly large (~0.6%), the recovery from new four-year lows may have signaled a reversal. European shares are posting more modest gains, and the Dow Jone Stoxx 600 is higher for the third consecutive session (~0.25%), led by information technology and materials. US shares are flat and may need to consolidate after yesterday’s sharp advance. The recovery in global shares is not sapping the bond market and ten-year benchmark yields are mostly one-to-two basis points lower. The US dollar is narrowly mixed against the major currencies, where the Antipodean currencies and Scandis are firmer. Brexit concerns and a soft inflation report are weighing on sterling. Oil prices are firm after the API estimated an unexpected 2.1 mln barrel draw of US oil inventories. It was the first reduction in four weeks. The EIA was expected to report a 2.5 mln barrel build today. Sterling: There are three developments to note. First, although little progress has been reported on the divorce proceedings, the UK and EU still seem close, and after the summit concludes, negotiations will continue. The top negotiator for the EC reportedly offered the UK a full-year extension in exchange for accepting a two-tier backstop to avoid a hard border between Northern Ireland and the Republic. Second, the UK’s September consumer inflation was weaker than expected. The preferred CPIH, which includes owner-occupied housing costs, slowed to 2.2% from 2.4% and matches the lowest of the year. CPI itself eased to 2.4% from 2.7%, and core rate moderated to 1.9% from 2.1%. Separately, the UK reported its house price index slowed to 3.2%, the weakest in five years. London house prices were the weakest, slipping 0.2%. UK short-term rates are marginally lower. Sterling is finding support near $1.3120, ahead of the week’s low of $1.3080. There is an option for nearly GBP500 mln at $1.3180 that will be cut today, and there is a 430 mln euro option struck aatGBP0.8800 that also expires. |

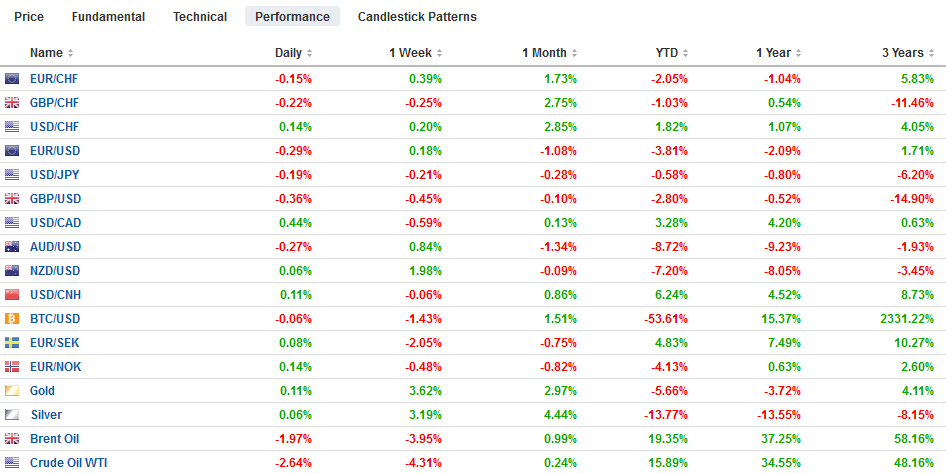

FX Performance, October 17 - Click to enlarge |

Euro: The confirmation of September CPI (2.1% on the headline and 0.9% at the core) failed to provide investors with fresh incentives. The eurozone also reported a soft August construction spending report. It was the first back-to-back decline in two years. Although last week’s slide in equities seemed to spur short-covering gains in the euro, the single currency remains resilient despite the equity recovery in recent days. The euro dipped briefly below $1.1550 in Asia but held above the week’s low near $1.1535 and additional support that extends to $1.1525. The gains yesterday faltered just shy of the $1.1630 resistance area, and the market may think twice of retesting it, especially with the help of a nearly 800 mln euro expiring today at $1.1575. One of the considerations behind the euro’s resilience may be the better performance of Italy. The Italian 10-year premium over Germany peaked near 308 bp and now is near 293 bp. Italian bank shares have also stabilized and are up for the third consecutive session, over which time the index has risen by about 2%.

Yen: The dollar bottomed against the yen on Monday near JPY111.65. It reached a new three-day high a little above JPY112. 40, where a JPY350 mln option will expire today. The intraday technicals favor upside. A move above JPY112.75 would help lift the tone.

There are two other data points to note in Asia. First, today’s Chinese lending data gives more evidence that officials have softened their efforts curb shadow banking ostensibly to offset some of the weakness that may have been, at least partly, spurred by dislocations associated with trade tensions. The difference between yuan loans and total aggregate financing is a proxy for the shadow banking. In July, for example, the yuan loans were greater than aggregate financing (CNY1.45 trillion vs. CNY1.04 trillion respectively). This is the opposite of what was reported for September. Yuan loans rose CNY1.38 trillion, while aggregate financing rose CNY2.21 trillion.

Second, given Singapore’s entrepot role, its trade performance is often seen as a bellwether. Today’s report showed non-oil exports rising by 8.3% in September (year-over-year) after a 5% increase in August.

South Korea’s central bank meets tomorrow. A slight majority of a Bloomberg survey do not expect a change in the key seven-day repo rate currently at 1.5%. If a hike is not delivered now, a move is likely next month. The rate differential is widening, inflation ticked up last month (.197% vs. 2% target). However, South Korea may be nearing the end of its tightening cycle. Earlier this week, the IMF cut the country’s growth forecast to 2.8% year-over-year from 3.0% and next year to 2.6% from 2.9%.

Staying in the emerging market space, we note the mild easing of tension in Turkey’s money market. The central bank meets next week. Although many banks had been forecasting a hike, the appreciation of the lira is giving them pause. The lira has appreciated for eight consecutive sessions coming into today, and it is slightly firmer, and over this streak, the US dollar has fallen about 10%. Turkey is feeling more confident and sold dollar-denominated bonds for the first time in six months. The $2 bln (five-year) offering was three-times over-subscribed at 7.5%.

Many observers still insist on taking Trump literally and had a field day with his claim that the Fed was his “biggest threat.” Investors, rather than the commentariat, know that the US President connotation is more important than the denotation. There was no change in market expectations for the trajectory of Fed policy through the end of next year.

There is no point in citing all the threats to the US and comparing them to the Federal Reserve. The fact of the matter is that the risk Trump takes on trade and threatening to walk away from multilateral organizations, like the WTO, if not satisfied, is made possible by a strong economy that can absorb the potential shocks. There are many mainstream economists who share the view that the US business cycle does not die of old age but is instead murdered by the Federal Reserve and an overly vigorous monetary policy. Trump is not alone in warning that the Fed is again being too aggressive. This is partly the debate over the significance of the flattening yield curve.

It is true that the TIC data for August showed that the value of Chinese-held Treasuries fell for the third consecutive month. However, the change was so small, and the numbers are so imprecise that no hard conclusions should be drawn from the fact that holdings attributed to Chinese entities fell $6 bln to $1.165 trillion. It is hardly a rounding error. Japan, the second largest foreign holder of US Treasuries, saw its holds slip by the same amount to $1.030 trillion, though it is interesting the different verbs the media uses to describe the two, with latter somehow less dramatic.

The more important takeaway is the strength of the demand for US financial assets. The demand for US long-term assets reached $131.8 bln in August, the most since September 2014. This year’s average through July was $49.3 bln and $44.4 bln in 2017. Through August, there has been the net purchase of $476.8 bln of US financial assets. The current account deficit in H1 was $223.2 bln.

The US reports housing starts and the FOMC minutes from last month’s meeting that including a rate hike. The interest-rate sensitive housing market is showing some signs of weakness, and there have been reports of some banks reducing their headcount this space. Housing starts rose a sharp 9.2% in August, matching last year’s strongest report. However, the signal is the other. A decline (~5%) that is expected for September would be the third decline in the past four months. Permits may have ticked up, but even so, through August were off four months of the past five. Since the Fed hiked and made little adjustment to their forecasts, the minutes are unlikely to do much more than provide some color. Investors are confident of a December hike.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,EUR/CHF,EUR/CHF and USD/CHF,newsletter,SPX,USD/CHF