Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

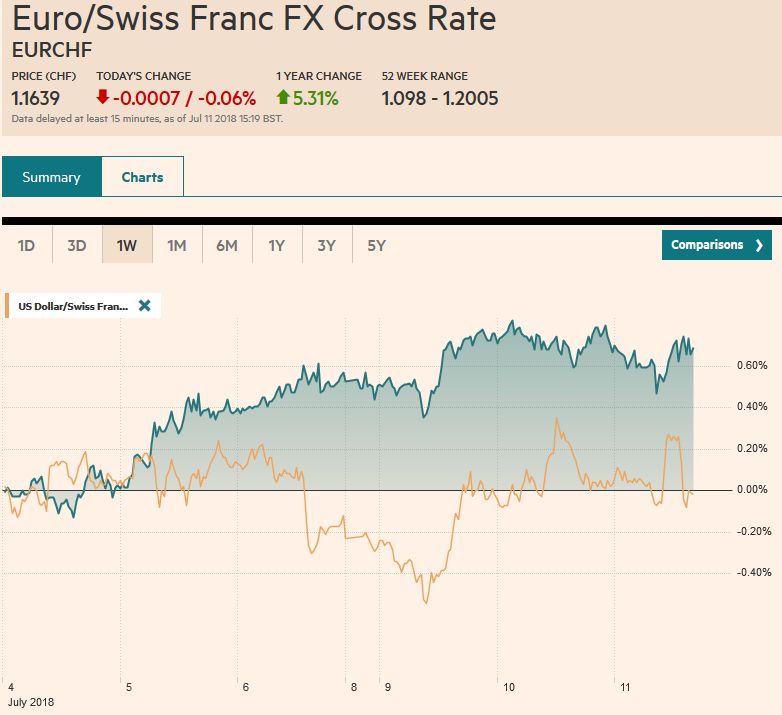

Swiss FrancThe Euro has fallen by 0.06% to 1.1639 CHF. |

EUR/CHF and USD/CHF, July 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

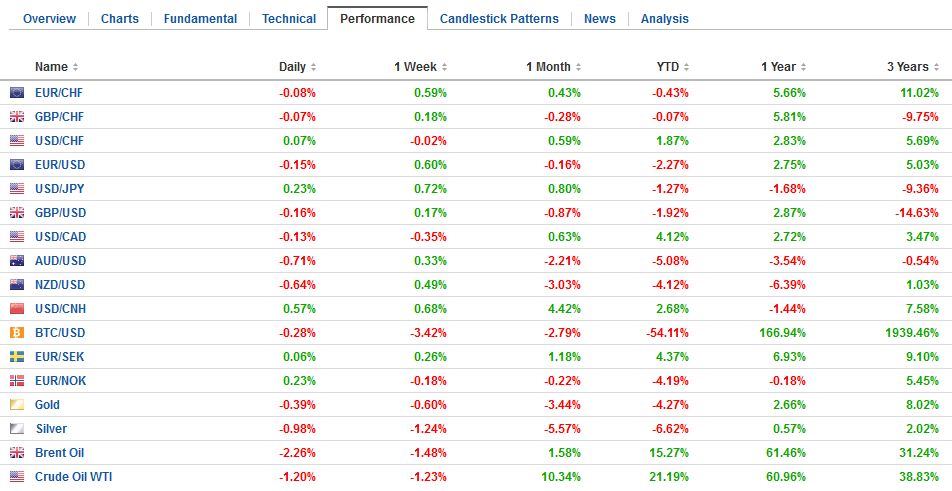

FX RatesThe US took the first step in making good its threat to put a 10% tariff on $200 bln of Chinese goods in response to the PRC retaliating for the 25% tariff on $34 bln of its exports. The US provided a list of products that will get the new tariffs after the public comment period is completed at the end of next month. This time the list included numerous consumer goods, like digital cameras, baseball gloves, but have left off popular products, like cell phones, tablets, and personal computers. |

FX Performance, July 11 - Click to enlarge |

China immediately objected and vowed to retaliate, but the tit-for-tat strategy is limited by the more modest US import penetration. Still, there are various asymmetrical ways China can respond, and it may be best for it to just do it without making major announcements, such as squeezing US businesses operating in China, which incidentally sell more than $300 bln of goods there in addition to exports. When considering the commercial relationship between the US and China, these domestically produced and sold goods are an important part even if the direct benefit to US employees is not straightforward.

The escalating trade confrontation is sucking the oxygen away from other issues and driving the capital markets today. The broad response was to take equities and commodities lower and the dollar and bonds higher. Among the major currencies, the Antipodean and Scandia have been hit the hardest. The yen and Swiss franc are down the least. The euro, yen, and sterling have largely been confined to yesterday’s range. In the emerging market space, the South African rand and Turkish lira are competing for the dubious honor of the weakest today, but nearly all emerging market currencies are lower.

The MSCI Asia Pacific Index closed poorly yesterday after turning back from the 20-day moving average. It gapped lower today and its way to a 1% drop. Some of the Asian markets open late, like India, Malaysia, and Indonesia fared better. The Shanghai Composite ended a three-day rally with a 1.75% decline, and the yuan fell 0.6%.

The major European equity markets are off sharply. The Dow Jones Stoxx 600 also gapped (slightly) lower. It is threatening to end the six-day advance which was longest in four months. The 1.1% decline through the European morning offset the gains seen in the past two sessions. All of the main industrial sectors are lower, with materials, energy and financials hit the hardest.

The economic calendar has been light. The main feature so far today has been the better than expected Japanese core machinery orders. The 3.7% decline in May was smaller than expected after a 10.1% surge in April. The year-over-year rate rose to 16.5% (from 9.6%), which is the strongest in three years.

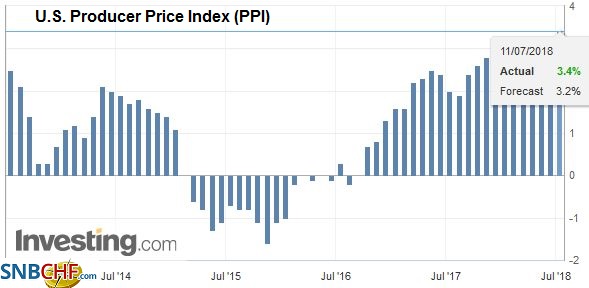

United StatesThe US reports June producer prices. The market typically does not react much to the PPI report, but economists will scrutinize it for clues into tomorrow’s more important CPI, where the headline is expected to creep a touch closer to 3% threshold. |

U.S. Producer Price Index (PPI) YoY, Jul 2013 - Jul 2018 Source: investing.com - Click to enlarge |

One of the highlights today was going to be a Bank of Canada rate hike. The fact that it is nearly fully discounted and the strong US dollar backdrop has kept the Canadian dollar on the defensive. Indeed, the US tariffs on China and the strident attitude at NATO plays on the uncertainty that makes the central bank cautious. It is not so much, perhaps, that the US is unpredictable, but rather that the course it has struck on is nearly the exact opposite of what has been the case. That said, the Bank of Canada is one of the few major central banks that could match the anticipated tow hikes by the Fed here in H2 18. We expect Governor Poloz to underscore the cautious approach but affirm that over time, it anticipates more accommodation can be removed.

The US 10-year auction takes on extra significance today after the rather poor 3-year note auction yesterday. That auction saw the lowest bid-cover (2.51) since 2009 and the smallest take down by indirect participants since 2014. Given the market segmentation, it is possible that the soft demand may be limited to the short-end of the curve.

Another story from yesterday that will carry into today’s session comes from the oil market. There have been conflicting signals between the industry estimate of US oil inventory (API) and the government’s measure (EIA). Last week, the former reported a drawdown while the latter showed a 1.2 mln barrel build. Yesterday, API again showed a 6.8 mln barrel liquidation. Brent is off a little more than 2% today, offsetting the bulk of the gains over the past couple of sessions. August WTI is off 0.8%, and it is giving back a little more than it gained in the week’s first two sessions. Dr. Copper is also sharply lower. Prices had been trying to stabilize after sliding seven sessions into the end of last week. It had gained almost 1% to start the week and pared those gains slightly yesterday. Today it is off nearly 3% to new 12-month lows. It had held the 38.2% retracement of the rally that began in early 2016 (~$279) but is though it now and looks headed toward the 50% retracement and the congestion from H1 17 near $263.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,FX Daily,newslettersent,OIL,Trade,U.S. Producer Price Index,USD/CHF