The relationship between Microsoft and OpenAI has been a defining partnership in the blooming AI technology. But the partnership terms are changing, and what was once a solid relationship may be fracturing. On Monday morning, Microsoft shares quickly fell 5% as the Bloomberg headline “OpenAI Breaks Free From Exclusive AI Pact With Partner Microsoft” sent concern among Microsoft investors. Microsoft shares snapped back once the revised partnership agreement was fully disseminated.

Microsoft and OpenAI have mutually agreed to end Microsoft's exclusive rights to sell OpenAI’s models. Accordingly, OpenAI can source arrangements with Microsoft’s hyperscale competitors, such as Amazon and Meta. In exchange for giving up its monopoly on OpenAI products, Microsoft will no longer pay OpenAI a revenue share from the OpenAI products it sells. However, OpenAI will continue to abide by its revenue-sharing agreement with Microsoft until 2032, two years beyond the original agreement. OpenAI API products will remain exclusive to Microsoft's Azure platform, while non-API products can use any cloud vendor. Further, OpenAI has contracted to purchase an additional $250 billion of Microsoft Azure services.

The bottom line is that Microsoft retains significant protections, but OpenAI is gaining some freedom. Analyst Jason Ader of William Blair summarized the revised partnership terms as follows:

"By securing IP rights through 2032, Microsoft protects the foundation of its Copilot strategy and Azure OpenAI monetization — still, Azure will now have to compete for more of OpenAI's workloads going forward."

What To Watch Today

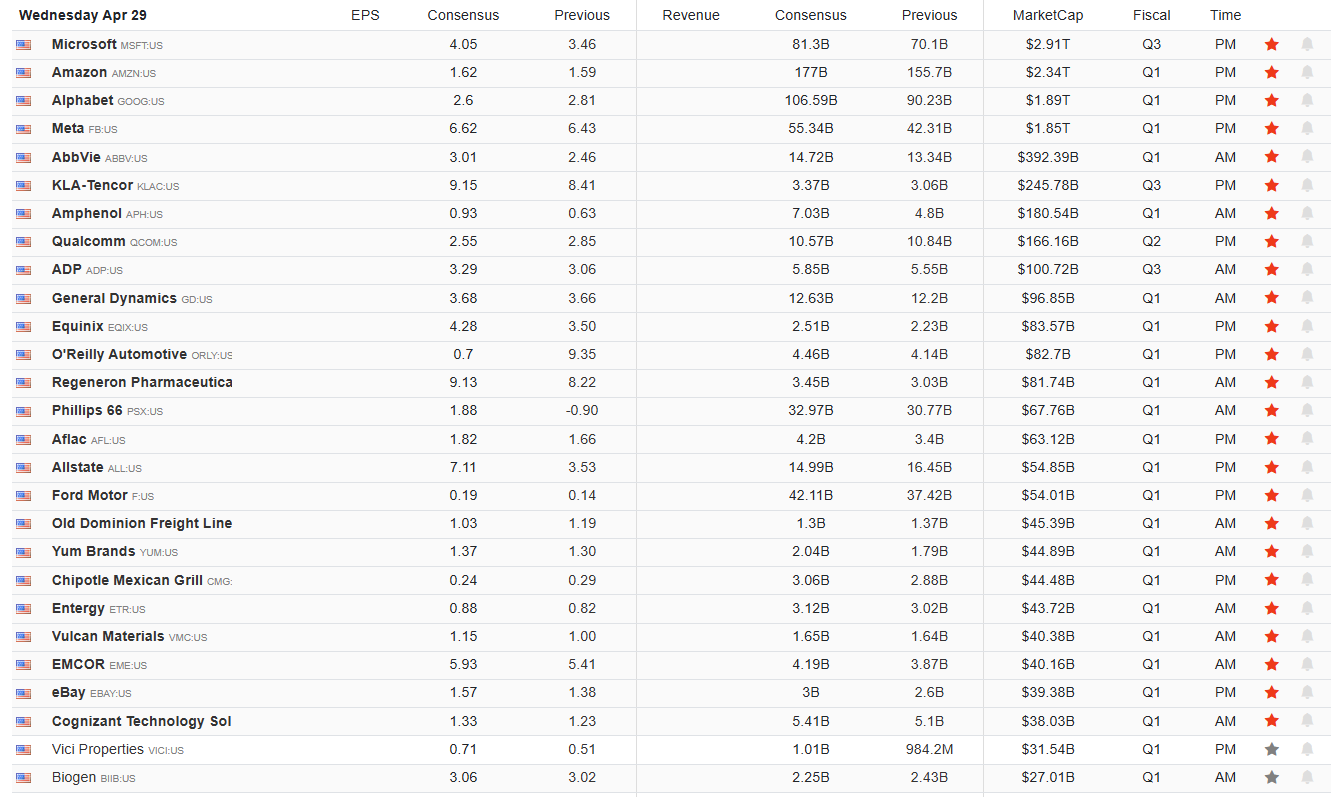

Earnings

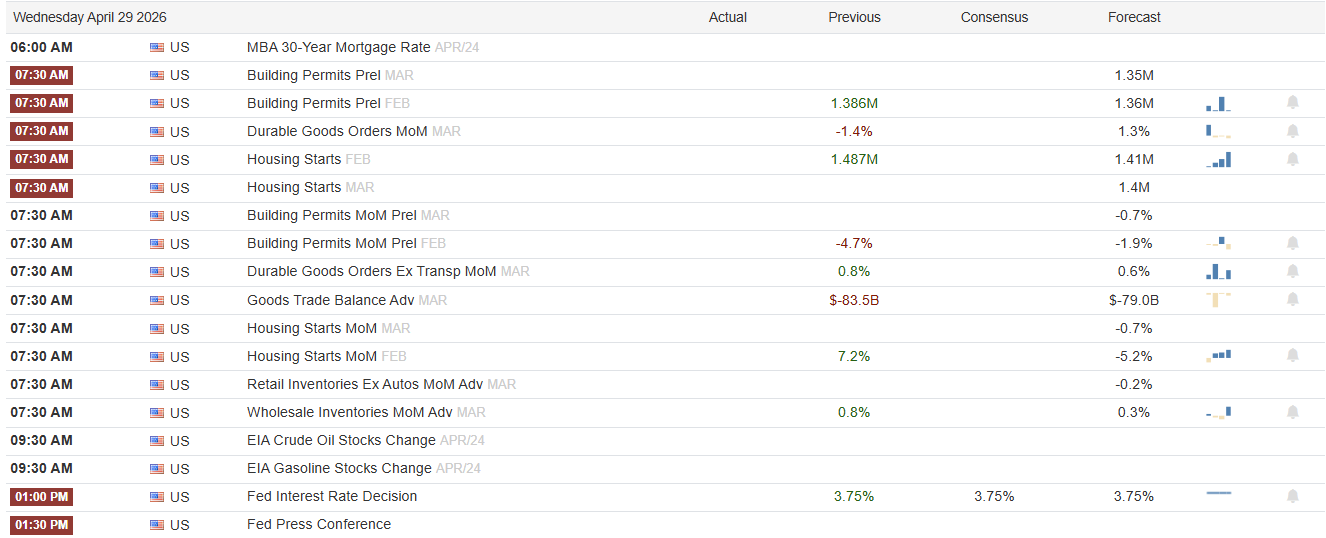

Economy

Market Trading Update

Yesterday, we discussed the seasonality of May as we enter the year's seasonally weak period. However, that won't matter until next week.

Today brings a true gauntlet for markets. Microsoft, Amazon, Alphabet, and Meta all report after the close, and the FOMC delivers its policy decision midafternoon. Roughly 40% of the S&P 500's market cap hands over its outlook in a single window, and the Fed gets to set the tone for risk appetite right before the bell. As I wrote last week, when the calendar concentrates this much catalyst into one session, the asymmetry tilts against complacent positioning.

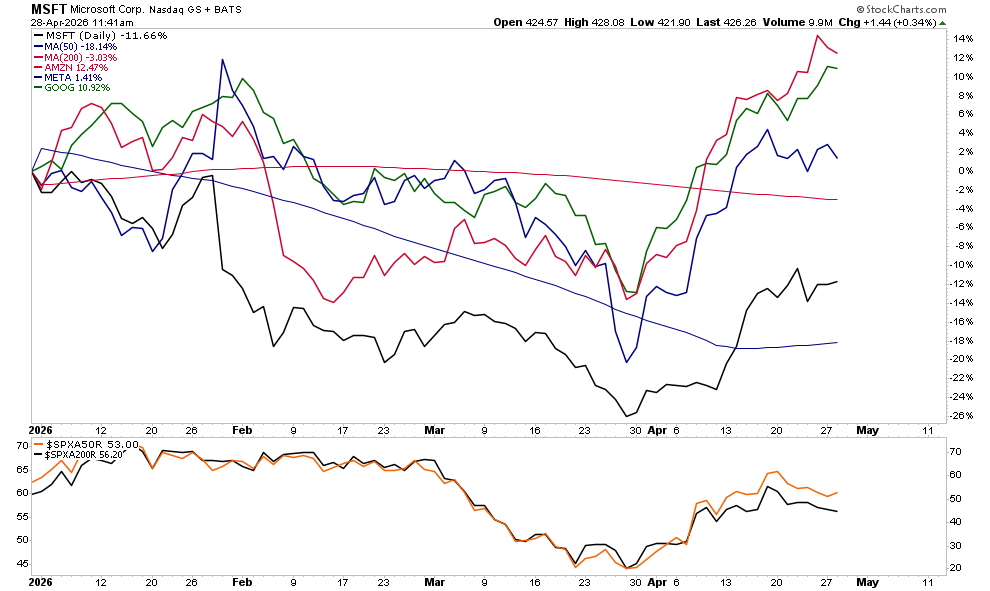

Expectations are not modest. Consensus has Microsoft posting another quarter of mid-teens revenue growth driven by Azure and Copilot monetization. Alphabet is expected to show search resilience and cloud margin expansion. Meta needs to justify its capex trajectory with continued ad-revenue strength, and Amazon must demonstrate AWS reacceleration alongside retail-margin discipline. The bar is particularly high because prices have risen so aggressively in recent weeks. The Magnificent names are trading well above their 50-day moving averages with stretched RSI readings, and several are extended more than 10% above trend.

Here is the problem. OpenAI's recent infrastructure announcement reframed the AI capex conversation overnight. Investors who had grown comfortable with the "AI builds itself in" narrative now face the prospect that hyperscaler capital intensity is rising again, not falling. Microsoft alone is likely to guide to capex above $100 billion next year. That is good news for Nvidia and the AI supply chain. It is more complicated for the hyperscalers themselves, where free cash flow conversion gets squeezed and return on capital math is pushed further into the future. The market has priced flawless execution and steadily rising AI revenue. Anything less rates a sell-the-news response, particularly given how stretched these stocks are heading in.

A few notes about earnings this evening:

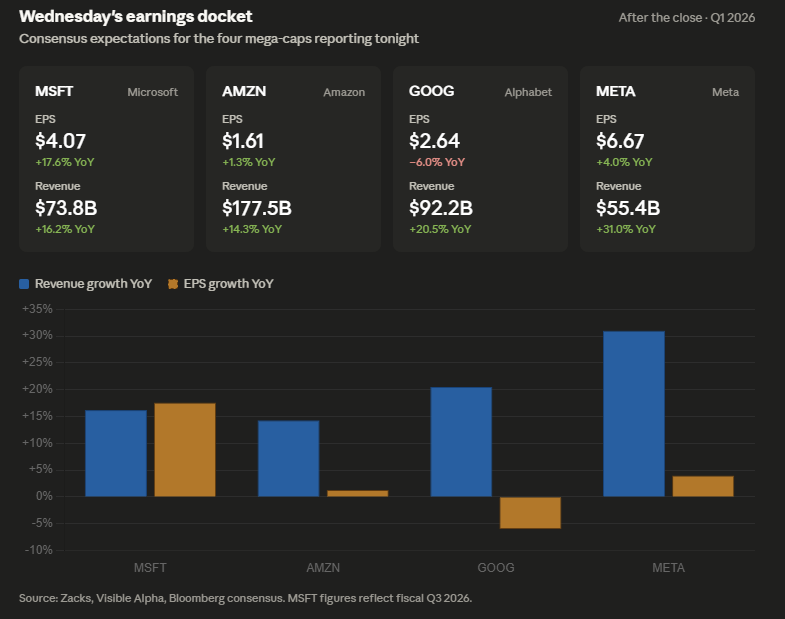

- Meta's revenue bar towers over the rest at +31%, but EPS growth is only +4% — that gap is the capex story in one chart. The Street is funding the build-out, but every dollar is going into MTIA silicon and data centers, not the bottom line.

- Alphabet is the only name on the slate with negative EPS growth (-6%), despite the strongest revenue acceleration ex-Meta. Stock-based comp and cloud investment are the swing factors. A clean cloud number near the $18.4B consensus, with RPO accelerating overrides, trumps the EPS optic.

- Microsoft is the most balanced print — EPS and revenue growth roughly matched in the high teens — but the bar to clear is Azure constant-currency above 38%. Anything below 36% reopens the capacity-constraint debate the bulls have been leaning on.

- Amazon is the wildcard. The EPS growth of just +1.3% looks soft, but that is the AWS capex flowing through depreciation. The print lives or dies on AWS actually hitting the 25%+ growth handle.

The FOMC adds another layer. A hold is fully priced. The risk lies in the press conference. If Powell pushes back on the easing path the curve has built in, equities will absorb that hit before they ever see the earnings tape. If he validates further cuts, dollar-sensitive names rip, but the hyperscaler reaction function is still tied to capex guidance and forward AI commentary, not the funds rate.

I am not adding risk into this print. Trim into strength on names trading well above trend, raise a little cash, and let the reports clear before reaching for exposure. Discipline beats conviction when four mega-caps and the Fed share a single afternoon.

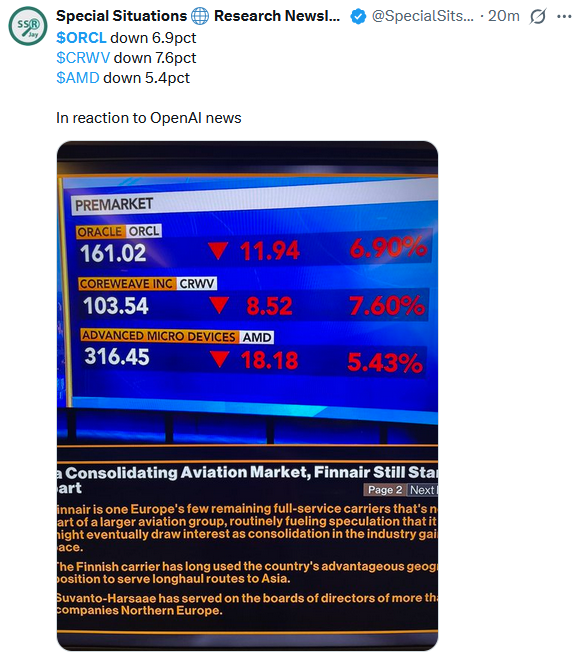

OpenAI Doubts Raise Concerns For Oracle Investors

An article published on Tuesday by the Wall Street Journal reports that there are headwinds to OpenAI's once-invincible growth story. Although a private company, OpenAI missed its internal goal of reaching one billion weekly active users by year-end and fell short of its ChatGPT revenue target as it is dealing with larger-than-expected subscriber cancellation rates. This comes on top of a report from earlier this year that also showed they missed multiple monthly revenue targets. CFO Sarah Friar has reportedly raised concerns that the company may be unable to fund its future computing contracts if revenue growth fails to keep pace with its internal goals. That is concerning for its clients, especially given that they just raised over $122 billion in a funding round.

The impact of OpenAI's shortfalls is pressuring companies like Oracle. Oracle provides two core products to OpenAI. It is the primary builder and operator of Stargate data centers that train and run OpenAI's models. Second, Oracle provides cloud computing services directly to OpenAI. More simply, Oracle builds the buildings, fills them with chips, powers them, and charges OpenAI to use them. Accordingly, investors in companies like Oracle are voicing concern over concerns at OpenAI.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post The Microsoft OpenAI Marriage Is On Rocky Ground appeared first on RIA.

Full story here Are you the author?You Might Also Like

High Oil Prices Won’t Spark A 1970s Inflation Repeat

High Oil Prices Won’t Spark A 1970s Inflation Repeat

2026-03-25

Some media pundits are warning the public that high oil prices will spark a repeat of the high-inflation era of the 1970s. High oil prices will feed through to inflation; however, the economic, monetary policy, and geopolitical environments of the 1970s are quite different from today’s. To wit, consider the following reasons for inflation in …

The LENDX Liquidity Trap

The LENDX Liquidity Trap

2026-03-23

The Stone Ridge Alternative Lending Risk Premium Fund (LENDX) is the latest to face liquidity pressure amid growing concerns about private credit. As an interval fund, LENDX’s shares aren’t publicly traded, so investors who want out must tender their shares for repurchase by the fund quarterly. Last Thursday, the $2.4 billion fund told clients that …

2026-03-21

🔎 At a Glance 🏛️ Market Brief – A Tough Market Week This week gave investors a brief exhale — and then took it back as Monday opened with genuine relief after news broke that a U.S.-led coalition would escort tankers through the Strait of Hormuz. On that news, oil pulled back sharply, the S&P …

2026-02-12

“Based on its current assessment, the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to target.” And with that statement, the European Central Bank (ECB) appears to have halted its rate hiking cycle. …

Technology Stocks: Dead Or An Opportunity?

Technology Stocks: Dead Or An Opportunity?

2026-02-07

🔎 At a Glance 🏛️ Market Brief – Market Volatility Returns Markets stumbled into February, a historically weak month. February tends to deliver modest returns, with average performance trailing the stronger gains typically seen in January and March. Seasonal tailwinds, such as earnings season and new-year fund flows, begin to fade, while macro headwinds, such …

European Buyers Strike Or Performance Chasing?

European Buyers Strike Or Performance Chasing?

2026-01-28

Bloomberg recently published “Wall Street Grapples With A New Risk: A European Buyers Strike.” The article notes that stock indexes in Europe, Japan, Canada, and South Korea are all beating US equities in both nominal and dollar terms. As a result, some European pension funds and other foreign buyers are trimming their exposure to US …

Tags: Featured,newsletter