Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

All three of the major central banks met last week and confirmed that monetary policy would continue to diverge for at least another year. The clarity of the trajectory of monetary policy reduces the impact of high-frequency economic data.

There are three major disruptive forces the make for a challenging investment climate just the same: the US policy mix, trade tensions, and immigration.

The mix of tighter monetary policy and looser fiscal policy is associated with currency appreciation. That mix in the US is in extremis. Monetary policy may be accommodative, as the Fed says, but the central bank clearly signaled its intention to bring policy to restrictive levels.

At the same time, the Fed’s balance sheet unwind will to accelerate from $30 bln a month to $40 bln starting in July. We have emphasized the signaling channel by which QE worked over the material impact, but to the extent, there is an impact on quantities from the unwind, it is in the direction of tighter policy.

In 2008 and 2009, those advocating more aggressive fiscal policy, including in the US, including the Federal Reserve, were defeated on political and ideological grounds. “A debt crisis cannot be resolved by issuing more debt,” went a popular refrain. Fast forward a decade and the fiscal stimulus that is being provided in the form of tax cuts and spending cuts are larger than in 2008-2009.

United StatesThe last time the US pursued such a policy mix on anywhere near this magnitude was in the early 1980s. The US ended up sucking in so much of the world’s saving that it led to cries of relief. The dollar’s recovery from the 1970s slump began generating large trade deficits, chronic current account deficits, and a protectionist backlash. In September 1985, the G5 met at the Plaza Hotel in New York and agreed on sustained coordinated intervention to drive the dollar lower. The current synchronized global upturn cannot hide that the main economic areas are in vastly different cyclical locations. More than a third of European bonds offer negative yields. The BOJ’s holding of outstanding JGBs is approaching 50%. Even when the ECB begins to hike rates, it starts with a minus 40 bp deposit rate, and the central bank is forecasting a gradual economic slowdown in 2019 and 2020. European fiscal policy is broadly neutral, while Japan is gradually reducing its deficit and is planning on raising the sale tax in October 2019. These considerations make the US policy mix even more potent. The aggressive US trade stance makes investors uneasy, injecting a difficult to quantify uncertainty. The US went forward, as it indicated it would, specifying a list of $34 bln of Chinese goods that will be subject to a 25% tariff starting July 6. Another $16 bln of goods are subject to industry comments (July 24) before being implemented. China quickly responded in similar amounts and time. Ostensibly the time between the announcement and implementation allows for a deal to be struck. Last month China offered to buy $70 bln more US agriculture, energy, and other products but this did not satisfy the US. The US is in no mood for a compromise. Indeed, the confrontation with China is one area draws support for the administration’s critics. A leading financial newspaper showed a chart of China’s trade surplus with the US and timeline began with the Tiananmen Square Massacre, the only purpose of which is to foster animosity. The initiative swings back to the US. Trump has threatened to put tariffs on another $100 bln of Chinese goods if Beijing retaliated. It is still an open question whether the US will make good on its threat. Even if it doesn’t, more pressure will be forthcoming soon. Before the end of June, the Treasury Department is expected to announce new restrictions on Chinese investment. In early July, the US will also be hit by the implementation of retaliatory tariffs by Canada and Europe. |

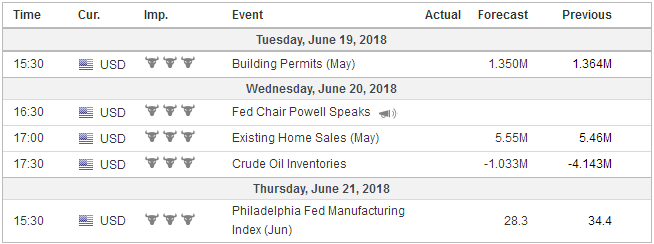

Economic Events: United States, Week June 18 - Click to enlarge |

United KingdomWhile the US is embroiled in its divisive immigration crisis and turning asylum seekers away, Europe’s refugee crisis threatens to topple two governments next week. The claim that UK needs to gain control of its borders and being in the EU prevents it, seems to animate those favoring Brexit more than any other issue. It is at the center of the debate with the EC. Prime Minister May has managed to navigate between the conflicting demands of a key minority of Tory MPs who are pro-Europe, and the Cabinet, which May selected after succeeding Cameron, where those that advocate a hard break dominate. However, the success May has enjoyed only because she has not satisfied either side, and that cannot persist much longer. The goal is to complete an agreement by October so it can go through the channels of approval and be ready for the end of the March 2019. Another game of brinkmanship is set to play out next week when the bill returns to the House of Commons. A constitutional crisis is being threatened as Parliament want a truly meaningful vote, by which the MPs seem to mean final approval, and while this would be seen as further limiting the government’s negotiating ability. Should May be forced to step down, sterling would likely immediately suffer. The most likely scenario is for someone who is advocating a harder Brexit would replace her. Sterling tends to suffer on ideas of a hard Brexit. May’s departure and the establishment of a new government could cost a couple of precious weeks of negotiations. This increases the chances of not being ready in October and an exit from the EU without an agreement. If the change in government and increased uncertainty around Brexit itself impacted interest rate expectations, that could be another weight on sterling. The BOE meets this week, and there may be one or two MPC members that favor an immediate hike. Although the majority will be inclined to stand pat, the minutes will probably show that many are getting close, maybe August close, to hiking rates. |

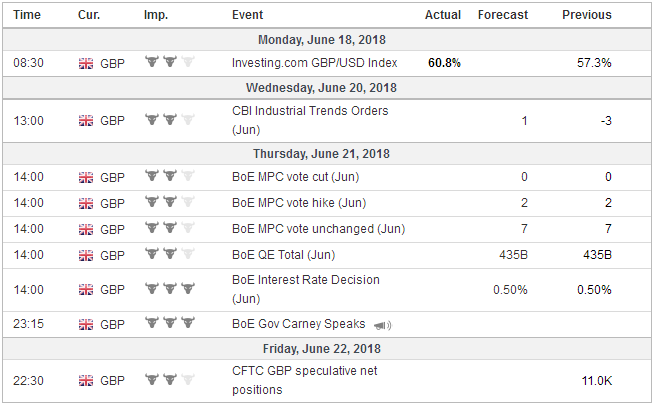

Economic Events: United Kingdom, Week June 18 - Click to enlarge |

EurozoneWe think we saw a hawkish hold by the ECB that did not prevent a dramatic slide in the euro. A hawkish hold by the BOE may not offer sterling much protection. The US premium (~1.85%) over the UK for two-year money is the most for the 30 years for which data is readily available. It would appear set to widen further in the period ahead. German Chancellor Merkel, who was billed as the head of the West by some wag at the recent G7 summit, may be in peril. She is being challenged by the Interior Minister Seehofer who is also the leader of Merkel’s coalition partner the CSU. The CSU is the center-right party in Bavaria, which faces a regional election in October. The CSU, like Merkel’s CDU, and the SPD, did poorly in last year’s national elections. Merkel’s policies had left it open to the populist anti-immigration rhetoric of the AfD. The CSU’s majority in the state house is at risk. Seehofer seeks to take a much tougher line on asylum-seekers than Merkel is prepared to sanction. Seehofer is to go before his party on Monday and seek to exercise his power as Interior Minister and go against the Chancellor’s wishes. Heresy. If Merkel does not fire him if he takes action, she will immediately be seen as weak and not in control of her government. If she dismisses him, it will precipitate a political crisis, and perhaps a collapse in the government. The two obvious courses would be a very un-German minority government or an unequally unprecedented new election. A collapse of Merkel’s government would add to the weight on the euro that has seen it return to its recent lows, nine cents lower over the past two months. The prospects of it may have contributed to the slide on June 14. Then the ECB gave a hard end date for the purchases, provided details of the tapering in Q4, and confirmed what the market had largely understood to be the case; the first rate hike will still more than a year away. |

Economic Events: Eurozone, Week June 18 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week June 18 - Click to enlarge |

Following the Fed’s meeting the previous day, the ECB removed the last obstacle one may have imagined to the continued divergence of monetary policy and short-term interest rates. It may have been the final fundamental hope that underpinned the resilience of the euro bulls, who continued to amass a near record gross long position in the futures market in recent weeks. Given these considerations, we suspect the euro is vulnerable to an asymmetrical response to the flash PMI data, whereby it is more likely to sell-off on disappointment than rally on improvement.

OPEC meets at the end of next week. On paper, it appears that OPEC and non-OPEC countries have cut production by around 50% more than the 1.8 mln barrels they agreed in 2016. Saudi Arabia took a deeper cut, but around a million barrels a day of Venezuelan oil has been removed through mismanagement, underinvestments, and US sanctions. Part of the run-up in oil prices earlier in earlier in Q2 may be traced to the risk of Iranian oil being constrained by the US sanctions.

Saudi Arabia and Russia are the only countries that have meaningful slack to boost output, and they already have. OPEC does not have to do anything. In fact, it may be in Saudi Arabia’s interest not to even press for an agreement. Saudi output remains well within its quota. There is nothing wrong with the status quo. Saudi Arabia also boosts oil output in the summer months to meet the increase in electricity demand related to air conditioning. The US-centric narrative, US pressure forced the concessions, and it is in no one’s interest to challenge it.

Slower world growth, the emergence of the US as a significant energy exporter, and the rising dollar suggests the price of oil may continue to unwind its earlier gains. The US is in a better position than Europe and Japan to cope with the implications of, say another 15%-20% decline in oil prices.

The Federal Reserve targets a core rate that excludes energy, unlike the ECB and BOJ. The US economy, with the fiscal stimulus still working its way through, many GDP models suggest Q2 growth likely enjoys a 4-handle allows the Fed to be confident. The eurozone economy is cooling compared with a year ago, and net-net the Japanese economy likely stagnated in H1 18. A drop in oil prices could quickly feed through to headline measures of inflation and Japan’s core, which excludes fresh food.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,$TLT,newslettersent,OIL,SPY