Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

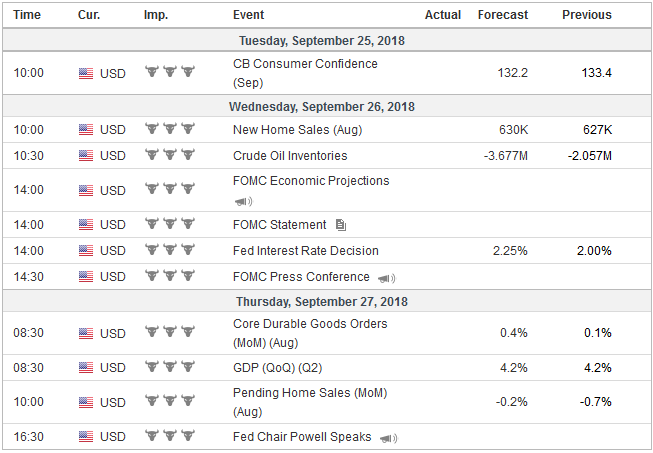

It is a testament to the Federal Reserves communication and the evolution of investors’ understanding that we can say that the rate hike that the central bank will deliver is not as important as what it says. A rate hike is a foregone conclusion. According to the CME’s model, there is about an 85% chance of December hike discounted as well.

The effective Fed funds rate is 1.92% with the target range of 1.75%-2.00%. The implied yield of the June 2019 is 2.62%. The market has 70 bp of tightening priced in through the first half of next year. In H2 19, there is another 20 bp discounted.

The new information that investors will receive is an updated economic assessment and updated forecasts. In June, the change of one member’s forecast was sufficient to lift the median forecast to two hikes in H2. In some ways, we should get a validation of this signal. The median forecast is also likely to continue to point to three rate hikes next year. The June forecasts also anticipated one hike in 2020, putting it 50 bp above what the officials see as the long-term equilibrium rate. For the first time, the Fed will extend its forecasts into 2021.

Over the past month, the yield of the entire coupon curve has risen 20-25 bp and the 2-10 year curve has stabilized. This coupled with a review of the breakeven rates suggest that the rise in nominal rates reflects a rise in real rates rather than inflation expectations. The 11 bp rise in the three-month T-bill yield over the same period points to supply as the likely culprit.

Tax Reform 2.0 is composed of three bills make individual tax cuts permanent, create a new savings vehicle, and provide tax incentives to start of business. Although the combination of tax cuts and spending increases have not fully run their course, this other round is in the works. All three bills may not be passed before the November election. However, when the stimulus has exhausted that is when there is much speculation about a “fiscal cliff” or the end of government-spurred expansions in 2020. We suspect the business cycle could peak earlier–the middle quarters of next year–putting the Fed on hold and allowing for a rate cut before the 2020 election.

United StatesThe US policy mix of fiscal expansion and monetary tightening is continuing to develop in both directions. As we have argued, this is the most bullish policy mix for a currency. At the same time, it puts the US in the best position to weather the disruptions caused by its trade policy. US President Trump’s claim that many countries are taking advantage of the US and the chronic trade deficit illustrates this strikes a responsive chord among many Americans. The 10% tariff on about $200 bln of Chinese goods will be implemented Monday, and China has already indicated its retaliatory measures. Both sides have tweaked their lists, but that should not be seen as a sign that a deal is around the corner. Not only will that tariff be raised to 25% on January 1, but Trump has threatened to levy another tariff on $267 bln of Chinese goods if it retaliated. If it follows the similar pattern, the new round of tariffs could be implemented as early as November. |

Economic Events: United States, Week September 24 - Click to enlarge |

ChinaMeanwhile, China has indicated it will not accept the US Treasury invitation to meet in Washington for talks. It has been made patently clear numerous times that in the Trump Administration trade policy is not set by the Treasury Department. For its part, China is looking to find alternative sources of US imports. It has already reduced some tariffs on neighbors and more are expected in the period ahead. Measures to blunt the impact on the domestic economy are also being considered. Caixin and the government’s PMI measures will be reported next week. They will be the first look into September activity and may offer some insight into the impact of the trade tensions. China will also report its final estimate for the Q2 current account. After reporting a $34 bln deficit in Q1, China’s preliminary estimate was of a $5.8 bln surplus in Q2. China has not reported a current account deficit for two quarters for at least 20-years for which data is readily available. The yuan itself has stabilized after depreciating earlier this year. September is the second month in which the dollar has traded between CNY6.80 and CNY6.90. The offshore yuan (CNH) is trading a little firmer than the onshore yuan (CNY) suggesting speculative pressure to weaken it are at a low ebb. |

Economic Events: China, Week September 24 - Click to enlarge |

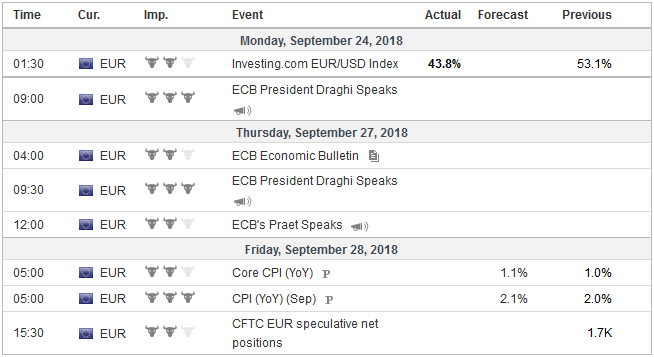

EurozoneEurozone inflation is remarkably stable. In the first eight months of the year, headline CPI averaged 1.6%, the same as in the first eight months of last year. At 2.0% in July, it was in the upper end of the range that it has been in since the middle of 2016. The core rate tells a similar story. It has averaged 1.0% so far this year; the same as for same period in 2017. The average in 2016 was 0.9%. Political developments in Europe may overshadow the CPI report, especially given that monetary policy appears to be on automatic pilot even if humans are still in the cockpit. The German state of Bavaria holds elections on October 14. They cannot be soon enough for CSU Seehofer, who has seen his party slip in the polls and the AfD rise. The CSU is most likely going to lose its outright majority. It seems almost certain that the AfD will be represented in the local parliament. The CSU blames Merkel’s immigration policies for its predicament. In the run-up to the election, Seehofer and Bavarian Governor Soder may tact to the right as other central-right politicians frequently have done in Europe to 1) retain voters who would otherwise defect and 2) attract more voters. This means being critical of Merkel, whose CDU is drawing the least support on record, according to recent polls. The mishandling of Maassen, who was promoted to a deputy minister post (Interior) rather than be dismissed for his support for the AfD, provides additional drama. Italy commands attention. Over the past couple of weeks, several banks have taken a more optimistic stance toward Italy and Italian bonds. Recall that after the spring election, capital went on strike. The 4-week moving average of the 10-year yield rose from 1.75% in late April to 2.80% two months later. It peaked earlier this month near 3.10%. Some of the more bellicose rhetoric has ben been toned down. Talk of the urgent need for a parallel currency has all but been forgotten. The 10-year yield has fallen nearly 50 bp this month, and this has been fully reflected in the premium over Germany (peaked on August 31 a little above 290 basis points and was finished last week near 235 basis points. Next week may test the new found optimism. Finance Minister Tria is reportedly fending off demands from the two deputy prime ministers have pet projects (tax cuts for the League and a new assistance program for the 5-Star Movement). Disappointing growth this has a knock-on effect to boost the deficit (as a percent of GDP). Tria will publish his initial projections. |

Economic Events: Eurozone, Week September 24 - Click to enlarge |

Canada

NAFTA moves back into the fore as well. The idea is an agreement with Canada is important to be reached by the end of September in order to allow the current Mexican President sign-off on it rather than AMLO who takes office on December 1. It would also enhance the chances that the current US Congress could approve it, even in a Lame Duck session after the November election, which could very well change the control of one or both chambers of the legislative branch.

Canada is likely to come under greater pressure as the month-end deadline approaches, and it would not be surprising if it becomes the target of Trump’s social media attention. The strength of last week’s data saw the probability of a Bank of Canada rate hike next month rise from high to higher (86.2% to 89.2%), but the Canadian dollar may have gotten all it could from the rate channel, at least for the time being. At the end of last week, the US dollar successfully tested the lows seen in late August near CAD1.2885. The burden is on the US dollar bears. If they cannot extend the dollar’s losses through there, we suspect it will snap back like pushing a beach ball under the water.

The preliminary estimate of September consumer prices for EMU will draw attention but it is not going to drive policy. At the start of next month, the ECB will dial back the bonds it is buying from 30 bln euro a month to 15 bln and will stop at the end of the year. ECB President Draghi has preserved some flexibility but the bar to extend the program is high.

United Kingdom

For the first time since the UK referendum in June 2016, there seemed to have been more constructive voices from the EC. We have been skeptical because there appear to be three constituencies, the EC, the Cabinet, and Parliament, which, not just May, but possibly no mortal, can please simultaneously. While sterling benefitted during the dollar’s pullback since mid-August, it also was aided by appeared to be the change in tone. For example, it has also had appreciated about 2.75% against the euro this month.

The goodwill was washed away and sterling dropped nearly 1.5% against the dollar before the weekend. That was its single biggest decline in 15 months. The euro posted the biggest advance against sterling since April. There is little chance that there will be a rapprochement ahead of May’s speech on the last night of the Tory Party conference on October 3. Under this scenario, the euro can rise through last month’s high near GBP0.9100, and sterling would unwind its recent gains against the dollar.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$CNY,$EUR,Brexit,Federal Reserve,Germany,Italy,MXN,newsletter,U.K.