Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

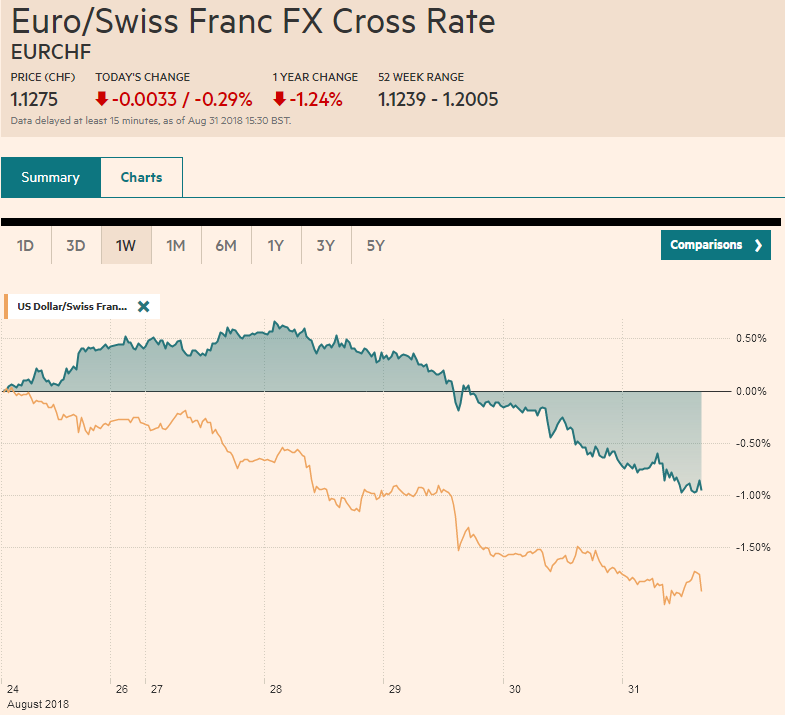

Swiss FrancThe Euro has risen by 0.29% at 1.1275. |

EUR/CHF and USD/CHF, August 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe dramatic price action seen yesterday among several emerging market currencies is eased today, but here at month-end, demand for risk-assets is tentative at best. The macro backdrop, including the increase in US core inflation, expectations for continued hikes by the Federal Reserve, and unambiguous signals that trade tensions will increase in the coming weeks dampens the risk appetite. The dollar benefitted broadly from this yesterday, but not against the yen. The greenback had been bouncing up against a three-year weekly downtrend line near JPY111.60. The unwinding of structured positions and short-term momentum players drove the dollar marginally through JPY111.00. Yesterday’s 0.65% dollar decline was the largest in a little over a month, and there has been follow-through selling today, pushing the greenback to JPY110.70. Additional support is seen near JPY110.50. There are several options expiring today. First, consider that there are $2.16 bln in options at JPY110.00-JPY110.25 and almost $700 mln at JPY110.50. Then the JPY1110.80-JPY110.85 houses another $1.19 bln in expiring option, with as much as $3.6 bln in options struck from JPY111.00 to JPY111.60. |

FX Performance, August 31 - Click to enlarge |

Separately, Japan reported an unexpected rise in the July unemployment rate to 2.5% from 2.4% and an unanticipated decline in industrial output (-0.1% vs. Reuters survey expecting a 0.2% increase following a 1.8% decline in June and a 0.2% decline in May). Separately, Japan also reported disappointing June auto output and July construction orders. The government’s capex survey out early next week will shape expectations for revisions to Q2 GDP.

After local markets closed, the BOJ announced some small tweaks to its September bond-buying plans. Essentially, it reduced the number of days it would make its purchases from six to five for 1-10 year bonds. However, it also increased the amount it could buy. Initially, it looked like some observers were putting more weight on the frequency than the increased range of potential purchases, and many concluded this was part of the “stealth tapering.”

The Nikkei snapped an eight-day advance with a 0.2% decline. It had fallen further during the session and recorded new lows for the week. However, although it entered the gap created by Monday’s sharply higher opening, the gap was not filled, and the Nikkei recovered to close near its highs. The 23,000 cap remains intact, but another attempt on it is likely in the coming days.

China’s August PMIs were better sequentially and relative to expectations. The manufacturing PMI edged up to 51.3 from 51.2. The median Bloomberg respondent saw a small decline. The same story was in the non-manufacturing PMI. It improved to 54.2 from 54.0. A weaker report was expected. The net result was an increase in the composite to 53.8 from 53.6. It has averaged 53.9 over the past three months, compares with 54.4 in Q2, 53.8 in Q1 and 54.3 in 2017.

The US dollar eased slightly against the yuan today to pare the week’s gains to about 0.4%. Since the middle of May, there have only been two weeks in which the yuan has gained against the dollar. The Shanghai Composite, which had been up slightly for the week, lost nearly 0.5% today to ensure a small weekly loss of about 0.2%. For the month, it shed 5.25%.

Most equity markets in the region were lower, with Korea being the notable exception. Korea and Taiwan saw strong foreign buying this week with both markets absorbing more than $1 bln of foreign equity inflows. On the week the Taiex rose nearly 2.4%, while the Kospi rose 1.3% (the KOSDAQ rose 2.4%). The MSCI Asia Pacific Index matched yesterday’s 0.3% decline but finished 1.2% higher on the week (and -0.85% for the month).

Euro and sterling turnover is quiet, and both have been largely confined to yesterday’s ranges. The economic news stream consists of slight downward revisions to EMU’s August CPI estimate to 2.0% and 1.0% for the headline and core CPI respectively, both 0.1% lower than the preliminary estimate. The EMU also reported that unemployment stood at 8.2% in July, the same as in June when the downward revision is taken into account. Separately, Nationwide reported an unexpected 0.5% decline in house prices in August, bringing the year-over-year increase down to 2.0%, matching the slowest pace in a few years.

There are several large euro options expiring today concentrated in the $1.1675-$1.1725. At $1.1675 there is a 1.1 bln euro option that will be cut and another 575 mln at a $1.1695 strike. At $1.17, there a 1.4 bln euro option and $1.1725 holds 1.5 bln euros. Sterling has traded in a tight range around $1.30, where there is nearly a nearly GBBP970 mln option expiring.

European shares began the last session of the month nursing a small gain for the week. However, the Dow Jones Stoxx 600 is about 0.5% lower in late morning turnover is enough to push it into the read for the week. Italian and Spanish benchmarks fell nearly 2% this week. For the month, the Dow Jones Stoxx is off a little more than 2%, the most since March.

Some rebalancing in the European bond market may help explain the outperformance by the Italy, where the 10-year benchmark is off 5 bp, and other peripheral bond yields are off 1-2 bp, while core European yields are a little firmer. The widening spread this month between Germany and Italy of about 50 bp approached levels seen in the May drama. There are two immediate implications for investors. First, the growing Italian premium is inversely correlated with the euro (-0.51 over the past 60-sessions on a purely directional basis). Second, the link between the sovereign and the banks remains in place. The index of Italian bank share is off nearly 3.5% this week to bring the month’s drop to about 16.4%.

Fitch is due to announce the review of Italy’s sovereign rating. It is currently assigned a BBB rating. Since the new government has yet to deliver a budget, Fitch may be reluctant to cut the rating. However, it is possible that it changes the outlook for stable to negative. Fitch is the first major review since the start of the new government and the sharp rise yields.

Turkey took additional steps to discourage sales of the lira without addressing the underlying policies which have repelled investors. Turkey announced an increase in the tax on six-month foreign currency deposits to 20% from 18% and on fx accounts up to one-year, the tax increased to 16% form 15%. It also cut the tax on one-year lira deposits to 3% from 12% and cut the tax to zero for lira deposits of longer duration. Given the volatility of the currency, the small tax changes are little more than a distraction.

Although official comments about NAFTA 2.0 reassure investors that progress is being made. However, today’s deadline may come and go. Talks will likely continue over the next couple of days Both the Canadian dollar and peso are slightly lower as some participants are getting nervous. Note that there is a $753 mln option at CAD1.30 that expires today.

Even if a NAFTA 2.0 deal is struck, trade tensions are set to rise. Reports indicate that the US President intends on going forward with new tariffs on $200 bln of Chinese imports because it retaliated against US action to punish the PRC for intellectual property rights violations. China has already indicated it will respond by levying tariffs on $60 bln of US goods. Separately, Trump seems to recognize this his trade strategy is conflicting with his geopolitical strategy. He indicated China is not cooperating as much with North Korea because of the trade tensions. Trump recently canceled the Secretary of State’s trip to North Korea.

The US is not ready to have serious trade negotiations with China. It seems that Chinese officials attribute it to posturing ahead of the mid-term elections in November. We think this means that China may still not recognize the broad-based support for a sustained economic confrontation in the US. The US political landscape may be polarized but one bridge issue is China has taken advantage of the US. What Graham Allison has called the Thucydides Trap seems to be well entrenched in pop psychology and culture.

Trump is also not in the mood to resolve the trade dispute with Europe. Reports indicate that in talks Europea has offered to abolish tariffs on US autos. President Trump pushed back. It was not sufficient because European consumers, he said, were conditioned to buy domestic brands.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,newsletter,USD/CHF